Facing a sudden freeze on your bank account can feel overwhelming. The stress and confusion may leave you unsure of where to turn next.

This guide is designed to demystify the bank levy process in 2026. You will learn what triggers a bank levy, how it works, and—most importantly—how to protect your rights and finances if it happens to you.

We will break down each step, from understanding your legal rights to responding quickly and preventing future levies. As bank levies are becoming a more common tool in debt collection, knowing your options is essential to safeguard your assets.

Ready to take control? Follow this comprehensive guide to confidently manage or avoid a bank levy.

What Is a Bank Levy?

Facing a bank levy can be intimidating, especially if you are unsure how the process works or what your rights are. Understanding the basics is the first step to protecting your finances and responding effectively.

Definition and Purpose

A bank levy is a legal process that allows a creditor to seize money directly from your bank account to satisfy an unpaid debt. Unlike wage garnishment, which takes funds from your paycheck, a bank levy targets the money you have already deposited in your account.

Several types of debt can lead to a bank levy. The most common triggers include unpaid taxes, court judgments, and defaulted loans. In the case of unpaid taxes, government agencies like the IRS can initiate a bank levy without a court judgment. If you are dealing with an IRS levy, the process can be different and may require specific strategies, as detailed in this IRS levy on bank accounts guide.

Who is involved in a bank levy?

- The creditor (the party owed money)

- The debtor (the account holder)

- The bank (where your funds are held)

- The court or enforcement agency (authorizes and oversees the process)

Here’s a quick comparison:

| Feature | Bank Levy | Garnishment |

|---|---|---|

| Source of funds | Bank account | Paycheck |

| Requires judgment? | Usually (except IRS/government) | Yes |

| Affected funds | Existing account balance | Future wages |

| Common debts | Taxes, judgments, loans | Child support, consumer debt |

For example, if you owe the IRS back taxes, the agency may issue a bank levy directly to your bank. In contrast, a private creditor must typically win a lawsuit and obtain a judgment before pursuing a bank levy.

