Failing to pay taxes on time can trigger a cascade of financial consequences that extend far beyond the original amount owed. The IRS imposes strict penalties for unpaid taxes, and these charges accumulate rapidly through interest and additional fees. Whether you're an individual taxpayer who missed the April deadline or a business owner struggling with payroll tax obligations, understanding the penalty structure is essential for protecting your financial future. This comprehensive guide explores the various types of penalties, how they're calculated, and the strategies available to minimize or eliminate these costly charges.

Understanding the Basic Penalty Structure

The IRS employs multiple penalty mechanisms to encourage timely tax compliance. Each penalty serves a specific purpose and applies under different circumstances.

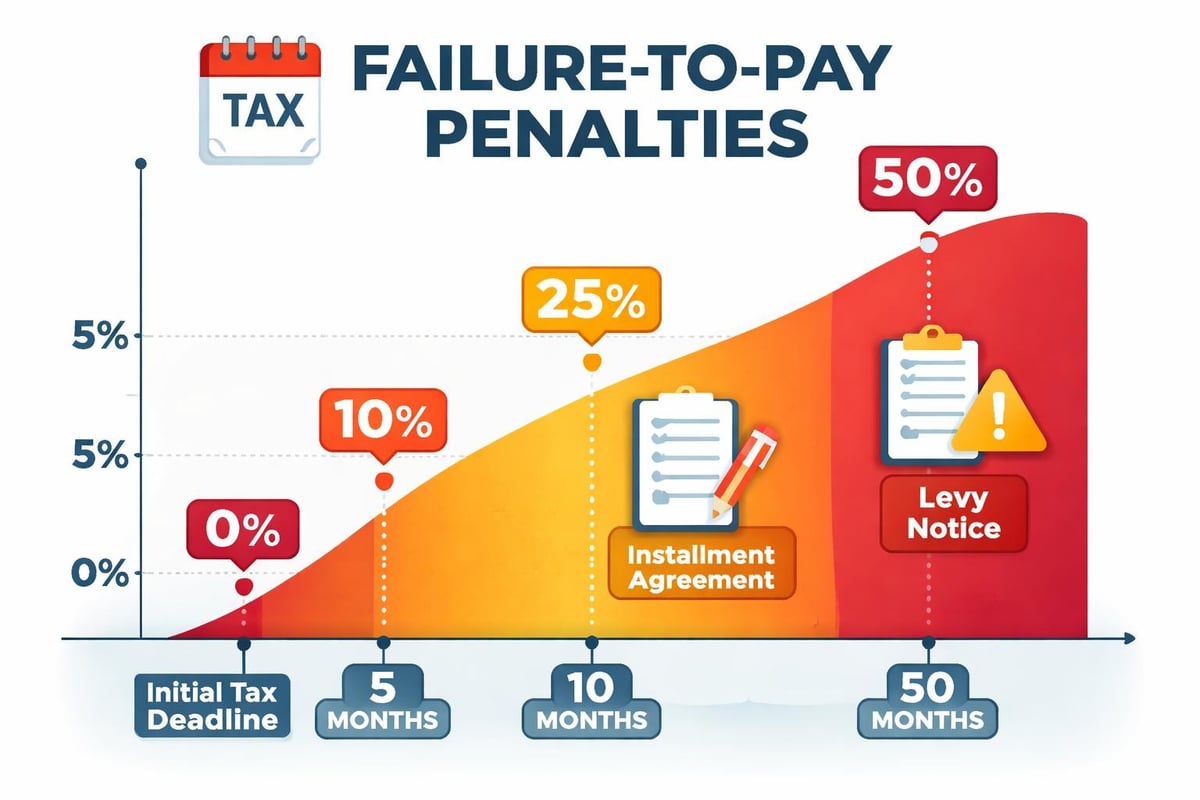

The most common penalty taxpayers encounter is the failure-to-pay penalty. This penalty begins accruing from the original due date of your tax return and continues until you pay the full amount owed. The failure-to-pay penalty currently stands at 0.5% of your unpaid taxes for each month or partial month the tax remains unpaid.

