Tax debt can create overwhelming financial pressure that affects every aspect of your life, from your ability to secure loans to the risk of wage garnishment and asset seizure. When you owe money to the IRS or state tax authorities, the stress can feel insurmountable. Fortunately, multiple programs and strategies exist to provide help paying tax obligations when you cannot afford to pay the full amount immediately. Understanding these options and knowing when to seek professional assistance can make the difference between years of financial struggle and a manageable path forward.

Understanding Your Tax Debt Situation

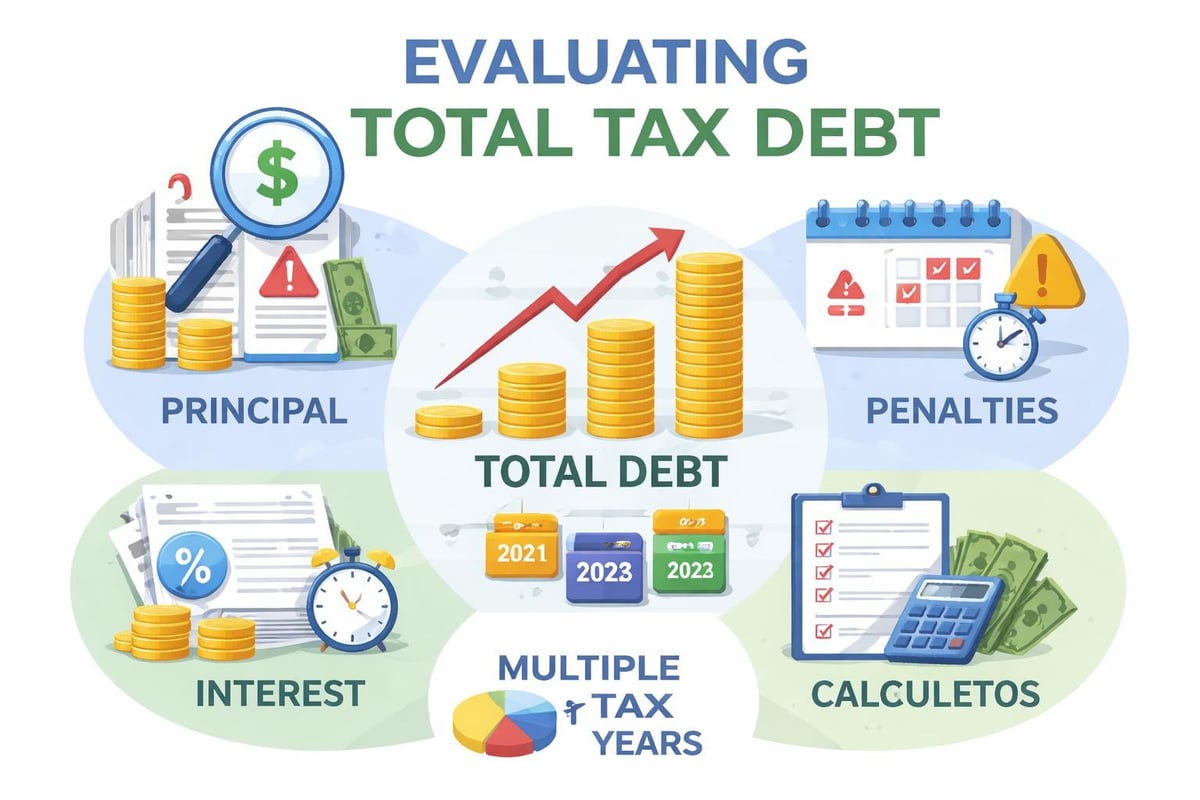

Before exploring relief options, you need a clear picture of exactly what you owe. Tax debt accumulates through unpaid income taxes, self-employment taxes, payroll taxes, or penalties and interest on late payments. The IRS sends notices detailing your balance, but these documents can be confusing and difficult to interpret.

Key information to gather includes:

- Total amount owed, including principal, penalties, and interest

- Tax years involved in the debt

- Type of tax debt (income, employment, business)

- Whether liens or levies have been filed against you

- Current financial status and ability to pay

Your financial situation directly impacts which relief programs you qualify for. The IRS evaluates your income, expenses, assets, and future earning potential when determining eligibility for help paying tax debt. This assessment forms the foundation of any resolution strategy.

Many taxpayers make the mistake of ignoring IRS notices, hoping the problem will resolve itself. Tax debt never disappears on its own. The IRS has a statute of limitations for collection, but during that period (typically 10 years), they can pursue aggressive collection actions that significantly worsen your financial situation.