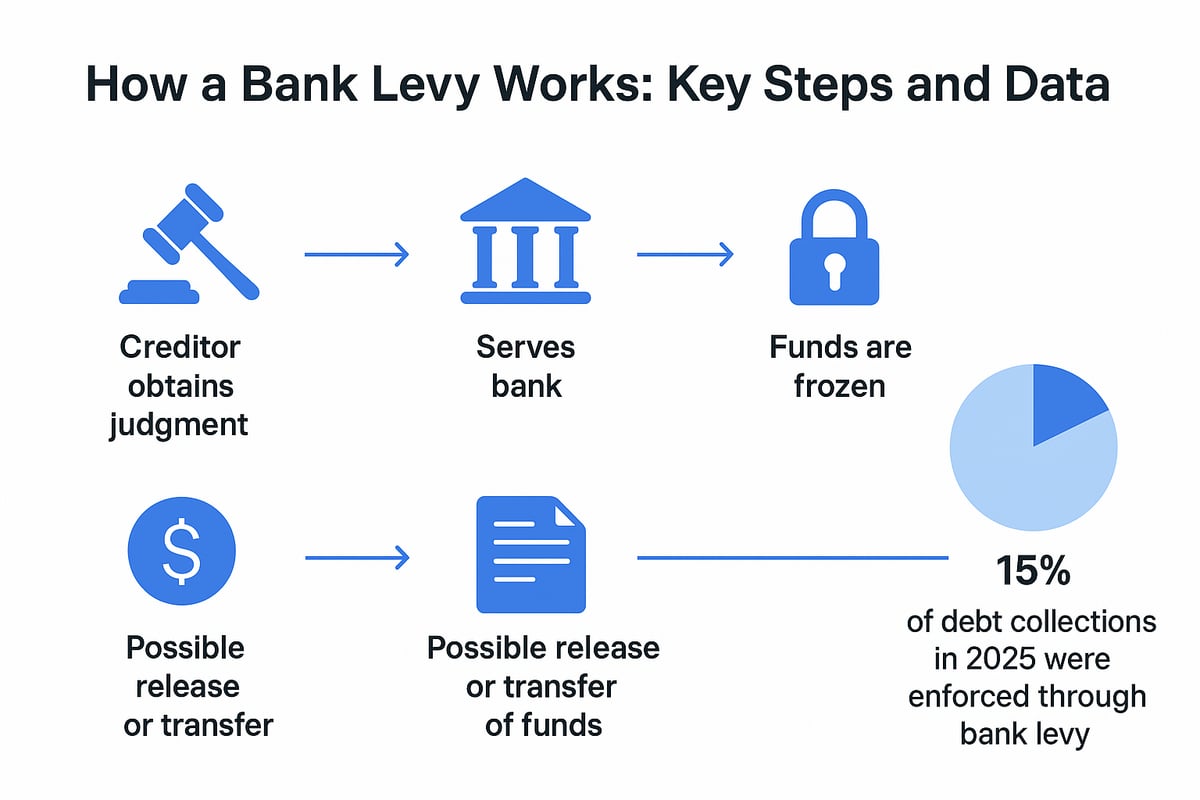

A bank levy is considered a last resort. Creditors usually attempt other collection methods before seeking court intervention. According to national data, over 15% of all enforced debt collections in 2025 involved a bank levy.

Joint and business accounts are not immune. If an account is jointly owned, all funds may be subject to a bank levy, though non-debtor owners can sometimes claim exemptions. Business accounts can also be levied if the business owes a debt.

How a Bank Levy Works

The bank levy process follows a strict sequence of steps. First, a creditor typically obtains a court judgment confirming the debt. Once the judgment is in place, the creditor requests a writ of execution from the court. This document authorizes the bank levy.

Next, the creditor serves the bank with the writ and levy instructions. At this point, the bank is legally required to freeze the funds in your account, up to the amount owed. You will then receive a formal notice, usually within a few days, alerting you to the bank levy and giving you a chance to respond.

An example timeline might look like this:

- Creditor wins judgment in court.

- Writ of execution issued.

- Bank is served and freezes account funds.

- Account holder notified and given opportunity to claim exemptions.

- If no exemption is granted, funds are released to the creditor.

A bank levy can be a one-time event or, in some cases, recurring until the debt is paid. The bank must act quickly upon receiving the levy notice, freezing only the funds available at the moment of service. Any deposits made after that point are generally not affected by the current levy.

State laws can influence specific procedures. For example, in California, banks with multiple branches are served through a central location, and unique rules may apply for joint or business accounts.

It is important to remember that only the funds present in your account at the time the bank receives the levy notice are subject to seizure. Later deposits are protected unless a new bank levy is issued.

Legal Rights and Protections During a Bank Levy

Facing a bank levy can be daunting, but understanding your rights is essential to protecting your assets and responding effectively. Federal and state laws ensure specific protections for account holders during the bank levy process. Let’s break down your legal safeguards step by step.