How Penalties Accumulate Over Time

Penalties don't exist in isolation. They work in combination with interest charges to create a compounding effect on your tax debt.

The failure-to-pay penalty can reach a maximum of 25% of your unpaid taxes. If you receive a notice of intent to levy and don't pay within ten days, the monthly penalty rate increases to 1%. However, if you establish an installment agreement before receiving this notice, the penalty rate reduces to 0.25% per month while the agreement remains in effect.

Interest charges apply separately from penalties and compound daily on both the unpaid tax and any penalties. The IRS adjusts the interest rate quarterly based on the federal short-term rate plus 3%. For the first quarter of 2026, individual taxpayers face an interest rate that reflects current economic conditions, making early resolution increasingly important.

Failure-to-File vs. Failure-to-Pay Penalties

Many taxpayers confuse these two distinct penalties, but understanding the difference is crucial for managing your tax obligations effectively.

The failure-to-file penalty applies when you don't submit your tax return by the deadline, including extensions. This penalty is significantly steeper than the failure-to-pay penalty, charging 5% of the unpaid taxes for each month or part of a month that your return is late, up to a maximum of 25%.

| Penalty Type | Monthly Rate | Maximum | Trigger Event |

|---|---|---|---|

| Failure-to-File | 5% | 25% | Missing filing deadline |

| Failure-to-Pay | 0.5% | 25% | Unpaid tax after deadline |

| Combined | 5% (4.5% + 0.5%) | 47.5% | Both violations |

When both penalties apply simultaneously, the failure-to-file penalty reduces to 4.5% per month, making the combined charge 5% monthly. After five months, the failure-to-file penalty reaches its maximum, but the failure-to-pay penalty continues accumulating.

The Minimum Penalty for Late Filing

If your return is more than 60 days late, you'll face a minimum penalty equal to the lesser of $485 (as of 2026) or 100% of the unpaid tax. This provision ensures that even small tax debts carry substantial penalties when filing is significantly delayed.

Understanding various penalties and interest charges helps you prioritize which actions to take first when facing tax difficulties.

Employment Tax Penalties for Businesses

Business owners face additional penalty exposure related to payroll taxes. These penalties can devastate a company's financial health if left unaddressed.

Trust Fund Recovery Penalty

When businesses fail to remit employee withholding taxes to the IRS, responsible parties may face the Trust Fund Recovery Penalty. This civil penalty equals 100% of the unpaid trust fund taxes and can be assessed personally against anyone responsible for collecting, accounting for, or paying over these taxes.

