Struggling to pay your IRS tax bill in full? You are not alone. Every year, millions of Americans turn to a tax payment payment plan to manage what they owe and avoid financial stress.

This guide will walk you through every aspect of the tax payment payment plan process for 2026. Learn about plan types, eligibility rules, costs, and key steps to apply, so you can make the choice that best fits your financial needs.

Discover actionable strategies to minimize penalties and interest, avoid common mistakes, and take control of your tax debt with confidence.

Understanding IRS Tax Payment Plans

Struggling with your tax bill is more common than you might think. If you are unable to pay your full balance right away, an IRS tax payment payment plan can offer a manageable solution. These plans are designed for individuals and businesses who owe taxes but need extra time to pay. They provide a structured way to resolve your debt, helping you avoid more serious consequences.

An IRS tax payment payment plan exists to help taxpayers avoid harsh penalties, interest, and aggressive collection actions. The IRS recognizes that unexpected financial challenges happen, so payment plans are designed to promote voluntary compliance. By entering into a plan, you demonstrate your intent to pay, which can stop the escalation of enforcement actions such as liens or levies.

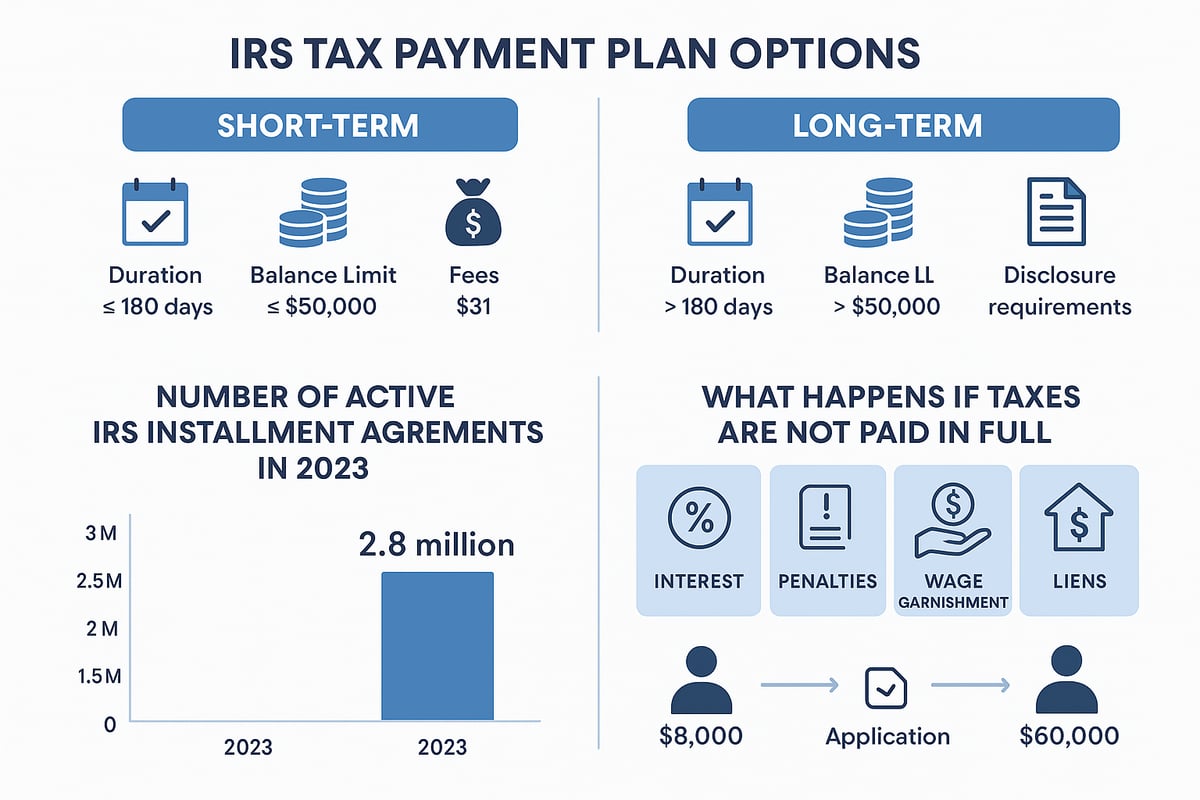

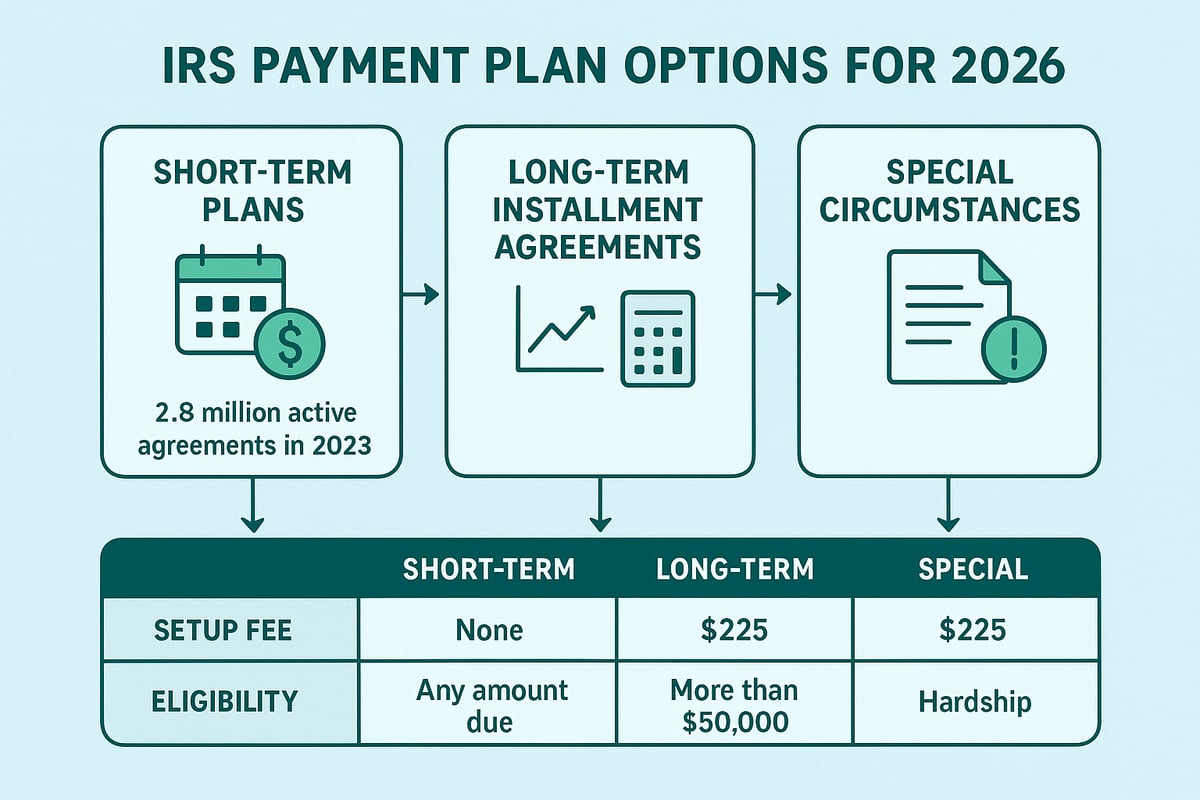

There are two main types of IRS tax payment payment plan options: short-term and long-term installment agreements. Short-term plans last up to 180 days, while long-term plans, also known as installment agreements, can extend over several years. According to recent statistics, over 2.8 million installment agreements were active in 2023, highlighting how common these arrangements have become. The IRS has also introduced “Fresh Start” programs to streamline the process for many taxpayers, making it easier than ever to apply.