Notification and Due Process

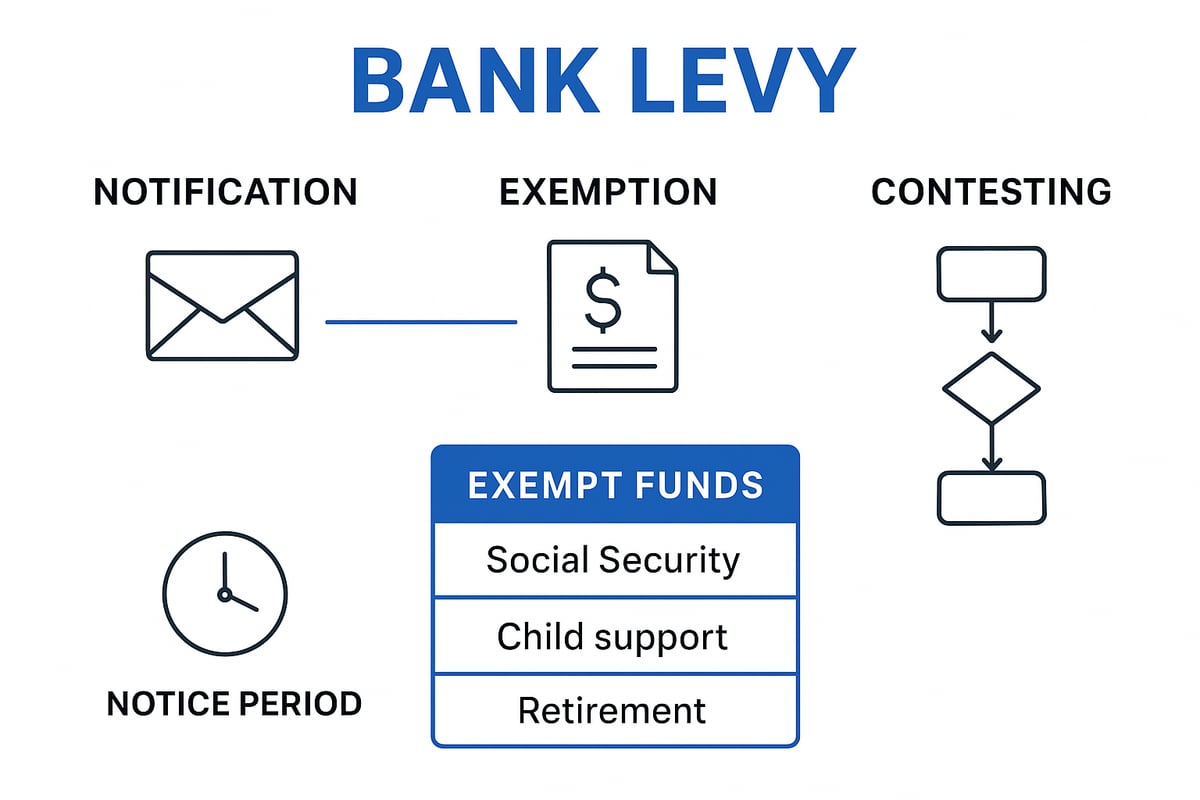

When a bank levy is initiated, the law requires that you receive prompt written notice. Typically, the bank or the enforcement agency must provide copies of the writ of execution and the notice of levy. For example, in California, you are entitled to a 10-day notice period after the bank receives the levy order. This window allows you to review your options and protect your assets.

Due process is a fundamental right during the bank levy process. The bank must freeze only the funds available at the time of service and notify you immediately. Under both federal and state law, failure to provide proper notice can invalidate a bank levy, giving you grounds to challenge the action.

You should always verify that you have received all required documentation. If you suspect your notice was delayed or missing, contact your bank and the court for clarification. Knowing these procedures ensures you are not caught off guard if a bank levy affects your account.

Exemptions and Protected Funds

Not all funds in your account are subject to a bank levy. Federal and state laws protect certain types of funds, such as Social Security benefits, child support, and specific retirement payments. For instance, federal law shields up to two months’ worth of Social Security benefits from a bank levy, regardless of your account balance.

Here is a quick reference table of commonly exempt funds:

| Exempt Fund Type | Federal Protection | State Variations |

|---|---|---|

| Social Security | Yes (2 months) | May offer more |

| Child Support | Yes | Varies by state |

| Retirement Benefits | Limited | Some states expand |

| Disability Benefits | Yes | Varies by state |

To claim your exemption, you must act quickly. Complete the required forms and provide supporting documents, such as benefit statements or proof of source. In 2025, courts upheld 30% of challenges related to exempt funds, demonstrating the importance of acting promptly. Special rules may apply to joint or spousal accounts, so review your account structure carefully.

For step-by-step guidance, visit this Claim of Exemption – Bank Levy resource, which explains forms and procedures in detail.

Contesting a Bank Levy

If you believe your bank levy is improper or targets exempt funds, you have the right to contest it. File a claim of exemption or a motion to quash the levy within the typical 10 to 15-day deadline. The process often involves submitting forms, providing documentation, and requesting a court hearing.

Here are the key steps:

- Review the notice and identify deadlines.

- File the appropriate forms with the court.

- Gather supporting evidence, such as proof of exempt income.

- Attend the hearing and present your case.

For example, you may file a Notice of Opposition to Claim of Exemption if you disagree with the creditor’s position. Timely action is critical, as missing deadlines may result in the permanent loss of funds. Understanding these procedures gives you the best chance to protect your finances during a bank levy.

Step-by-Step Guide: The Bank Levy Process in 2026

A bank levy can feel complex, but understanding each step helps you respond effectively. In 2026, the bank levy process generally follows a strict legal pathway. Knowing what to expect at every stage gives you the power to protect your assets and act quickly if your account is targeted.