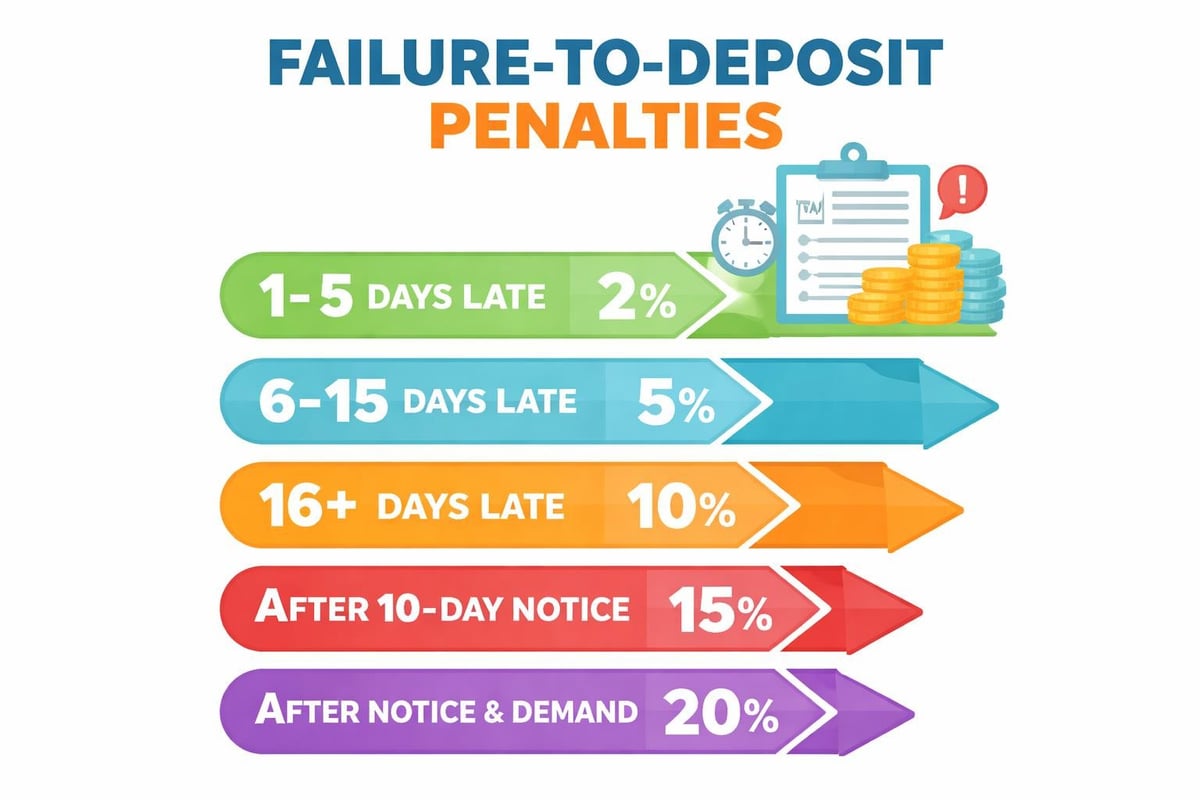

The failure-to-deposit penalty applies when businesses don't deposit employment taxes according to their required schedule. The penalty varies based on how late the deposit is:

- 2% for deposits made 1-5 days late

- 5% for deposits made 6-15 days late

- 10% for deposits made 16 or more days late

- 10% for amounts paid within 10 days of receiving the first IRS notice

- 15% for amounts still unpaid more than 10 days after receiving the IRS notice

These percentages apply to the deposit amount, not the total tax liability, making timely deposits essential for business financial planning.

State-Level Penalties and Variations

Federal penalties represent only part of the picture for many taxpayers. State tax authorities impose their own penalty structures that often mirror but sometimes exceed federal rates.

State Penalty Examples

Different states take varying approaches to penalties for unpaid taxes. California and Colorado provide useful examples of how state penalties operate alongside federal obligations.

California’s penalty structure includes a 5% penalty for late payment, plus an additional 0.5% per month or part of a month that the tax remains unpaid, up to 40 months. California also imposes a separate late filing penalty of 5% of the unpaid tax for each month the return is late, up to a maximum of 25%.

Colorado’s penalty and interest provisions similarly combine percentage-based penalties with interest charges. Colorado assesses a late payment penalty of 5% of the tax due, with additional monthly penalties that can significantly increase the total amount owed.

When you owe both federal and state taxes, penalties can accumulate on multiple fronts simultaneously. Professional tax resolution services help coordinate responses to multiple tax authorities, preventing one penalty from distracting you from others that may be accumulating.

Interest Calculations and Compounding Effects

Interest on unpaid taxes operates differently from penalties and deserves separate attention. Unlike penalties that have maximum caps, interest continues indefinitely until you pay the full tax debt.

The IRS compounds interest daily on both the unpaid tax and any accrued penalties. This compounding effect means that delaying payment becomes increasingly expensive over time. For tax years beginning in 2026, taxpayers should monitor quarterly interest rate adjustments to understand their total debt trajectory.

How Interest Interacts with Payment Plans

Even when you establish an installment agreement, interest continues accruing on the unpaid balance. However, the reduced penalty rate for payments made under an installment agreement helps minimize the overall growth of your tax debt.

Many taxpayers underestimate the long-term cost of interest when negotiating payment arrangements. A tax debt that starts at $10,000 can grow substantially over a 3-5 year payment period when interest compounds daily at rates exceeding 6-8% annually.

Penalty Abatement Opportunities

The IRS provides several mechanisms for reducing or eliminating penalties, though interest charges are rarely waived except in cases of IRS error.

