Falling behind on tax obligations creates mounting problems that compound with each passing year. Whether due to financial hardship, life changes, or simple procrastination, unfiled tax returns represent a serious issue that requires immediate attention. IRS back tax filing involves submitting returns for previous years when you failed to file by the original deadline, and understanding this process is crucial for regaining compliance and avoiding severe consequences. The IRS maintains the authority to pursue collection actions, impose significant penalties, and even initiate criminal proceedings against taxpayers who neglect their filing obligations. Taking action now can help minimize damage and create a pathway toward financial stability.

Understanding IRS Back Tax Filing Requirements

The IRS generally requires taxpayers to file returns for at least the past six years to achieve full compliance, though the agency technically has no statute of limitations on assessing taxes when returns remain unfiled. This means the government can pursue collection indefinitely until you submit required documentation.

Filing obligations depend on your income level and filing status. For 2026, these thresholds vary significantly based on age, dependency status, and income type. Even if you earned below the filing threshold in previous years, you might still want to file if you're entitled to refunds.

Who Must File Back Tax Returns

Several categories of taxpayers face mandatory filing requirements:

- Self-employed individuals who earned $400 or more in net self-employment income

- Taxpayers whose gross income exceeded the standard deduction for their filing status

- Individuals who owe special taxes such as household employment taxes or alternative minimum tax

- Anyone who received distributions from health savings accounts or retirement plans

The IRS prioritizes recent years when pursuing unfiled returns. While they can theoretically demand returns from any year, practical enforcement typically focuses on the most recent six years. However, certain situations-like suspected fraud or substantial income-may trigger investigations extending further back.

Penalties and Consequences of Unfiled Returns

The financial impact of failing to file extends far beyond the original tax owed. IRS penalties create layers of additional debt that grow exponentially over time, transforming manageable obligations into overwhelming burdens.

Failure-to-File Penalty Structure

The IRS assesses a failure-to-file penalty of 5% of the unpaid taxes for each month the return is late, capped at 25% of the total tax due. This penalty alone can increase your debt by one-quarter within just five months.

When both failure-to-file and failure-to-pay penalties apply simultaneously, the IRS reduces the failure-to-file penalty by the failure-to-pay amount. The failure-to-pay penalty equals 0.5% of unpaid taxes per month, also capped at 25%.

| Penalty Type | Monthly Rate | Maximum Penalty | Notes |

|---|---|---|---|

| Failure to File | 5% | 25% | Based on unpaid tax amount |

| Failure to Pay | 0.5% | 25% | Continues until balance paid |

| Combined | 4.5% + 0.5% | 47.5% total | When both apply simultaneously |

| Interest | Variable (8% in 2026) | No cap | Compounds daily |

Interest compounds daily on both the original tax and accumulated penalties. This creates a snowball effect where debts grow faster than many taxpayers can manage through standard payment methods.

Beyond Financial Penalties

Non-filing consequences extend into serious legal territory. The IRS can file a substitute for return (SFR) on your behalf, typically calculating taxes using the least favorable filing status and disallowing most deductions. These SFRs almost always result in higher tax assessments than properly prepared returns.

Criminal prosecution remains possible for willful tax evasion, though the IRS reserves this for egregious cases. More commonly, unfiled returns trigger aggressive collection actions including wage garnishment, bank levies, and property liens that devastate credit ratings and financial stability.