1. Creditor Obtains a Judgment

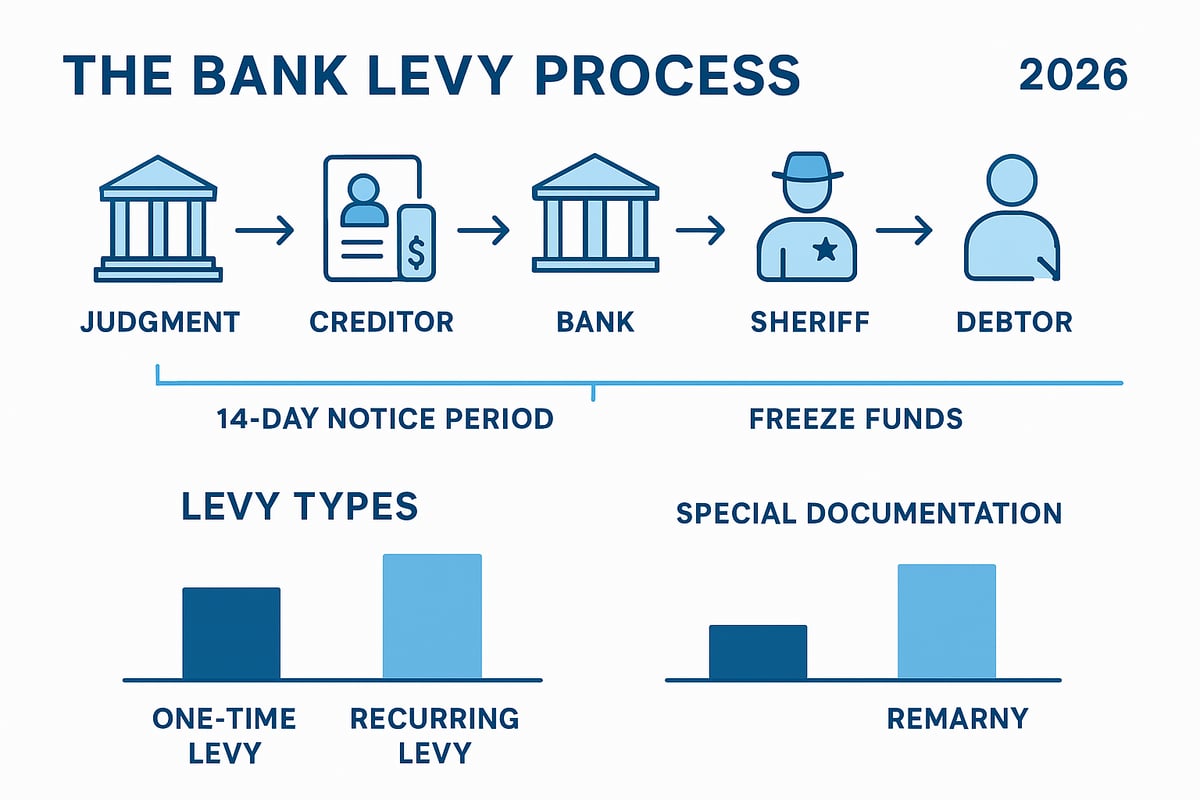

The bank levy process typically begins when a creditor wins a court judgment against you. This judgment is a formal declaration that you owe the debt. For example, if you default on a credit card, the lender might sue, and if the court rules in their favor, they can move forward with a bank levy.

Some exceptions exist. Government agencies like the IRS can initiate a bank levy for unpaid taxes without a court judgment. In these cases, exploring IRS payment plan options can help you avoid a levy altogether.

Data from 2025 shows that over 60% of consumer bank levies follow a civil judgment. This step is crucial, as it sets the stage for all further actions.

2. Writ of Execution and Levy Instructions

After obtaining a judgment, the creditor requests a writ of execution from the court. This legal document authorizes the seizure of your funds. Supporting paperwork, such as a file-endorsed judgment or a memorandum of costs, is usually required.

In California, for instance, creditors use the EJ-130 form to request a writ. The writ may also include post-judgment costs and interest, increasing the total owed. At this point, the groundwork for the bank levy is fully in place.

3. Serving the Bank and Freezing Funds

Once the writ is issued, the creditor arranges for service on your bank. The sheriff or a process server delivers the levy instructions directly to the bank. The timing is critical, as only the funds in your account at the moment of service are frozen for the bank levy.

Some creditors may strategically serve the bank on payday to maximize the funds available. After receiving the notice, the bank must immediately freeze the specified amount and notify you of the action. Larger banks may require service at a central location, depending on state law.