IRS Payment Plans and Installment Agreements

One of the most accessible forms of help paying tax debt comes through installment agreements, which allow you to pay your balance over time through monthly payments. These agreements work well for taxpayers who cannot pay immediately but have sufficient income to make regular payments.

Short-Term Payment Plans

If you can pay your full tax debt within 180 days, a short-term payment plan offers a straightforward solution. The IRS charges no setup fee for these arrangements, though penalties and interest continue accruing until you pay the balance in full.

Short-term plans work best for temporary cash flow problems, such as unexpected expenses or seasonal income fluctuations. You maintain control over when and how much you pay, as long as you clear the debt within the agreed timeframe.

Long-Term Installment Agreements

For debts requiring more than 180 days to repay, long-term installment agreements provide structured monthly payments. These agreements typically extend up to 72 months, depending on your total debt and financial capacity.

| Agreement Type | Setup Fee | Payment Method | Best For |

|---|---|---|---|

| Direct Debit IA | $31 | Automatic bank withdrawal | Lowest cost option |

| Standard IA | $130 | Manual payments | Those without bank accounts |

| Low-Income IA | $0 | Either method | Taxpayers meeting income thresholds |

The tax relief services available through professional representation can help you negotiate the most favorable payment terms based on your specific circumstances. Tax professionals understand how to present your financial information to maximize approval chances and minimize monthly payment obligations.

Offer in Compromise: Settling for Less

An Offer in Compromise represents one of the most valuable forms of help paying tax debt, allowing qualified taxpayers to settle their obligations for less than the full amount owed. However, the IRS approves only a fraction of submitted offers because strict eligibility requirements apply.

Qualifying for an Offer in Compromise

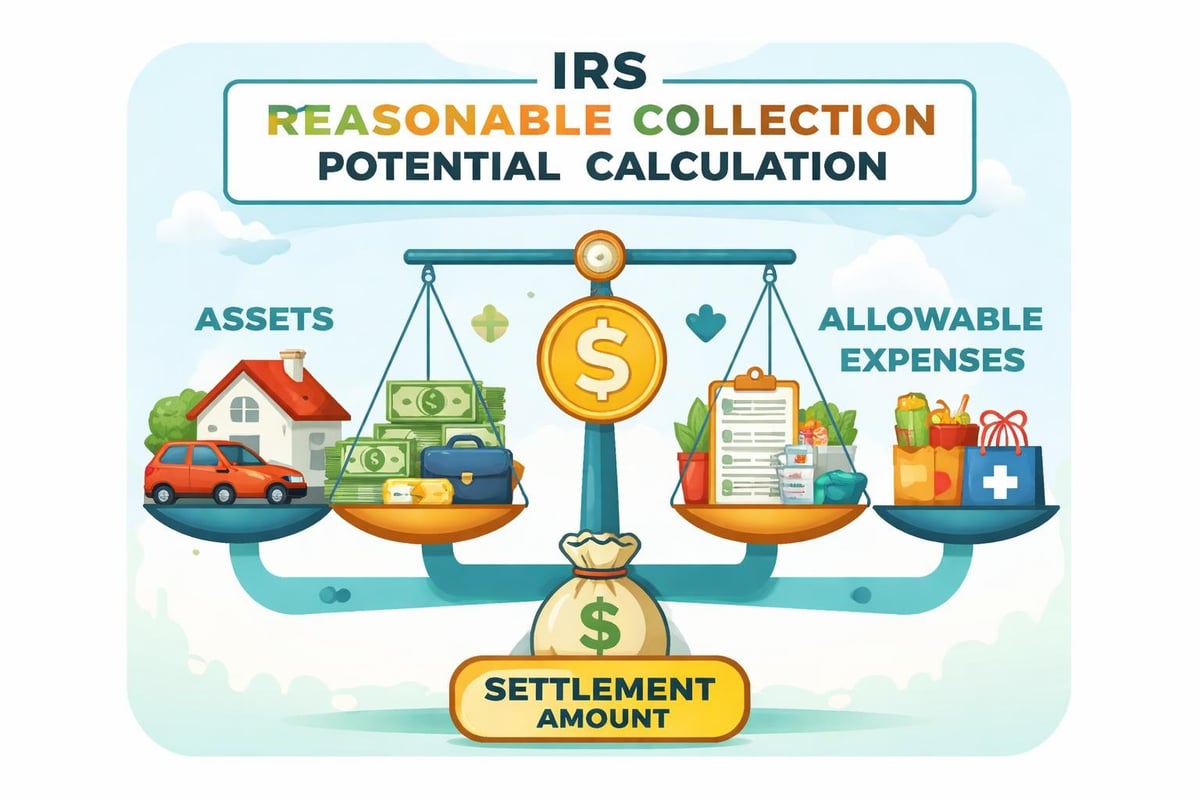

The IRS accepts offers based on doubt as to collectibility, meaning they recognize you cannot pay the full debt now or in the foreseeable future. They calculate what they can reasonably expect to collect by analyzing your assets, income, and expenses.