Failing to pay your taxes in full can lead to several negative outcomes. Interest accrues daily on unpaid balances, and late payment penalties generally add 0.5 percent per month. If left unresolved, the IRS may garnish your wages, place liens on your property, or even levy your bank account. These consequences make it essential to consider a tax payment payment plan before your situation escalates.

Eligibility for a tax payment payment plan depends on several factors, including the total amount owed and your filing history. For example, a taxpayer who owes $8,000 may qualify for a simple, streamlined agreement with minimal paperwork. In contrast, someone with a $60,000 debt must provide detailed financial disclosures and may be subject to additional scrutiny. To compare your options and understand which plan fits your needs, consult resources like this IRS payment plan guide.

Below is a comparison of short-term and long-term plans:

| Plan Type | Maximum Balance | Duration | Setup Fee | Financial Disclosure |

|---|---|---|---|---|

| Short-Term | $100,000 | Up to 180 days | $0 | No |

| Long-Term | $50,000 ($100k with extra steps) | Over 180 days | $22–$178 | Sometimes required |

Understanding your tax payment payment plan options can empower you to take control of your finances. Whether your debt is large or small, knowing how the process works is the first step toward a resolution.

Types of IRS Payment Plans for 2026

Navigating your tax payment payment plan options for 2026 is crucial if you owe more than you can pay at once. The IRS offers several structured solutions to help taxpayers manage tax debt without risking severe penalties or collection actions. Understanding each tax payment payment plan type will empower you to make the best decision for your financial health.

Short-Term Payment Plans (180 Days or Less)

A short-term tax payment payment plan is ideal for those who can resolve their IRS debt within 180 days. If you owe less than $100,000 in combined tax, penalties, and interest, you likely qualify. This plan requires no setup fee, making it the most affordable entry point for many taxpayers.

Interest and late-payment penalties still accrue while you pay off your balance. However, the absence of a setup fee and the straightforward application process make this tax payment payment plan attractive. You can apply online, by phone, or mail, and detailed financial disclosures are not necessary.

For example, if you have a $3,000 balance and can pay it off over four months, a short-term tax payment payment plan lets you avoid collection actions while minimizing extra costs. In recent years, the IRS has reported increased use of these plans as economic conditions changed and more people sought flexible solutions.

Remember, this option works best if you can pay your tax bill quickly. The faster you resolve your balance, the less you’ll pay in interest and penalties. Always compare your ability to pay to ensure a short-term tax payment payment plan is the right fit.

Long-Term Installment Agreements (Over 180 Days)

If your debt will take longer than 180 days to pay, a long-term tax payment payment plan, known as an installment agreement, may be your best solution. Taxpayers owing up to $50,000 can often use a streamlined process, while higher balances require additional documentation.

There are several types of long-term tax payment payment plan options: Direct Debit Installment Agreements (DDIA), payroll deduction, and standard agreements. Setup fees vary based on your payment method and how you apply, ranging from $22 for online direct debit to $178 for mail or phone applications.

Monthly payments are typically calculated by dividing your total debt by up to 72 months. For instance, a $36,000 balance would require payments of at least $500 per month. If your debt exceeds $50,000, the IRS will ask for detailed financial disclosures and might place a lien on your property.

For more details on plan types, fees, and tips for managing your agreement, visit the IRS payment plans and installment agreements resource. Choosing a long-term tax payment payment plan offers flexibility but can lead to more interest over time. Carefully weigh the pros and cons to protect your finances.

Special Circumstances: High-Balance and Financial Hardship Plans

Some taxpayers face unique challenges, such as owing more than $50,000 or experiencing serious financial hardship. In these cases, a special tax payment payment plan may be necessary. The IRS requires extra steps, including submitting Form 9465 and Form 433-A to disclose your financial situation.

For debts over $50,000, the IRS may request collateral or file a lien. If you demonstrate genuine hardship, you might qualify for a Partial Payment Installment Agreement, allowing you to pay less than the full amount. In severe situations, you can apply for “Currently Not Collectible” status, where the IRS temporarily suspends collection due to your inability to pay.