4. Notice to Debtor and Opportunity to Respond

After the bank freezes the funds, you will receive a written notice. This notice outlines your rights and provides copies of the writ of execution and the levy itself. Typically, you have 10 days to contest the bank levy or claim exemptions, though this period varies by state.

Receiving the notice promptly is essential. Delays may limit your options to protect your money. The notice will also include forms and instructions for how to file a claim of exemption or request a hearing.

5. Release or Transfer of Funds

If you do not contest the bank levy or your challenge is unsuccessful, the frozen funds are released to the creditor. The timeline for this transfer depends on local rules, often ranging from 15 to 30 days after the initial notice.

If your account balance is less than the judgment amount, only available funds are taken. Partial bank levies may occur, and the creditor could initiate another levy if the debt remains unpaid.

6. Special Situations and Documentation

Bank levies involving joint, spousal, or business accounts require extra steps. For example, in California, a spousal affidavit may be necessary to clarify ownership of funds. Business accounts with fictitious names need a certified business name statement.

Each situation adds documentation but also provides opportunities to assert rights. Reviewing account types and preparing supporting evidence can help protect non-debtor funds during a bank levy.

Your Options If Your Bank Account Is Levied

Discovering a bank levy on your account can feel overwhelming, but you have options to protect your finances and exercise your rights. Taking prompt, informed action is crucial to limiting the impact of a bank levy and potentially recovering your funds.

Responding Quickly and Effectively

When a bank levy is placed on your account, immediate action is key. Contact your bank as soon as you receive notice. Ask for details about the levy, including a copy of the writ and notice. This will help you understand which creditor initiated the bank levy and the exact amount frozen.

Quick response can make a significant difference. Delays may result in permanent loss of funds if you miss important deadlines. Make sure to keep records of all communication with your bank and the creditor. Being proactive gives you the best chance to protect your money and resolve the bank levy efficiently.

Filing a Claim of Exemption

Certain funds in your account may be protected from a bank levy by law. To claim these exemptions, follow these steps:

- Obtain the claim of exemption forms from your bank or local court.

- Gather supporting documents, such as proof of Social Security benefits or child support deposits.

- File the forms within the deadline, typically 10 to 15 days from receiving notice.

- Attend any scheduled court hearings to present your case.

For example, claiming Social Security funds as exempt can prevent their seizure. Courts often uphold valid exemption claims, and in 2025, about 25% of such claims succeeded. Acting within the required timeframe is essential to protect your assets from the bank levy.

Negotiating With Creditors

Negotiation is another effective strategy if you face a bank levy. Contact your creditor directly to discuss possible arrangements. Many creditors are open to alternatives, such as:

- Setting up an installment plan

- Offering a lump-sum payment for a reduced amount

- Negotiating new payment terms

Sometimes, creditors will agree to release the bank levy if you show willingness to resolve the debt. Keep all agreements in writing and confirm terms before making payments. Open communication can prevent further legal action and help you regain financial stability.

Seeking Legal or Professional Help

Legal or financial professionals can provide essential guidance when dealing with a bank levy, especially in complex situations. If you have multiple creditors or disputed debts, consulting an attorney or tax resolution specialist is wise. Professional representation can increase your chances of a successful exemption or negotiation.

Services like those described in Tax resolution services explained can assist with filing claims, negotiating with creditors, and defending your rights. Many regions also offer free or low-cost legal aid for those who qualify. Expert advice ensures you make informed decisions and protects your interests during the bank levy process.

Preventing Future Levies

Addressing the root causes of a bank levy is vital to avoid repeated issues. Consider these proactive steps:

- Set up automatic payments to stay current on debts

- Consolidate outstanding balances if possible

- Communicate with creditors at the first sign of financial trouble

Proactive measures can help you avoid legal action and additional levies. Remember, a bank levy can also affect your credit score, so maintaining open communication and managing debts responsibly is crucial for long-term financial health.

Common Questions and Misconceptions About Bank Levies

Facing a bank levy can raise many questions and concerns. Understanding the facts helps you respond with confidence and protect your rights. Let’s address the most common questions and clear up some widespread misconceptions about the bank levy process.

Are All Debts Subject to Bank Levy?