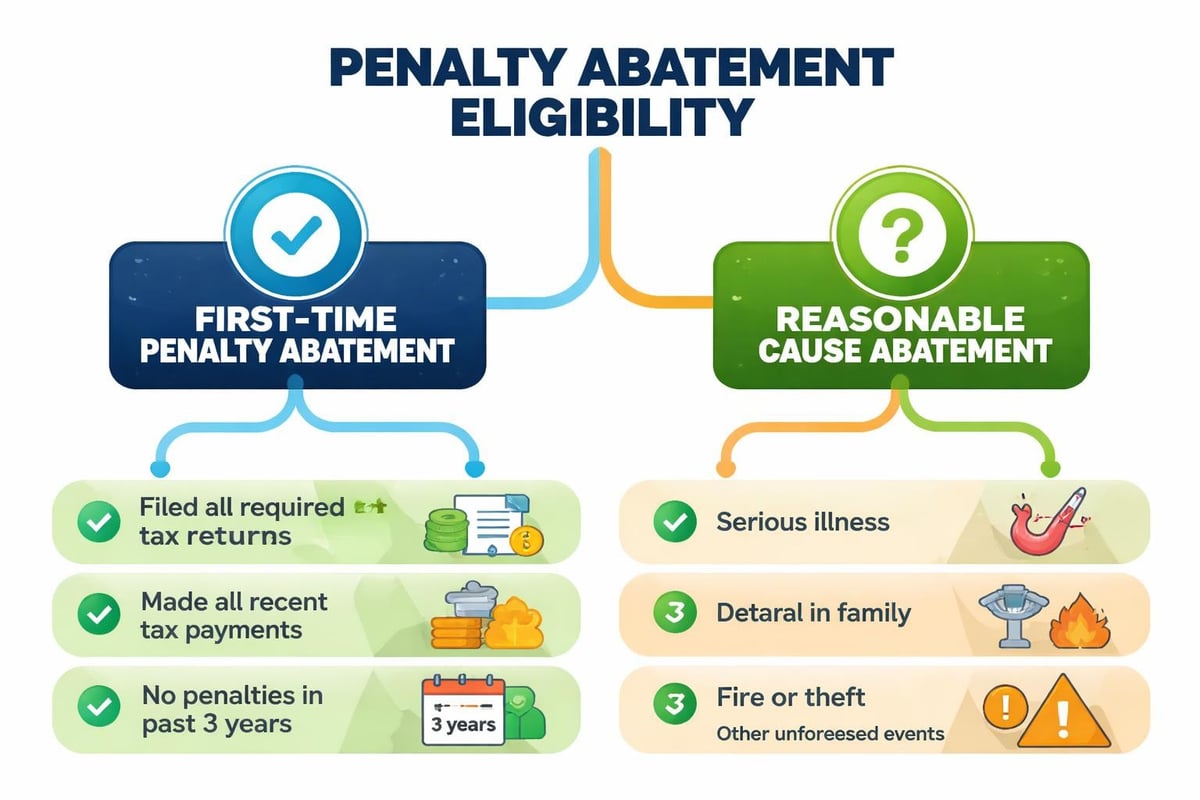

First-Time Penalty Abatement

Taxpayers with a clean compliance history may qualify for first-time penalty abatement. This administrative waiver can eliminate failure-to-file, failure-to-pay, and failure-to-deposit penalties if you meet specific criteria:

- No penalties in the prior three tax years

- All required returns have been filed or filed on extension

- You've paid or arranged to pay any tax due

First-time abatement applies only to penalties for a single tax year and doesn't extend to future years without maintaining compliance.

Reasonable Cause Abatement

When circumstances beyond your control prevented timely payment or filing, you may qualify for reasonable cause abatement. Acceptable reasons include:

- Natural disasters or other catastrophic events

- Serious illness or death in the immediate family

- Unavoidable absence

- Fire, casualty, or other disturbance

- Inability to obtain records necessary for filing

The IRS evaluates reasonable cause requests on a case-by-case basis. Documentation supporting your claim strengthens your abatement request significantly.

Criminal Consequences of Tax Evasion

While civil penalties represent the most common consequence of unpaid taxes, severe cases can escalate to criminal charges. Understanding the distinction between civil non-compliance and criminal tax evasion is essential.

