Managing tax debt through an installment agreement with the Internal Revenue Service provides relief for taxpayers who cannot pay their full balance immediately. Once you've established your payment plan, understanding how to pay my IRS installment efficiently becomes essential to maintaining compliance and avoiding additional penalties. The payment process involves multiple options, deadlines, and potential pitfalls that every taxpayer should navigate carefully to protect their financial standing and prevent enforcement actions.

Understanding Your IRS Installment Agreement Structure

When you enter into an installment agreement with the IRS, you're committing to a legally binding payment schedule that requires consistent monthly payments until your tax debt is fully satisfied. The agreement specifies your payment amount, due date, and the total balance including any accrued interest and penalties that continue to accumulate until the debt is paid in full.

Types of Installment Agreements and Payment Requirements

The IRS offers several installment agreement types, each with distinct payment structures and obligations:

- Guaranteed Installment Agreements for balances under $10,000 with repayment within three years

- Streamlined Installment Agreements for balances up to $50,000 with repayment within 72 months

- Partial Payment Installment Agreements where monthly payments don't cover the full balance before the collection statute expires

- Non-Streamlined Installment Agreements for larger balances requiring detailed financial disclosure

Your monthly payment amount depends on your agreement type, total debt, and financial circumstances. The IRS payment plans page provides detailed eligibility criteria for each agreement category, helping you understand which structure applies to your situation.

Primary Methods to Pay My IRS Installment

The IRS provides multiple payment channels designed to accommodate different preferences and circumstances. Selecting the right method ensures timely payments while minimizing fees and processing delays.

Direct Debit (Automatic Withdrawal)

Direct debit represents the most reliable method to pay my IRS installment, automatically withdrawing your monthly payment from your designated checking or savings account on your specified due date. This approach eliminates the risk of missed payments and qualifies you for reduced setup fees when establishing your agreement.

Benefits of Direct Debit:

- Automatic compliance with payment deadlines

- Reduced setup fee ($31 versus $130 for non-direct debit agreements in 2026)

- Lower risk of default due to forgotten payments

- No monthly transaction fees

When setting up direct debit through the online payment agreement application, you'll provide your bank routing number, account number, and preferred withdrawal date. The IRS typically processes withdrawals on the same date each month, providing predictable cash flow management.

IRS Direct Pay Online Portal

The IRS Direct Pay system allows you to make individual installment payments directly from your bank account without fees or registration requirements. This free service processes payments immediately and provides instant confirmation of your transaction.

To pay my IRS installment through Direct Pay:

- Visit the IRS Direct Pay website and select "Installment Agreement" as your payment reason

- Enter your tax year, Social Security number or Employer Identification Number, and address

- Verify your identity through information from your tax return

- Select your bank account and confirm payment details

- Save your confirmation number for your records

This method works best for taxpayers who prefer manual control over payment timing or those who want to make payments larger than their minimum monthly amount to reduce interest accumulation.

Electronic Federal Tax Payment System (EFTPS)

EFTPS provides a secure government payment portal that processes tax payments with next-day settlement. After enrolling and receiving your PIN by mail, you can schedule payments up to 365 days in advance, making it useful for planning multiple installment payments simultaneously.

| Payment Method | Processing Time | Fees | Best For |

|---|---|---|---|

| Direct Debit | Automatic on due date | None (reduced setup fee) | Set-it-and-forget-it reliability |

| IRS Direct Pay | Same day | None | One-time control and flexibility |

| EFTPS | Next business day | None | Advanced scheduling needs |

| Debit/Credit Card | Same day | 1.85%-1.98% | Emergency or reward points |

| Check/Money Order | 5-7 business days | None | No bank account access |

Credit and Debit Card Payments

Third-party processors accept credit and debit card payments for IRS installment agreements, though convenience fees ranging from 1.85% to 1.98% of the payment amount apply. While expensive for regular payments, this option provides value in specific circumstances such as earning credit card rewards or managing temporary cash flow constraints.

The IRS partners with several approved payment processors that charge different fee structures. Calculate whether rewards or benefits offset the processing fee before using this method to pay my IRS installment regularly.

Mail and Physical Payments

Traditional payment methods remain available for taxpayers who prefer or require non-electronic options. When paying by check or money order, include your name, address, Social Security number, tax year, and the notation "Installment Agreement Payment" on your payment instrument.

Mail payments to the address specified on your installment agreement notice, allowing adequate time for postal delivery and IRS processing. Payments are credited on the date received, not the postmark date, making this method risky for tight deadlines.