Not every debt can lead to a bank levy. Typically, a bank levy is triggered by certain types of debts after other collection methods fail. These include:

- Tax debts (federal and state)

- Court judgments from lawsuits

- Unpaid child support or alimony

- Defaulted student loans

| Debt Type | Can Trigger Bank Levy? | Special Rules |

|---|---|---|

| IRS/State Tax Debt | Yes | Often no court needed |

| Private Loans | Yes | Court judgment required |

| Child Support | Yes | State-specific process |

| Credit Card Debt | Yes | Court judgment required |

Some debts, like medical bills or utility payments, only result in a bank levy after a lawsuit and court judgment. Understanding which debts can lead to a bank levy helps you prioritize which accounts need the most attention.

Can a Bank Levy Happen Without Notice?

A common misconception is that a bank levy always comes as a total surprise. In reality, laws require written notice before funds are seized in most cases. For example, IRS levies may happen quickly, but you will usually receive a final notice and an opportunity to respond. Private creditors must provide a notice of levy and copies of related court documents.

In some states, like New York, new laws are enhancing notice and exemption protections. For instance, the Notice to Financial Institutions: Wage Exemption Amount for Restraining Notices and Levies to Increase in New York State on January 1, 2026 describes upcoming changes to wage exemption amounts, which could affect the timing and scope of a bank levy.

What Happens to Joint or Business Accounts?

A bank levy can also impact joint and business accounts. If your name appears on a joint account, the entire balance may be frozen, even if some of the funds belong to a non-debtor. In these cases, the non-debtor can file a claim of exemption to recover their share.

For business accounts, a bank levy targets the entity named in the judgment. However, if personal and business funds are mixed, it can complicate the release of exempt funds. Always keep documentation ready to prove ownership and protect eligible funds from a bank levy.

How Long Does a Bank Levy Last?

The duration of a bank levy depends on the type of levy and the jurisdiction. Most bank levies are one-time events, freezing only the funds available at the time the levy is served. Later deposits are usually not affected unless a new levy is issued.

Typically, the bank holds the funds for 10 to 30 days, giving you time to contest the levy or claim exemptions. If you do not act, the money is released to the creditor. Staying informed about the timeline allows you to respond effectively when a bank levy occurs.

Will a Bank Levy Affect My Credit?

A bank levy itself does not appear as a separate item on your credit report. However, the underlying court judgment or debt that led to the bank levy often does. This judgment can lower your credit score and make future lending more difficult.

If you resolve the debt quickly, you may limit the long-term impact. However, repeated bank levy actions signal ongoing financial distress and can further damage your credit profile. Taking prompt action to address any bank levy can help protect your financial reputation moving forward.

State and Federal Laws Governing Bank Levies in 2026

Understanding the legal landscape for a bank levy is essential to protecting your assets and rights. Both federal and state laws set the rules for how a bank levy is applied, what funds are protected, and how you can respond. Let’s break down how these laws interact and what recent changes mean for you.

Federal Law Overview

Federal law provides a foundation for how a bank levy can be imposed. The Fair Debt Collection Practices Act (FDCPA) governs how creditors may pursue debts, while the Social Security Act protects certain federal benefits from a bank levy. For instance, federal law ensures that up to two months of Social Security benefits are shielded from levy, providing a crucial safety net for vulnerable populations.

When a bank levy is initiated, banks are required to review accounts for protected federal benefits and automatically exempt them from seizure. However, federal law sets only the minimum standards. States can, and often do, offer additional protections beyond what federal law requires.

Here’s a quick comparison:

| Law Level | Example Protections | Minimum Exemptions |

|---|---|---|

| Federal | Social Security, Veterans’ Benefits | 2 months of Social Security |

| State | Homestead, wages, higher account limits | Up to $2,500 in some states |

This dual system means understanding both federal and state rules is vital when facing a bank levy.

State-Specific Variations

Every state has its own rules regarding a bank levy, which can significantly impact your experience. States may set higher exemption amounts, require longer notice periods, or mandate specific procedures for creditors and banks. For example, California requires large banks to use a central location service for levy notices, which streamlines the process and protects account holders from missed notifications.

Common exempt assets by state include:

- Personal property up to a set value

- Retirement accounts

- Public benefits

- A portion of wages

In some states, up to $2,500 in a personal account is protected from a bank levy, giving debtors a financial buffer. Always check your own state’s exemptions, as they may be more generous than the federal baseline.