Consider the example of a taxpayer with $120,000 in debt but limited income. Approval rates for hardship-based tax payment payment plan options are lower, and the IRS requires detailed documentation. In many cases, professional guidance is essential to navigate these complex options.

Securing a special tax payment payment plan can provide relief, but you must be prepared for thorough review and ongoing compliance. Always collect comprehensive records and seek help if your situation is complicated.

Step-by-Step: How to Apply for a Tax Payment Plan in 2026

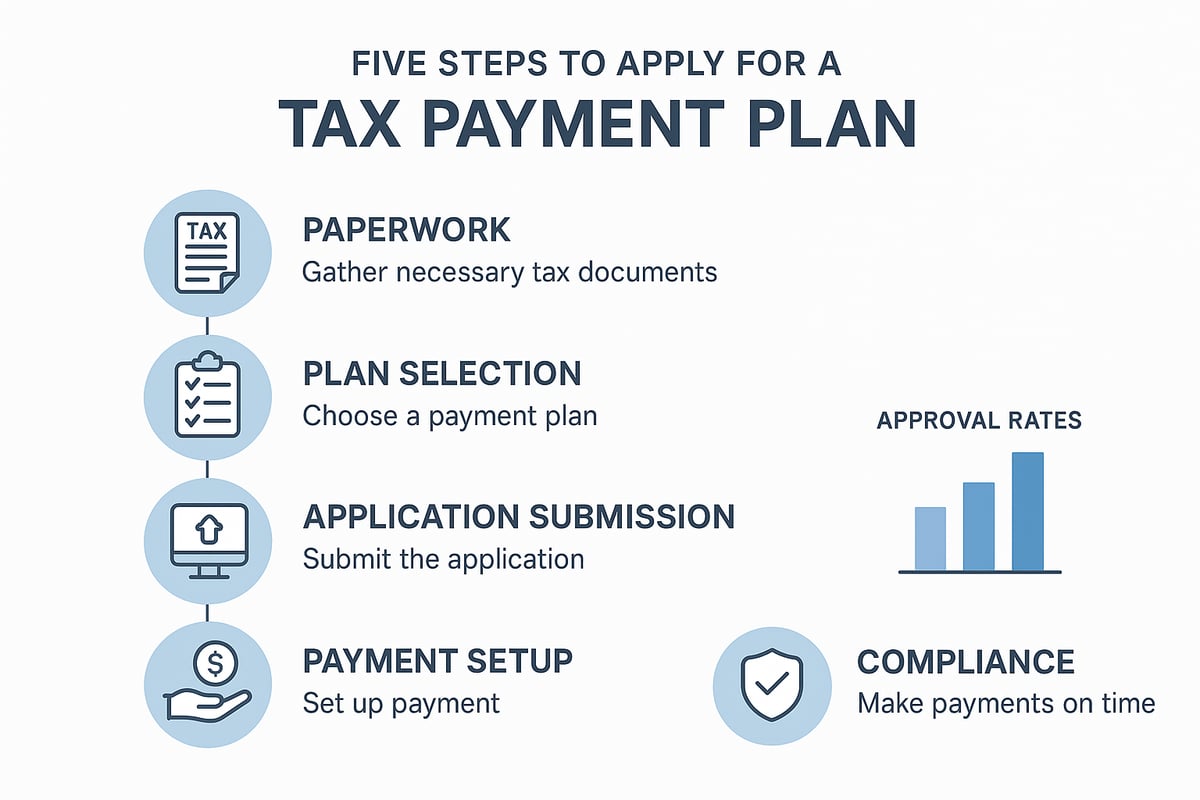

Applying for a tax payment payment plan with the IRS can feel overwhelming, but breaking the process down into clear steps will help you move forward with confidence. Use this guide to organize your documents, select the best plan, and keep your account in good standing.

Step 1: Assess Your Tax Situation

Start by gathering all relevant IRS notices, recent tax returns, and account transcripts. Knowing the total amount you owe, including penalties and interest, is essential before you apply for any tax payment payment plan.