Criminal tax prosecution typically requires proof of willful intent to evade taxes. Simply owing taxes, even substantial amounts, doesn't constitute a crime. However, certain actions cross the line into criminal territory:

- Filing false returns with intent to underreport income

- Maintaining double sets of books

- Making false statements to IRS agents

- Concealing assets or income through sophisticated schemes

Tax-related criminal charges carry serious penalties including imprisonment, making early intervention critical when tax debts become overwhelming. Most taxpayers facing criminal investigation benefit from immediate legal representation specializing in tax defense.

The IRS Criminal Investigation Division handles fewer than 3,000 cases annually, focusing on egregious violations rather than typical unpaid tax situations. However, when businesses fail to remit employee withholding taxes repeatedly, criminal prosecution becomes more likely.

Payment Options to Avoid or Reduce Penalties

Taking proactive steps to address tax debts minimizes penalty exposure and demonstrates good faith to the IRS.

Installment Agreements

The IRS offers various installment agreement options depending on the amount owed and your financial situation. Guaranteed installment agreements are available for taxpayers owing $10,000 or less, while streamlined agreements accommodate debts up to $50,000.

When you establish an installment agreement, the failure-to-pay penalty rate reduces from 0.5% to 0.25% monthly. Interest continues accruing, but the reduced penalty rate significantly decreases the total cost of resolving your tax debt over time.

Offers in Compromise

An Offer in Compromise allows qualifying taxpayers to settle their tax debt for less than the full amount owed. The IRS considers your ability to pay, income, expenses, and asset equity when evaluating offers.

While an offer is under consideration, the IRS suspends most collection activities. Successfully negotiating an offer eliminates both the remaining tax debt and associated penalties, though interest typically remains included in the negotiated amount.

| Resolution Option | Penalty Relief | Best For | Approval Difficulty |

|---|---|---|---|

| Installment Agreement | Reduced rate (0.25%) | Manageable debts | Low |

| Offer in Compromise | Complete elimination | Financial hardship | High |

| Currently Not Collectible | Temporary suspension | Severe hardship | Medium |

| Penalty Abatement | Targeted elimination | Clean history | Low-Medium |

Professional representation significantly improves success rates for complex resolution strategies. Tax relief services navigate IRS procedures while protecting your rights throughout the process.

The Cost of Inaction

Ignoring tax debts creates a downward spiral of accumulating penalties and interest. What happens when you don’t pay taxes on time extends beyond financial penalties to include aggressive collection actions.

IRS Collection Powers

When penalties for unpaid taxes remain unaddressed, the IRS escalates enforcement through increasingly severe collection mechanisms. The progression typically follows this pattern:

- Notices and demands for payment – Initial contact establishing the debt

- Federal tax liens – Public records that damage credit and attach to property

- Levies on bank accounts – Direct seizure of funds from financial institutions

- Wage garnishment – Continuous withdrawal from paychecks until debt resolves

- Property seizure – Physical taking of assets for auction to satisfy debts

Each collection action carries additional fees and administrative costs that increase your total debt. A federal tax lien filing fee adds $10,000 minimum to your balance in many cases when the IRS files this public notice.

Impact on Financial Health

Beyond the direct costs of penalties and collection actions, unpaid tax debts create cascading financial problems. Federal tax liens appear on credit reports, damaging your credit score and making it difficult to secure loans, mortgages, or even employment in certain industries.

Wage levies take a substantial portion of your paycheck, leaving minimal amounts for living expenses. Unlike typical garnishments limited to 25% of disposable income, IRS levies can claim much larger percentages based on filing status and dependents.

Strategic Timing for Tax Debt Resolution

When you address tax debts matters almost as much as how you address them. Strategic timing can reduce penalties significantly.

Filing your return on time, even when you can't pay the full amount, eliminates the failure-to-file penalty. This single action can save you 4.5% per month compared to delaying both filing and payment.

Requesting an installment agreement before the IRS sends a notice of intent to levy prevents the penalty increase from 0.5% to 1% monthly. This timing consideration saves substantial amounts on larger tax debts.