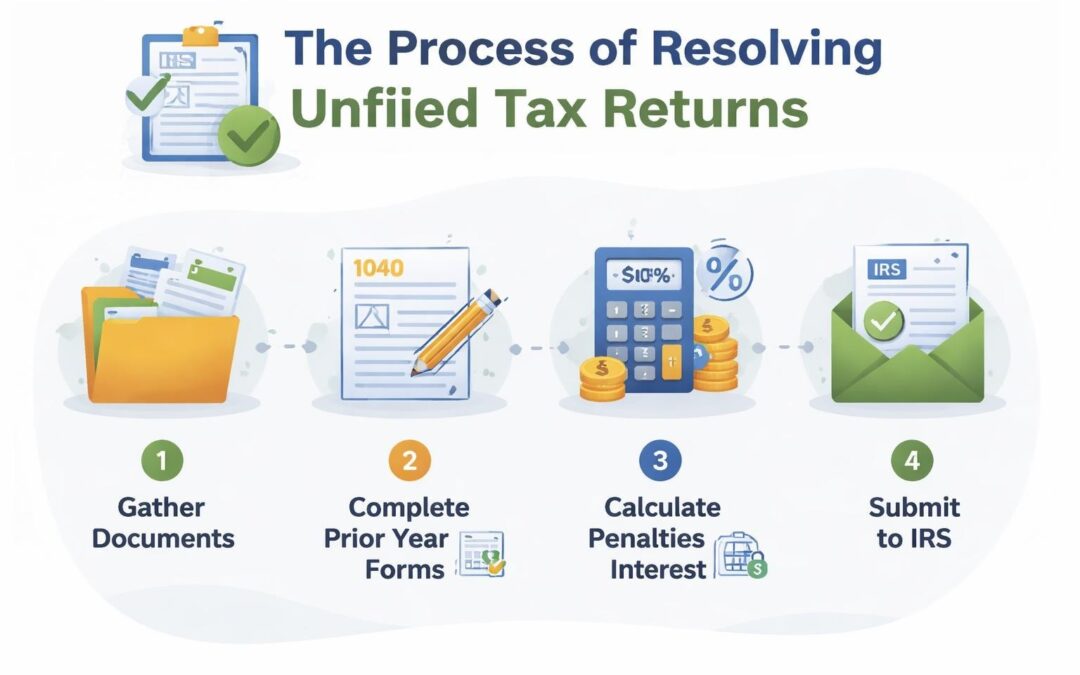

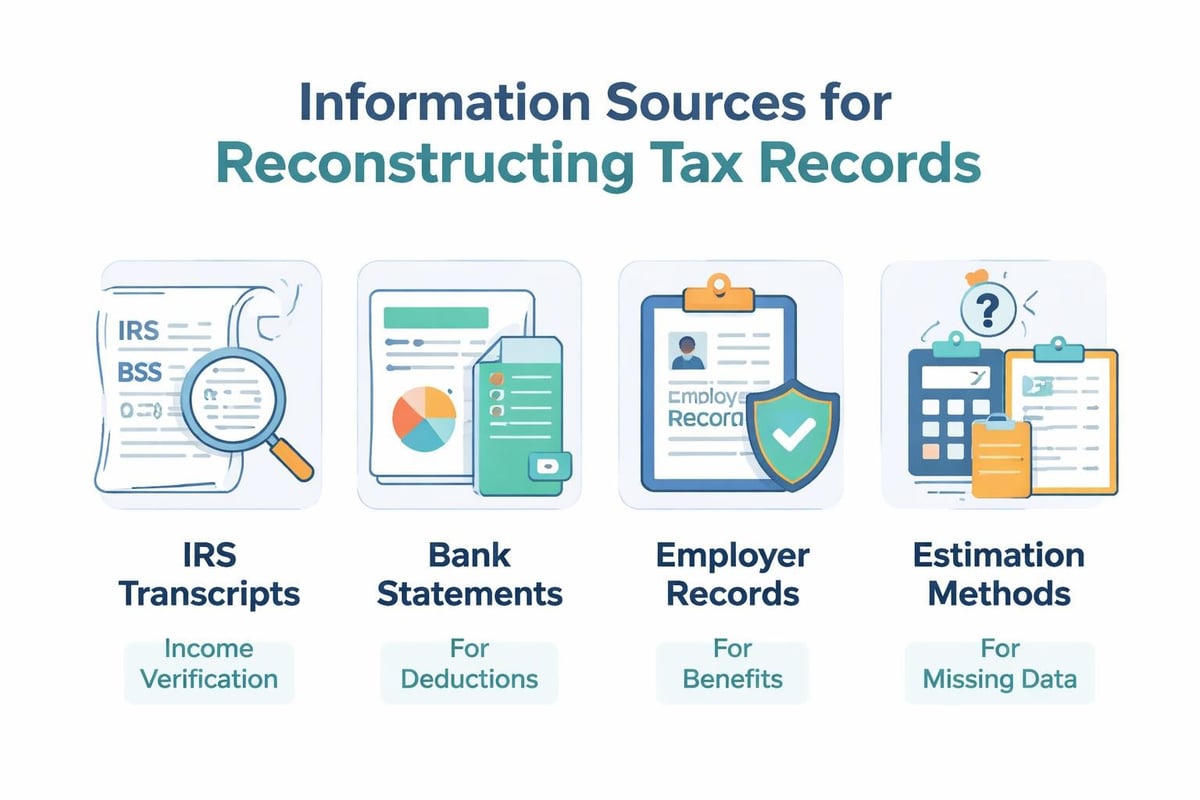

Gathering Documentation for Back Tax Filing

Reconstructing financial records from previous years presents one of the most challenging aspects of irs back tax filing. Systematic organization and resourcefulness help overcome missing documentation obstacles.

Obtaining IRS Transcripts

The IRS maintains records of income reported by employers, banks, and other entities through information returns. Request wage and income transcripts for each year you need to file. These transcripts show:

- W-2 wage statements from employers

- 1099 forms reporting interest, dividends, and independent contractor income

- 1098 forms showing mortgage interest and student loan interest

- Any other third-party reported income

Account transcripts provide additional details about previous interactions with the IRS, including any substitute returns filed on your behalf and penalties already assessed.

Reconstructing Deductions and Credits

While income documentation often comes from IRS records, proving deductions requires your own record-keeping. Contact banks for statements showing mortgage payments, property taxes, and charitable contributions. Healthcare providers can supply medical expense documentation, and employers may maintain records of retirement contributions.

When precise records are unavailable, reasonable estimation based on patterns and available partial documentation becomes necessary. The IRS allows reconstructed records when taxpayers demonstrate good faith efforts to comply.

Filing Procedures and Best Practices

Successfully completing irs back tax filing requires attention to specific procedures that differ from current-year returns. Using correct forms and following proper submission protocols prevents rejection and delays.

Selecting Appropriate Tax Forms