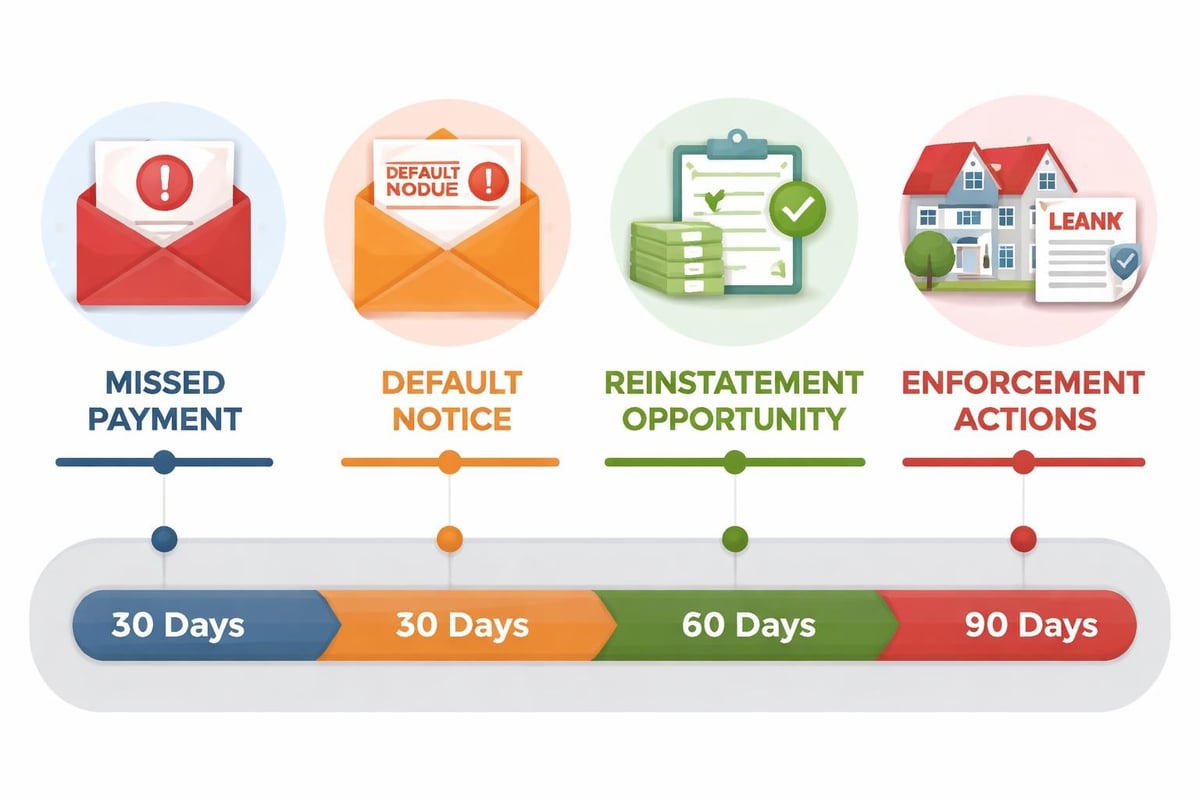

Managing Payment Deadlines and Avoiding Default

Your installment agreement specifies the exact date your monthly payment must be received by the IRS. Missing even a single payment or paying less than the agreed amount can trigger default proceedings, potentially leading to aggressive collection actions.

Default Triggers and Consequences

An installment agreement enters default status when:

- You miss a monthly payment deadline

- You submit a payment for less than the agreed amount

- You accrue new tax debt while the agreement is active

- You fail to file required tax returns by their deadlines

Default consequences escalate quickly. The IRS can immediately file a Notice of Federal Tax Lien if one isn't already in place, levy your bank accounts, garnish wages, or seize assets. Interest and penalties continue accumulating on the full balance, and you'll need to reapply and pay additional fees to reinstate the agreement.

Setting Up Payment Reminders

Establishing systematic reminders prevents accidental missed payments when you manually pay my IRS installment each month. Consider these strategies:

- Set recurring calendar alerts 5-7 days before your due date

- Create automatic email or text notifications through your bank

- Link payments to regular monthly events like paycheck deposits

- Maintain a dedicated checklist for monthly financial obligations

For taxpayers with variable income or irregular cash flow, scheduling payments immediately after receiving income ensures funds are available when needed. The various payment plan options the IRS offers include flexibility for different financial situations.

Handling Financial Hardship During Agreement

Temporary financial difficulties don't automatically terminate your installment agreement. If you cannot pay my IRS installment in a given month due to unexpected circumstances, contact the IRS immediately to discuss modification options before the payment deadline passes.