If you're exploring how to pay the IRS if you owe taxes, understanding these timing factors helps prioritize your actions. Filing, establishing payment arrangements, and requesting penalty abatement should occur in strategic sequence to maximize savings.

Documentation and Record Keeping

Maintaining thorough documentation serves multiple purposes when dealing with penalties for unpaid taxes. Accurate records support penalty abatement requests, substantiate reasonable cause claims, and protect your interests during IRS examinations.

Essential documents to preserve include:

- All correspondence from the IRS and state tax authorities

- Proof of payment for all tax installments

- Medical records supporting illness or disability claims

- Death certificates and estate documents for family circumstances

- Natural disaster declarations and insurance claims

- Bank statements showing financial hardship

- Employment records documenting income changes

When requesting penalty abatement, the burden of proof rests with you. Comprehensive documentation transforms subjective claims into credible evidence that tax authorities must consider seriously.

Working with Tax Professionals

Complex tax situations involving substantial penalties typically benefit from professional representation. Tax attorneys bring specialized knowledge of IRS procedures, penalty abatement strategies, and negotiation techniques that improve outcomes.

Professional representation provides several advantages:

- Technical expertise in penalty calculation and applicable relief provisions

- Negotiation skills developed through repeated IRS interactions

- Protection from self-incrimination during IRS interviews and examinations

- Strategic planning to address current debts while preventing future problems

- Time savings by handling complex paperwork and IRS communications

Tax professionals also identify opportunities that non-specialists commonly overlook. Penalty abatement strategies, installment agreement structures, and offer in compromise qualifications require nuanced understanding of IRS policies and procedures.

Multi-Year Tax Debt Complications

Taxpayers with multiple years of unpaid taxes face compounded penalty exposure. Each tax year generates separate penalties that accumulate independently, creating overwhelming total debt loads.

The IRS applies payments according to specific rules that may not align with your best interests. Generally, payments apply first to the oldest tax year, reducing penalties on old debts while newer years continue accumulating penalties at full rates.

Strategic payment allocation can sometimes be negotiated as part of comprehensive resolution plans. However, these arrangements require sophisticated understanding of IRS collection procedures and designation protocols.

When dealing with multi-year debts, the statute of limitations on collection becomes relevant. The IRS generally has 10 years from the assessment date to collect tax debts. Certain actions pause or extend this period, making professional guidance valuable for understanding when debts may expire.

Preventing Future Penalty Exposure

Once you've addressed existing penalties for unpaid taxes, preventing recurrence becomes essential. Several strategies help maintain compliance and avoid future penalty accumulation.

Adjusting Withholding and Estimated Payments

Many tax debts result from insufficient withholding or estimated tax payments throughout the year. Reviewing your withholding after major life changes prevents year-end surprises.

Self-employed individuals and those with investment income should calculate quarterly estimated tax payments carefully. The IRS provides safe harbor rules that, when followed, eliminate underpayment penalties even if your final tax liability exceeds estimates.

Building Tax Savings Reserves

Setting aside funds throughout the year for tax obligations creates a buffer against future penalties. Business owners should maintain separate accounts for payroll tax obligations, treating these funds as untouchable until remitted to tax authorities.

Individual taxpayers benefit from similar discipline, automatically transferring percentage amounts from each paycheck into dedicated tax savings accounts.

Regular Tax Planning Reviews

Annual tax planning sessions identify changing circumstances that affect tax liability. Proactive planning allows for withholding adjustments, estimated payment modifications, and strategic decisions that minimize both tax liability and penalty exposure.

Working with tax professionals on a preventive basis costs significantly less than resolving penalty-laden tax debts after they've accumulated for months or years.

Understanding penalties for unpaid taxes empowers you to make informed decisions about addressing tax obligations before they spiral out of control. Early intervention, strategic payment arrangements, and professional representation can significantly reduce or eliminate these costly charges. If you're facing tax debt and accumulating penalties, CLAW Tax Group provides comprehensive tax resolution services including penalty abatement, installment agreements, and offers in compromise to help you resolve your tax obligations while protecting your financial future. Don't let penalties continue mounting when solutions exist to reduce your burden and restore your peace of mind.