Each tax year requires the forms applicable during that specific period. Tax laws change annually, so 2022 returns require 2022 forms, not current versions. The IRS maintains an archive of prior-year forms on its website, allowing taxpayers to download historically accurate documents.

- Identify the correct tax year form – Never use current-year forms for previous years

- Calculate using that year's tax tables – Tax rates and brackets change annually

- Apply that year's standard deduction amounts – These amounts adjust for inflation yearly

- Claim credits available in that specific year – Some credits expire or modify over time

- Sign and date the return accurately – Include the actual date you're filing, not the original due date

Mail back tax returns to the designated IRS address for your state, separate from any current-year returns. Never e-file multiple years simultaneously, as the IRS system rejects duplicate electronic submissions.

Payment Strategies for Back Taxes

You're not required to pay the full balance when filing, though including payment reduces penalties and interest. Several resolution options exist for taxpayers who cannot afford immediate full payment.

Installment agreements allow monthly payments spread over time. Currently Not Collectible status temporarily suspends collection when you demonstrate genuine financial hardship. Offers in Compromise potentially settle debts for less than the full amount when collectibility is doubtful.

Understanding authoritative tax references helps ensure your filing approach aligns with IRS regulations and maximizes available relief options.

Resolution Options for Overwhelming Back Tax Debt

When irs back tax filing reveals debts exceeding your ability to pay, specialized resolution programs provide pathways forward. These options require careful analysis and often benefit from professional representation.