The IRS may approve:

- Temporary payment reduction or suspension for defined hardship periods

- Extension of the agreement term to reduce monthly payment amounts

- Reclassification to a different agreement type based on updated financial information

- Currently Not Collectible status if financial circumstances warrant suspension

Proactive communication demonstrates good faith and often results in more favorable outcomes than simply allowing the agreement to default.

Optimizing Your Installment Payment Strategy

Strategic payment management reduces total interest costs and accelerates debt elimination while maintaining compliance with your agreement terms.

Making Additional Principal Payments

Your installment agreement sets a minimum monthly payment, but nothing prevents you from paying larger amounts or making extra payments. Additional payments apply directly to your principal balance, reducing accumulated interest charges over the agreement's life.

When you pay my IRS installment with extra funds, specify that the additional amount should apply to your oldest tax year first unless you prefer a different allocation. This approach minimizes interest on the highest-balance periods.

Calculate potential savings using this approach:

- Identify your current monthly payment and remaining agreement term

- Calculate total interest that will accrue under the current payment schedule

- Determine how much you can afford beyond the minimum payment

- Project the accelerated payoff date and reduced total interest

- Compare total costs between minimum payments and accelerated payments

Even modest increases to your monthly payment can generate significant savings over multi-year agreements.

Coordinating Payments with Tax Refunds

If you expect federal or state tax refunds while maintaining an installment agreement, the IRS automatically applies your federal refund to your outstanding balance. This mandatory offset reduces your principal but doesn't count as a monthly installment payment.

Strategic refund coordination includes:

- Adjusting withholding to reduce refunds and increase monthly cash flow for larger regular payments

- Planning for refund offset when budgeting annual tax obligations

- Making voluntary payments from state refunds to further reduce balance

- Recalculating your agreement term based on refund applications

Some taxpayers prefer maximizing refunds to make large annual principal reductions, while others optimize withholding for consistent monthly payment capacity. Your preference depends on your financial discipline and cash flow stability.

Monitoring Your Balance and Interest Accumulation

The IRS continues charging interest and certain penalties on your unpaid balance throughout your installment agreement period. Current interest rates adjust quarterly based on federal short-term rates plus three percentage points for individual taxpayers.

Request updated account transcripts quarterly to verify:

- Accurate application of your payments to principal and interest

- Current remaining balance across all tax years

- Interest rate and daily interest charges

- Penalty assessments and compliance status

These transcripts identify discrepancies early and help you project your exact payoff date based on your payment schedule. Understanding precisely how much you owe at any given time empowers better financial planning and payment allocation decisions.

Special Considerations for Business Tax Installment Agreements

Business taxpayers face unique challenges when maintaining installment agreements for employment taxes, excise taxes, or corporate income taxes. These agreements often involve trust fund taxes that carry additional legal implications and stricter compliance requirements.

Trust Fund Recovery Penalties

When businesses fall behind on employment taxes, the IRS can assess Trust Fund Recovery Penalties against responsible individuals who willfully failed to collect or pay over withheld employee taxes. These penalties make company officers personally liable for the trust fund portion of unpaid employment taxes.

If your installment agreement includes trust fund taxes, the IRS may require:

- Separate agreements for the trust fund and employer portions

- Higher minimum monthly payments to satisfy trust fund portions within specific timeframes

- Personal guarantees from responsible officers

- Subordination of certain business assets as security

Understanding these distinctions ensures you structure your agreement appropriately and avoid personal liability exposure for business tax debts.

Maintaining Current Tax Obligations

Business installment agreements require strict compliance with all current tax filing and payment obligations while repaying past debt. You must timely file all required returns and pay current taxes in full to avoid agreement default.

Compliance checklist for business agreements:

- File all quarterly employment tax returns (Forms 941) by deadlines

- Make all required federal tax deposits for current payroll periods

- Submit annual business returns (1120, 1065, etc.) on time

- Pay estimated taxes for current year obligations

- Report and pay all excise taxes when due

Failure to remain current on any tax type automatically defaults your installment agreement for past liabilities. The Taxpayer Advocate Service offers guidance on installment agreement requirements including business-specific considerations.

Modifying or Terminating Your Installment Agreement

Circumstances change throughout multi-year payment plans, sometimes requiring agreement modifications or early termination. Understanding your options helps you adapt to evolving financial situations.