Review your IRS Online Account to see your current balance and payment history. Use the IRS payment calculator to estimate your monthly obligations. Confirm eligibility for each plan type based on your balance and filing status.

If you are unsure about your figures, consult with a tax professional or use IRS resources to double-check your numbers. This upfront clarity will help you avoid surprises during the application process.

Step 2: Choose the Right Plan

Compare short-term and long-term options to decide which tax payment payment plan fits your financial situation. Short-term plans are best if you can pay off your tax debt within 180 days, while long-term installment agreements allow more time but accrue more interest.

Evaluate setup fees, documentation requirements, and payment methods. Consider how each option affects your monthly budget and credit profile. For example, a faster payoff reduces interest costs but may strain your cash flow.

Use the IRS eligibility tool to see which plans you qualify for. Take time to weigh the pros and cons before making your choice, as switching plans later can be complicated.

Step 3: Submit Your Application

Once you have selected a tax payment payment plan, you can submit your application online via IRS.gov, by phone, or by mailing Form 9465. For balances over $50,000, attach Form 433-A to provide detailed financial information.

Have your personal details, tax year, amount owed, and proposed monthly payment ready. Application fees range from $0 for short-term plans to up to $178 for long-term agreements, depending on the payment method and application channel.

Online applications are processed immediately, while mailed forms can take several weeks. For detailed guidance and direct access to IRS forms, visit the Tax resources and forms page. Direct debit is often required for higher balances, so have your bank information available.

Be sure to keep a copy of all forms and confirmation numbers for your records. Double-check all entries to avoid delays or rejections.

Step 4: Set Up and Manage Payments

After approval, set up automatic payments for your tax payment payment plan using direct debit, payroll deduction, check, or credit card. Direct debit minimizes the risk of missed payments and is required for larger debts.

Monitor your payments through your IRS Online Account to ensure they are credited correctly. If your financial situation changes, contact the IRS promptly to adjust your payment amount. Missing payments can lead to plan default and reinstatement fees.

If you switch banks or need to update your information, do so immediately to prevent disruptions. Most plan defaults happen due to missed or late payments, so set reminders and stay proactive.

Staying organized and monitoring your tax payment payment plan will help you maintain compliance and avoid additional penalties.

Step 5: Stay Compliant and Avoid Pitfalls

File all future tax returns on time, as this is required to keep your tax payment payment plan active. Pay any new tax bills promptly or request to add them to your existing agreement.

Watch for IRS notices about your plan status or changes. If you anticipate trouble making payments, contact the IRS before missing a deadline to explore possible options.

Keeping communication open and staying on top of your obligations is the best way to prevent plan termination or collection actions. Proactive management ensures your tax debt remains under control.

Costs, Fees, and Interest: What to Expect

Choosing a tax payment payment plan can help you manage your IRS debt, but understanding the true costs is essential. Every plan comes with setup fees, ongoing interest, and potential penalties. Being informed will help you avoid surprises and make the best financial decision for your situation.