Offers in Compromise

An Offer in Compromise (OIC) allows qualifying taxpayers to settle their tax debt for less than the full amount owed. The IRS accepts offers when the amount represents the most they can reasonably collect within the remaining statute of limitations.

Qualifying for an OIC requires demonstrating doubt about collectibility or doubt about the liability itself. The IRS examines your income, expenses, asset equity, and future earning potential. Most offers fail because taxpayers either don't qualify financially or submit incomplete applications.

Installment Agreements

Installment agreements provide structured payment plans ranging from short-term arrangements (120 days or less) to long-term plans extending up to 72 months. The type of agreement available depends on the total amount owed and your financial situation.

Streamlined installment agreements for debts under $50,000 require minimal financial disclosure. Partial payment installment agreements for larger debts involve comprehensive financial analysis and monthly payments based on your ability to pay rather than the full debt amount.

| Agreement Type | Debt Threshold | Duration | Financial Disclosure |

|---|---|---|---|

| Short-term | Any amount | Up to 120 days | Minimal |

| Streamlined | Under $50,000 | Up to 72 months | Basic income/expense |

| Partial Payment | Over $50,000 | Up to 72 months | Comprehensive collection information |

| Non-streamlined | Over $50,000 | Varies | Full financial statement |

Professionals who understand Circular 230 regulations can negotiate more favorable terms and ensure compliance throughout the resolution process.

Penalty Abatement Strategies

Reducing or eliminating penalties significantly decreases total debt and makes resolution more achievable. The IRS grants penalty relief under specific circumstances that demonstrate reasonable cause rather than willful neglect.

First-Time Penalty Abatement

The First-Time Penalty Abatement (FTA) waiver provides administrative relief for taxpayers with clean compliance histories. If you've filed and paid timely for the previous three years, you may qualify for automatic penalty removal on failure-to-file and failure-to-pay penalties.

FTA applies to only one tax year and covers only certain penalties. It doesn't eliminate accuracy-related penalties or fraud penalties. However, removing failure-to-file penalties-the most severe-creates substantial savings.

Reasonable Cause Abatement

Beyond FTA, the IRS considers reasonable cause arguments for penalty removal. Qualifying circumstances include:

- Serious illness or death in the immediate family

- Natural disasters or civil unrest

- Inability to obtain necessary records despite reasonable efforts

- Erroneous written advice from the IRS itself

- Unavoidable absence from business operations

Documentation supporting reasonable cause claims strengthens requests. Medical records, death certificates, insurance claims from disasters, and dated correspondence all provide evidence supporting penalty relief.

Exploring resources from the Office of the Taxpayer Advocate can provide additional support when navigating complex penalty abatement situations.

Professional Assistance vs. Self-Filing

Determining whether to handle irs back tax filing independently or seek professional help depends on complexity, debt size, and your comfort with tax regulations. Each approach offers distinct advantages and limitations.

When to File Independently

Simple situations involving straightforward W-2 income, standard deductions, and minimal debt often allow successful self-filing. If you have complete documentation, owe modest amounts, and understand basic tax concepts, independent filing saves professional fees while ensuring compliance.

The IRS provides free resources including publications, online tools, and telephone assistance. Taxpayer Assistance Centers offer in-person help with basic questions. Federal tax research guidance helps navigate official publications and regulations.

When Professional Help Becomes Essential

Complex scenarios involving significant debt, business income, multiple unfiled years, or potential criminal exposure require professional expertise. Tax professionals certified to practice before the IRS understand negotiation strategies, resolution options, and procedural requirements that laypeople typically miss.

Enrolled agents, CPAs, and tax attorneys possess different expertise levels and costs. Enrolled agents specialize in IRS representation and typically charge less than attorneys. CPAs provide broader financial planning expertise. Tax attorneys handle criminal matters and complex legal issues.

Firms specializing in tax resolution understand the nuances that make the difference between successful and failed resolution attempts. Reading insights from CLAW Tax Group’s blog provides valuable perspective on common scenarios and strategic approaches.