Requesting Agreement Modifications

The IRS considers modification requests when your financial situation changes significantly. Valid reasons for modification include:

- Income reduction due to job loss or business decline

- Increased expenses from medical emergencies or family changes

- Ability to pay off the balance early with lump sum settlement

- Need for extended repayment terms due to financial hardship

Submit modification requests in writing with current financial documentation using Form 9465 or through your online account. The IRS reviews your updated financial information and may approve reduced payments, extended terms, or temporary suspension during hardship periods.

Be aware that requesting modification doesn't automatically protect you from default if you cannot make your current payment while the request is pending. Continue making agreed payments until you receive written approval of modified terms.

Paying Off the Agreement Early

You can eliminate your installment agreement at any time by paying the remaining balance in full. Early payoff benefits include:

- Immediate cessation of interest accumulation

- Elimination of monthly payment obligations

- Potential release of tax liens within 30 days

- Improved ability to secure credit and financing

Before paying off your agreement early, request a current payoff quote from the IRS to determine the exact amount needed. Interest accrues daily, so the balance increases between your quote date and payment date. Pay slightly more than the quoted amount to ensure full satisfaction, with any overpayment refunded by the IRS.

Reinstating a Defaulted Agreement

If your agreement defaults due to missed payments or non-compliance, you can potentially reinstate it by:

- Paying all missed payments plus associated penalties

- Submitting a reinstatement request explaining the default circumstances

- Demonstrating ability to maintain future payments

- Paying a reinstatement fee (currently $89 in 2026)

The IRS isn't required to approve reinstatement requests and may instead require a new agreement application with updated financial disclosure. Reinstatement works best when default results from temporary circumstances that have been resolved.

Technology Tools for Managing Installment Payments

Modern tax management tools simplify the process to pay my IRS installment and maintain compliance throughout your agreement term.

IRS Online Account Features

Your IRS online account provides comprehensive installment agreement management capabilities:

| Feature | Function | Benefit |

|---|---|---|

| Payment History | View all payments applied to your account | Verify proper crediting and catch errors |

| Balance Information | Check current balance and interest charges | Track progress toward payoff |

| Agreement Details | Review payment amount and due dates | Confirm compliance requirements |

| Secure Messaging | Contact IRS about agreement questions | Document communications |

| Payment Scheduling | Set up automatic or one-time payments | Ensure timely payments |

Accessing your online account regularly keeps you informed about your agreement status and helps identify potential issues before they cause defaults.

Third-Party Tax Software Integration

Many tax preparation and financial management software platforms integrate with IRS payment systems, allowing you to pay my IRS installment directly through your budgeting or accounting software. These integrations can:

- Automatically record payments in your financial records

- Generate reminders based on your agreement schedule

- Track tax debt alongside other financial obligations

- Provide reports on total interest paid and remaining balance

Evaluate integration options based on your existing financial management systems and technical comfort level. NerdWallet provides practical guidance on setting up and managing IRS payment plans using various technological approaches.

Mobile Payment Options

IRS2Go, the official IRS mobile application, enables you to make installment payments from your smartphone or tablet. The app provides convenient access to payment functions while away from your computer, helping you meet deadlines even during travel or other disruptions to your normal routine.

Mobile payment features include:

- Direct Pay access for immediate bank account payments

- Payment history review and confirmation

- Refund status tracking for offset monitoring

- Tax form access and account management

Download IRS2Go from your device's app store and set up biometric authentication for secure, quick access when you need to pay my IRS installment on short notice.

Professional Assistance for Complex Installment Situations

While many taxpayers successfully manage installment agreements independently, certain situations benefit from professional tax resolution assistance.

When to Seek Professional Help

Consider engaging tax professionals when:

- Your installment agreement includes multiple tax years with complex allocation issues

- You're negotiating agreements for business employment taxes with trust fund implications

- The IRS has proposed levies or liens despite your payment efforts

- You need to modify agreements multiple times due to ongoing financial challenges

- Your situation involves both federal and state tax installment agreements requiring coordination

- You're considering alternatives like Offers in Compromise or Currently Not Collectible status

Tax resolution specialists understand IRS procedures and can negotiate more effectively on your behalf, particularly in complex scenarios involving financial hardship or disputed liabilities. Professional representation ensures you understand all available options and select the optimal strategy for your specific circumstances.

Enrolled Agents and Tax Attorneys

Enrolled agents and tax attorneys possess specialized credentials for representing taxpayers before the IRS. These professionals can:

- Negotiate installment agreement terms based on detailed financial analysis

- Represent you in communications with IRS revenue officers

- Appeal unfavorable determinations or default decisions

- Coordinate state and federal payment plans

- Advise on tax implications of payment strategies

When selecting a tax professional, verify credentials through the IRS Office of Professional Responsibility and check for any disciplinary actions or complaints with state licensing boards.