Setup Fees: What You Pay Upfront

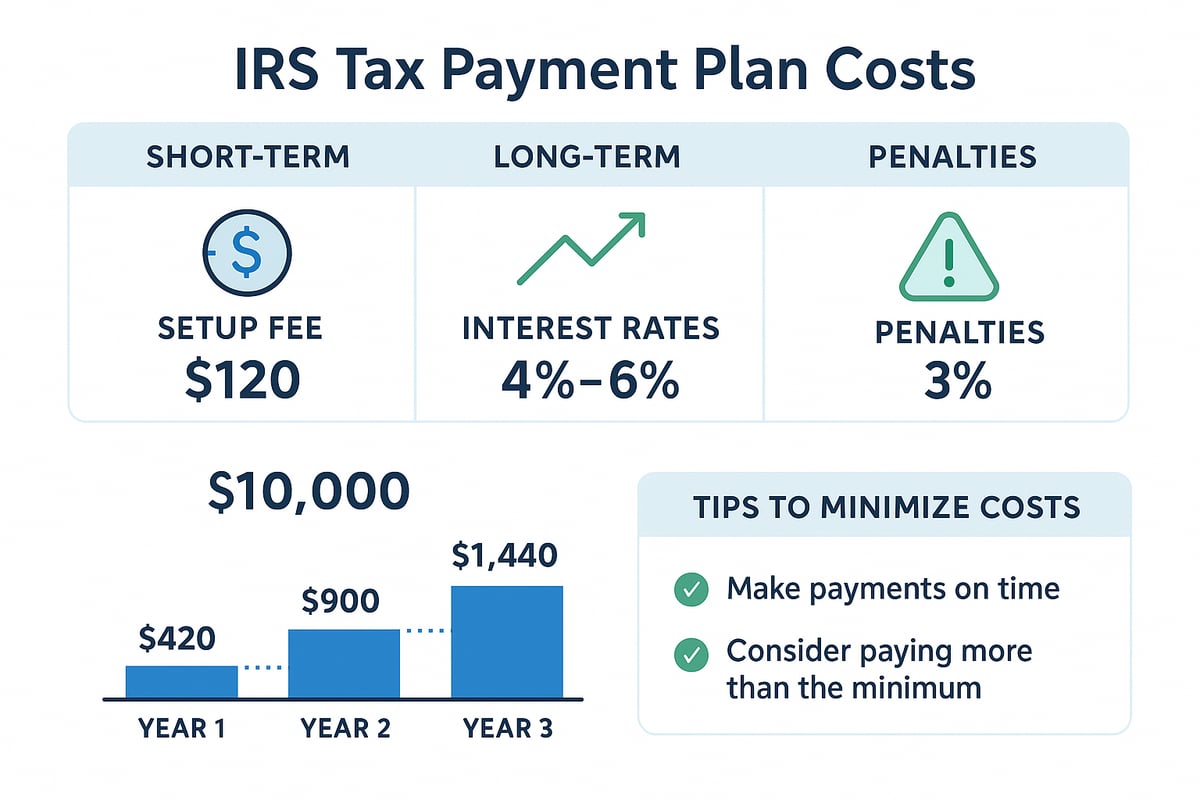

When enrolling in a tax payment payment plan, you may face a setup fee based on the plan and payment method you choose. Short-term plans (180 days or less) have no setup fee, while long-term installment agreements have variable costs. Here is a summary of common fees:

| Plan Type & Payment Method | Application Channel | Setup Fee |

|---|---|---|

| Short-Term (≤180 days) | Online/Phone/Mail | $0 |

| Long-Term, Direct Debit | Online | $22 |

| Long-Term, Non-Direct Debit | Online | $69 |

| Long-Term, Any Method | Phone/Mail | $107–$178 |

Low-income taxpayers may qualify for a reduced or waived setup fee. Always check the latest IRS payment plan options for current details and eligibility.

Interest and Penalty Charges

Interest is a major factor in the cost of any tax payment payment plan. The IRS sets interest rates quarterly; for example, rates were around 8% in 2024, and they compound daily. This means the longer your balance remains, the more you will owe.

In addition to interest, a late payment penalty of 0.5% per month applies until your tax is fully paid. These charges can quickly add up if payments are delayed or missed, so prompt and regular payments are vital for minimizing your total expense.

Total Cost Example and Comparisons

Consider a $10,000 IRS debt repaid over three years using a tax payment payment plan. With compounded interest and penalties, you could pay more than $1,500 extra over the repayment period.

Comparing this to a credit card or personal loan is important. Some credit cards offer promotional 0% APR, potentially saving you interest, but most standard rates exceed IRS rates. Personal loans may be an option if they carry lower rates than a tax payment payment plan, but always factor in fees and your ability to qualify.

Reducing Costs: Smart Strategies

To pay less for your tax payment payment plan, consider these strategies:

- Pay as much upfront as possible to reduce the principal.