Preventing Future Filing Problems

Once you've addressed past filing failures, implementing systems to maintain ongoing compliance prevents future irs back tax filing situations. Proactive measures save money, stress, and legal complications.

Creating a Filing System

Organize tax documents throughout the year rather than scrambling at deadline time. Designate a physical location or digital folder for tax-related paperwork. When documents arrive, file them immediately in categorized sections:

- Income statements (W-2s, 1099s, K-1s)

- Deduction receipts (medical, charitable, business expenses)

- Property records (mortgage statements, property tax bills)

- Retirement and investment statements

Set calendar reminders for quarterly estimated tax payments if you're self-employed. Missing estimated payments triggers penalties even when you file on time.

Addressing Financial Hardship Proactively

When financial difficulties threaten your ability to file or pay, communicate with the IRS immediately rather than avoiding the problem. Filing for extensions provides additional time to prepare returns accurately, even if you cannot pay immediately.

Filing a return without payment avoids the severe failure-to-file penalty while incurring only the smaller failure-to-pay penalty. This seemingly small distinction saves substantial money over time.

Consider adjusting withholding or estimated payments to better match your actual tax liability. Chronic underpayment creates annual crisis situations, while proper tax planning distributes the burden manageable throughout the year.

Statute of Limitations Considerations

Understanding collection statutes and refund limitations influences strategic timing decisions in irs back tax filing. These time limits create both opportunities and risks that impact resolution outcomes.

Collection Statute Expiration Date

The IRS generally has 10 years from assessment to collect outstanding tax debts. This Collection Statute Expiration Date (CSED) provides a definitive endpoint for collection activities, though certain actions suspend or extend the period.

Filing for bankruptcy, submitting Offers in Compromise, or leaving the country can extend collection periods beyond the standard 10 years. Understanding these nuances prevents inadvertent statute extension when taxpayers believe debts are approaching expiration.

Refund Statute Limitations

Unlike collection periods, refund statutes limit your ability to claim money the IRS owes you. Generally, you must file within three years of the original due date or two years from when you paid the tax, whichever is later, to claim refunds.

This creates urgency for filing back tax returns when refunds are due. Many taxpayers with modest incomes qualify for refundable credits like the Earned Income Tax Credit, potentially representing thousands of dollars in unclaimed refunds that expire if not pursued timely.

Older unfiled returns where refunds would have been due often make sense to skip filing if the refund statute has expired and no income reporting discrepancies exist. However, strategic decisions require analysis of your complete tax situation rather than isolated year-by-year evaluation.

State Tax Implications

Federal irs back tax filing often triggers corresponding state obligations. Most states with income taxes require residents to file when federal filing thresholds are met, creating dual compliance requirements.

State agencies frequently receive federal tax information through data-sharing agreements. When you file federal back tax returns, state authorities become aware of previously unreported income and may issue their own assessments.

Coordinating Federal and State Filings

File federal returns first, as state returns typically require federal adjusted gross income as a starting point. Most states use federal tax data to calculate state obligations, making federal returns the foundational document.

State penalty and interest structures differ from federal rules. Some states impose more aggressive penalties, while others offer more lenient resolution options. Each state maintains unique rules about:

- Installment agreement qualifications

- Offer in Compromise availability

- Penalty abatement procedures

- Collection enforcement methods

Research your specific state's requirements or consult professionals familiar with both federal and state tax resolution. Resolving federal obligations while ignoring state debts leaves significant exposure unaddressed.

Addressing unfiled tax returns requires prompt action, careful planning, and often professional guidance to navigate complex regulations and resolution options. Whether you're facing one missed year or multiple unfiled returns, understanding the irs back tax filing process empowers you to take control of your tax situation before penalties and collection actions escalate beyond manageability. CLAW Tax Group specializes in helping taxpayers resolve back tax situations through strategic planning, professional negotiation, and comprehensive resolution services designed to minimize debt and restore compliance efficiently.