Factors the IRS considers:

- Total equity in assets (real estate, vehicles, bank accounts, investments)

- Current and projected future income

- Reasonable and necessary living expenses

- Age, health, and ability to earn income

- Special circumstances affecting ability to pay

Your offer amount must reflect your reasonable collection potential (RCP), which equals your total asset equity plus your future income over a specific period. The IRS uses strict formulas to determine RCP, often disallowing expenses they deem unnecessary.

The Offer in Compromise Process

Submitting an offer requires extensive documentation proving your financial situation. You must provide bank statements, pay stubs, asset valuations, and detailed expense reports. Incomplete applications face automatic rejection, wasting months of time while interest and penalties continue accumulating.

The application fee of $205 and initial payment (20% of lump-sum offers or first monthly payment of periodic payment offers) accompany your submission. Low-income taxpayers may qualify for fee waivers based on federal poverty guidelines.

Professional representation significantly improves your chances of offer acceptance. Tax attorneys understand the nuances of IRS financial analysis and can present your case effectively while protecting your rights throughout negotiations.

Currently Not Collectible Status

When you genuinely cannot afford to pay anything toward your tax debt without creating severe financial hardship, the IRS may grant Currently Not Collectible (CNC) status. This designation provides temporary help paying tax obligations by suspending all collection activities until your financial situation improves.

CNC status does not eliminate your debt. Interest and penalties continue accruing, and the collection statute of limitations remains active. However, the IRS will not pursue wage garnishments, bank levies, or other enforcement actions while you maintain this status.

To qualify for CNC status, you must demonstrate that paying any amount toward your tax debt would prevent you from meeting basic living expenses like housing, food, transportation, and medical care. The IRS reviews your financial situation periodically to determine whether you have regained the ability to pay.

Strategic Considerations for CNC Status

Currently Not Collectible status works best as a temporary bridge when facing genuine financial crisis, such as job loss, serious illness, or business failure. It provides breathing room to stabilize your situation without the immediate pressure of IRS collection activities.

However, because your debt continues growing, CNC status should not be viewed as a long-term solution. Once your income increases or circumstances improve, the IRS will resume collection efforts, potentially for a larger amount than your original debt.

Penalty Abatement and Interest Relief

Beyond reducing the principal amount owed, obtaining penalty abatement provides significant help paying tax debt by eliminating or reducing the penalties that can double or triple your original obligation. The IRS assesses various penalties for late filing, late payment, accuracy-related issues, and other violations.

First-Time Penalty Abatement

Taxpayers with a clean compliance history may qualify for administrative relief called First-Time Penalty Abatement (FTA). This one-time benefit removes failure-to-file, failure-to-pay, and failure-to-deposit penalties if you meet specific criteria.

FTA eligibility requirements:

- No penalties for the three tax years prior to the penalty year

- Filed all required returns or filed extensions

- Paid or arranged to pay any tax due

- No current requirement for unfiled returns

First-Time Penalty Abatement represents straightforward help paying tax obligations because it requires no detailed explanation or documentation beyond your compliance history. The IRS grants FTA administratively upon request, provided you meet the basic qualifications.

Reasonable Cause Penalty Abatement

When circumstances beyond your control prevented timely filing or payment, reasonable cause abatement offers another avenue for penalty relief. The IRS considers factors like natural disasters, serious illness, death in the family, inability to obtain records, and reliance on incorrect professional advice.

Unlike FTA, reasonable cause requests require detailed explanations and supporting documentation. You must demonstrate that you exercised ordinary business care and prudence but still could not meet your obligations due to circumstances outside your control.

Innocent Spouse Relief and Separation of Liability

Joint tax returns create joint liability, meaning both spouses are responsible for the full tax debt regardless of who earned the income or made errors. However, specific relief provisions protect innocent spouses from debts they should not reasonably bear.