- Choose direct debit to lower your setup fee and avoid missed payments.

- Apply for low-income fee waivers if you qualify.

- Always pay more than the minimum monthly amount if possible, which directly cuts down on total interest and penalties.

- Review your plan regularly and adjust payments if your finances improve.

Streamlined plans for balances under $50,000 are often the most cost-effective due to lower fees and simpler approval. Staying proactive and informed will help you manage your tax payment payment plan efficiently and avoid unnecessary expenses.

Eligibility, Approval, and Plan Maintenance

Understanding whether you qualify for a tax payment payment plan is the first step to resolving IRS debt. The IRS requires all applicants to have filed their tax returns up to date, not be in active bankruptcy, and have no recent defaulted agreements. Meeting these basic standards ensures your application will be considered and helps you avoid delays in approval.

Guaranteed and Streamlined IRS Tax Payment Payment Plans

If you owe less than $10,000, you may qualify for a "guaranteed" tax payment payment plan. These plans require that you pay off the full amount within three years, and approval is almost automatic if you meet the criteria. For balances between $10,000 and $50,000, "streamlined" plans allow you to set up an agreement with minimal paperwork and no need for detailed financial disclosure. Both options are designed for quick approval and are ideal if you can commit to timely monthly payments.

| Plan Type | Balance Limit | Docs Needed | Approval Rate |

|---|---|---|---|

| Guaranteed | <$10,000 | Minimal | Very High |

| Streamlined | $10k-$50k | Basic Info | High |

| High-Balance | >$50,000 | Full Fin. | Lower |

High-Balance and Hardship Plans: Extra Steps

For those with tax debts over $50,000, the IRS enforces stricter requirements for a tax payment payment plan. You will need to submit detailed financial disclosures, such as Form 433-A, and may face the filing of a federal tax lien. Approval rates are lower for these plans, especially if you request partial payment due to financial hardship. The IRS reviews your income, expenses, assets, and liabilities carefully before approving any arrangement in this category. Professional help is often recommended for complex situations.

Maintaining Your Tax Payment Payment Plan

Once your tax payment payment plan is active, you must make every payment on time and file all future tax returns promptly. Missing payments or failing to submit new returns can result in plan default, which may lead to additional penalties or aggressive IRS collection actions. If you default, the IRS may terminate the agreement and resume collection, including levies or liens. For example, a taxpayer who misses two consecutive payments might lose their plan and face immediate wage garnishment. If you encounter difficulties, contact the IRS or review Tax relief services overview for guidance on next steps and reinstatement options.

Strategies to Minimize Interest, Penalties, and Tax Debt

Facing a tax payment payment plan can feel overwhelming, but you have powerful options to reduce the final cost of your tax debt. By using smart strategies, you can limit interest, cut penalties, and even prevent future tax problems.

Pay More Upfront to Cut Interest

The fastest way to save money on a tax payment payment plan is by paying as much as you can upfront. Every dollar you pay immediately starts working for you, reducing the principal that interest and penalties are calculated on. Even a modest extra payment can significantly lower your total cost over time.

If you have savings, or can temporarily adjust your budget, consider making a larger initial payment. This not only shortens your repayment period but also demonstrates good faith to the IRS.

Explore Lower-Cost Alternatives

Sometimes, the IRS interest rate may be higher than what you could get with a 0 percent APR credit card or a low-interest personal loan. Compare the total costs carefully before deciding. Using a short-term loan or balance transfer card can help you pay off your tax payment payment plan faster, saving on compounding interest.

The IRS also offers several options to help taxpayers pay their tax bill, including payment plans, penalty relief, and hardship programs. Review all available alternatives to find the best fit for your situation.

Seek Penalty Relief and Settlements

If you have a valid reason for falling behind, you may qualify for penalty abatement. Common reasons include illness, natural disasters, or other circumstances beyond your control. To request penalty relief, submit a written explanation when you set up your tax payment payment plan or contact the IRS directly.