Recent Legal Updates and Trends

The legal environment for a bank levy is evolving. Between 2025 and 2026, several states have raised exemption thresholds, expanded protected funds, and updated notice requirements to enhance consumer protection. These changes reflect a response to rising debt and financial pressures nationwide.

For context, the delinquency rate on all loans in the U.S. 2025 rose, increasing the likelihood of bank levy actions as creditors seek repayment. Legislatures are responding by prioritizing fairness and transparency in the levy process.

Stay informed about new laws in your state, as trends point toward greater consumer rights and protections in the bank levy process.

Resources for Legal Assistance

If you are facing a bank levy, knowing where to get help can make a big difference. Many states offer free or low-cost legal aid through legal services organizations, consumer protection agencies, and court self-help centers. For example, the Sacramento Law Library provides guides and forms to help consumers navigate the bank levy process.

Sample resources:

- Legal aid societies and pro bono attorneys

- State court websites with forms and instructions

- Consumer protection agencies

- Tax relief professionals, like those featured in this tax relief services overview, can also help with complex bank levy issues

Data shows that over 40% of consumers seek legal advice after receiving a bank levy notice. Taking advantage of these resources improves your chances of protecting your assets and asserting your rights.

Preventing and Managing Bank Levies: Proactive Strategies

Facing a bank levy is never easy, but proactive strategies can help you minimize risk and protect your financial future. By understanding your vulnerabilities, communicating effectively, and taking steps to shield your assets, you can reduce the chances of a bank levy disrupting your life.

Understanding Your Financial Vulnerabilities

The first step in preventing a bank levy is knowing your own risk factors. Review your credit reports and court records regularly to spot any judgments or tax debts that could lead to a bank levy. If you have outstanding obligations, address them promptly.

Keep an eye out for warning signs such as collection notices or letters from creditors. Early action can prevent issues from escalating into a bank levy. Being aware of your financial situation helps you respond before creditors seek legal action.

You should assess your accounts for potential exposure. Joint or business accounts may also be at risk if you have unresolved debts.

Communicating With Creditors

Open, proactive communication with your creditors is vital in avoiding a bank levy. Many creditors prefer voluntary payment arrangements over legal proceedings. If you anticipate trouble meeting your obligations, contact creditors early to discuss options.

Consider negotiating a payment plan, hardship arrangement, or lump-sum settlement. Clear documentation of your efforts can support your case if legal action arises.

Banks are increasingly focused on debt recovery, especially in times of strong financial performance. For instance, FDIC-Insured Institutions Reported Return on Assets of 1.27 Percent and Net Income of $79.3 Billion in Third Quarter 2025, which may influence their willingness to pursue a bank levy. Early negotiation can reduce the likelihood of aggressive collection tactics.

Budgeting and Asset Protection

Effective budgeting is essential for managing your finances and reducing the risk of a bank levy. Keep exempt funds, such as Social Security or child support payments, in dedicated accounts whenever possible. This separation makes it easier to demonstrate exempt status if a levy occurs.

Maintain thorough records of all deposits and account activity. Proper documentation can help you prove that certain funds are protected by law. Consider using direct deposit for exempt payments to avoid any confusion during a bank levy.

If you anticipate a bank levy, consult with your bank about ways to safeguard your assets. Some institutions offer tools or alerts to help monitor account activity and potential legal actions.

Working With Tax Resolution and Legal Professionals

For complex situations or when facing an imminent bank levy, professional help is invaluable. Tax resolution specialists and attorneys can negotiate with creditors, file claims of exemption, and represent you in court if needed.

If you have multiple creditors or disputed debts, legal guidance can improve your chances of a favorable outcome. Professionals understand the nuances of bank levy laws and can help you navigate exemption rules.

Timely intervention by an expert may not only stop a bank levy but also prevent future occurrences. Seeking advice early helps you build a strategy tailored to your unique circumstances and ensures your rights are fully protected.

If you’re feeling uncertain about how a bank levy could impact your finances or what steps to take next, you’re not alone. Understanding your rights and options is the first step toward protecting your assets and regaining control. At CLAW Tax Group, we help individuals and businesses navigate complex tax and legal challenges every day—from negotiating with creditors to defending against IRS action. If you want clear guidance, practical solutions, or simply peace of mind, I encourage you to Contact us for a free consultation.

You don’t have to face this alone—let’s find the best path forward together.