Record Keeping and Documentation Requirements

Maintaining thorough records throughout your installment agreement protects you in case of disputes and facilitates accurate financial reporting.

Essential Documents to Maintain

Organize and preserve these critical documents for the duration of your agreement plus at least three years after final payment:

- Original installment agreement notice with terms and conditions

- Payment confirmations for every installment payment made

- Bank statements showing debit transactions for each payment

- Correspondence with the IRS regarding the agreement

- Account transcripts showing balance and payment application

- Tax returns filed during the agreement period

- Financial statements submitted with agreement applications or modifications

Store these records in both physical and digital formats, with backups in secure, separate locations. Well-organized documentation becomes invaluable if the IRS claims you missed payments or failed to comply with agreement terms.

Payment Confirmation and Verification

Every time you pay my IRS installment, save the confirmation number, receipt, or transaction record provided by your payment method. These confirmations serve as proof of payment if the IRS fails to properly credit your account.

Document each payment with:

- Payment date and time

- Payment method used

- Confirmation or transaction number

- Amount paid

- Tax period applied to

- Any correspondence reference numbers

If you discover a payment wasn't properly credited, contact the IRS immediately with your confirmation documentation. Resolution becomes significantly easier when you can provide specific transaction details rather than relying on IRS records alone.

State Tax Installment Agreements and Coordination

Many taxpayers with federal installment agreements also owe state taxes requiring separate payment arrangements. Coordinating both obligations prevents conflicts and cash flow problems.

Managing Multiple Agreements Simultaneously

Federal and state tax agencies operate independently, requiring separate applications and payments for installment agreements. When juggling multiple agreements:

- Stagger payment dates to align with income receipt patterns

- Prioritize agreements with stricter enforcement policies

- Allocate unexpected funds based on interest rates and penalty structures

- Monitor both federal and state compliance requirements separately

- Maintain distinct record-keeping systems for each agreement

Some states model their installment programs on federal guidelines, while others impose unique requirements. Research your specific state's policies through their revenue department website or consult with tax professionals familiar with your jurisdiction.

Refund Offset Coordination

Both federal and state agencies can offset tax refunds to satisfy installment agreement balances. This means:

- Your federal refund applies to federal tax debt automatically

- State refunds may offset either state or federal debt depending on reciprocity agreements

- Simultaneous offsets can eliminate expected refund entirely

- Offset applications may not count as regular installment payments

Plan for potential offsets when budgeting annual tax obligations and don't rely on refunds for other financial commitments while installment agreements remain active.

Impact on Credit and Financial Standing

IRS installment agreements affect your broader financial profile beyond just satisfying tax obligations.

Tax Liens and Credit Reporting

The IRS may file a Notice of Federal Tax Lien even after approving your installment agreement, particularly for balances exceeding $10,000. These liens:

- Appear on public records and may impact credit reports

- Attach to all your current and future property

- Create priority claims for IRS over other creditors

- Complicate real estate transactions and refinancing

Under certain circumstances, the IRS withdraws liens after agreement completion or considers lien subordination during the agreement period. Request lien withdrawal within 30 days of final payment using Form 12277.

The installment agreement itself doesn't appear on credit reports, but the underlying tax lien does. This distinction means maintaining your agreement successfully prevents further credit damage even though the lien remains visible to creditors.

Financial Disclosures and Loan Applications

When applying for mortgages, business financing, or other credit during an installment agreement period, you'll typically need to disclose the tax debt and payment arrangement. Lenders evaluate:

- Your payment history on the installment agreement

- Remaining balance and monthly payment obligation

- Impact on debt-to-income ratios

- Risk of future liens or levies

Demonstrating consistent compliance with your agreement improves lender confidence. Provide documentation showing your payment history, current balance, and remaining term to help underwriters accurately assess your financial position.

Successfully managing your IRS installment agreement requires understanding payment methods, maintaining compliance, and adapting to changing circumstances throughout the repayment period. Whether you choose automatic withdrawals, manual payments, or professional assistance, consistent attention to deadlines and obligations protects you from default and enforcement actions. When tax debt becomes overwhelming or installment agreements prove insufficient for your financial situation, CLAW Tax Group provides experienced representation to negotiate payment arrangements, explore alternative resolution options, and defend against aggressive IRS collection actions. Their tax resolution specialists work directly with the IRS on your behalf to structure sustainable payment solutions that protect your assets while resolving outstanding tax obligations.