For severe financial hardship, consider applying for an Offer in Compromise (OIC). This allows you to settle your tax debt for less than the full amount owed, if you can prove that paying in full would cause significant hardship. The IRS approves OIC applications selectively, but for those who qualify, the average settlement is only 20 to 30 percent of the original debt.

Prevent Future Tax Debt

To ensure you do not end up with another tax payment payment plan in the future, review your tax withholding or estimated payments. Adjust them as needed so you are not underpaying throughout the year.

If you are unable to pay anything at all, you might qualify for “Currently Not Collectible” status. In this case, the IRS temporarily suspends collection activities, giving you time to recover financially. Documentation is required, and interest continues to accrue, but this can offer essential breathing room.

Real-Life Example and IRS Data

Suppose you owe $5,000 in penalties. By successfully requesting penalty abatement due to a documented medical emergency, your tax payment payment plan could shrink by thousands. According to IRS data, the average Offer in Compromise settles at about one quarter of the original debt for qualifying taxpayers.

Using these strategies can help you take control, reduce financial stress, and reach a faster resolution with the IRS.

Resources and Support for Taxpayers

Navigating a tax payment payment plan can feel overwhelming, but you are not alone. There are many resources designed to help taxpayers understand their options, take action, and stay compliant. Whether you need basic guidance or expert representation, the right support can make all the difference.

IRS & Government Resources

The IRS provides several tools to help you manage your tax payment payment plan. Start with the IRS Online Account, where you can view your balance, set up or manage a payment plan, and update personal information. This portal makes it easy to track payments and stay up to date.

If you have questions or complex issues, call the IRS helplines or reach out to the Taxpayer Advocate Service for independent assistance. They can help resolve delays, errors, or disputes. The IRS also offers payment calculators and detailed FAQs to guide you through each step.

Understanding IRS collection actions is critical, especially if you are worried about levies or wage garnishment. Learn what could happen if you default by reviewing this IRS bank account levy resource. Knowing your rights and obligations can help you avoid serious consequences.

Nonprofit & Professional Support

If your tax payment payment plan situation is complicated, nonprofit organizations offer valuable assistance. Free tax clinics, such as Low Income Taxpayer Clinics (LITCs), provide help to those who qualify based on income. These clinics can represent you before the IRS, negotiate on your behalf, or help you apply for relief programs.

Nonprofit credit counseling agencies can also advise on budgeting and debt management strategies if you are balancing multiple obligations. When your tax debt is high, your finances are complex, or you face audit risk, consider seeking a qualified tax professional. They can prepare required forms, represent you during IRS negotiations, and ensure your tax payment payment plan is set up correctly.

For instance, if you owe a large balance and need to submit detailed financial disclosures, a professional can help avoid errors that might delay approval or trigger collection actions.

Forms, Tools & Warnings

Being organized is key to a successful tax payment payment plan. Keep track of essential IRS forms, such as:

| Form Name | Purpose |

|---|---|

| 9465 | Installment Agreement Request |

| 433-A/B/F | Financial Disclosure (for higher balances) |

Use the IRS payment calculators to estimate monthly payments and total costs. These tools can help you choose the best plan for your situation.

Be wary of tax relief scams that promise quick fixes for a fee. Legitimate help will never pressure you or ask for payment upfront. Always verify credentials and use official IRS resources or trusted nonprofit organizations.

For more guidance, consult IRS FAQs and guides, or seek support from reputable advisors. With the right information and support, you can navigate your tax payment payment plan successfully and regain control of your finances.

Navigating IRS payment plans can feel overwhelming, especially with so many options and details to consider for 2026. You deserve clarity and confidence when managing your tax debt, and you do not have to do it alone. If you are unsure which path best protects your finances or you are facing high balances, legal concerns, or just need expert guidance, we are here to help you find real solutions. Let’s work together to reduce your stress and secure a manageable plan for your future. Contact us for a free consultation.