Innocent Spouse Relief applies when your spouse or former spouse failed to report income, claimed improper deductions, or made other errors without your knowledge. This relief requires proving you did not know and had no reason to know about the understatement when you signed the return.

| Relief Type | Timing | Scope | Requirements |

|---|---|---|---|

| Innocent Spouse | Within 2 years of collection | Removes liability for understatements | Lack of knowledge |

| Separation of Liability | Within 2 years of collection | Allocates debt between spouses | Divorced, separated, or not living together |

| Equitable Relief | Within 10 years or collection period | Broad discretion | Unfair to hold liable |

Equitable relief provides the broadest protection, applying even when other forms of innocent spouse relief do not qualify. The IRS considers all facts and circumstances to determine whether holding you liable would be inequitable.

Working with Tax Professionals for Resolution

Professional representation provides invaluable help paying tax debt through expert negotiation, legal protection, and strategic planning. Tax attorneys, enrolled agents, and CPAs authorized to practice before the IRS understand the complexities of tax law and collection procedures that most taxpayers find overwhelming.

Benefits of Professional Representation

Tax professionals serve as your advocate with the IRS, handling all communications and negotiations on your behalf. This representation protects you from making statements that could harm your case and ensures your rights are preserved throughout the resolution process.

Professional services include:

- Comprehensive financial analysis to determine optimal resolution strategy

- Preparation and submission of offers in compromise

- Negotiation of installment agreement terms

- Requests for penalty abatement and interest relief

- Audit representation and appeals

- Protection from aggressive collection actions

- Defense against criminal tax investigations

The Taxpayer Advocate Service provides free assistance to taxpayers experiencing financial difficulty or system problems. However, for complex debt resolution involving significant amounts or multiple tax years, professional representation offers advantages that free services cannot match.

When to Seek Professional Help

Certain situations demand professional expertise rather than attempting to navigate the process alone. If you owe more than $10,000, face liens or levies, are under audit, or have unfiled returns combined with tax debt, professional representation becomes essential rather than optional.

Business owners dealing with payroll tax issues face particularly serious consequences, including personal liability for trust fund recovery penalties. These situations require immediate professional intervention to protect both your business and personal assets.

The tax resources available through established tax resolution firms provide education while offering pathways to professional assistance tailored to your specific circumstances.

Wage Garnishment and Levy Release

When you cannot afford help paying tax obligations and collection efforts escalate, the IRS may initiate wage garnishments or bank levies. These aggressive actions can devastate your financial stability, taking a significant portion of your paycheck or freezing your bank accounts.

Understanding Wage Garnishments

IRS wage garnishments differ from other creditor garnishments because they take a much larger percentage of your income. The IRS uses Publication 1494 tables to determine how much of your wages to exempt based on your filing status and number of dependents, often leaving taxpayers with insufficient income to cover basic living expenses.

You have rights when facing garnishment. The IRS must provide notice and opportunity to make payment arrangements before initiating wage levies. If garnishment has already begun, you can request release by entering into an installment agreement, proving financial hardship, or demonstrating the levy creates economic hardship.

Strategies for Levy Release

Bank levies freeze your account for 21 days before the bank sends funds to the IRS. During this window, you can take action to release the levy and recover your funds. Immediate response is critical because once the bank transfers money to the IRS, recovering those funds becomes extremely difficult.

Professional representation expedites the levy release process. Tax attorneys understand the procedures and documentation required to prove hardship and negotiate levy releases while establishing sustainable payment solutions.

Bankruptcy and Tax Debt

Bankruptcy provides help paying tax debt in specific circumstances, though most people incorrectly believe tax debts cannot be discharged in bankruptcy. While bankruptcy offers limited relief for tax obligations, certain income tax debts may be eliminated through Chapter 7 or Chapter 13 bankruptcy filings.

Qualifying Tax Debt for Bankruptcy Discharge

Income tax debt may be dischargeable if it meets specific criteria. The debt must be at least three years old (from the original due date of the return), you must have filed the return at least two years before filing bankruptcy, and the IRS must have assessed the tax at least 240 days before your bankruptcy filing.

Additional requirements include no fraudulent returns or tax evasion attempts. Even when income taxes qualify for discharge, other tax obligations like payroll taxes, trust fund recovery penalties, and recent income taxes remain non-dischargeable.

Chapter 13 bankruptcy offers an alternative approach, creating a repayment plan that may reduce tax penalties and interest while providing protection from collection actions during the plan period.

State Tax Debt Resolution

While this discussion focuses primarily on IRS debt, state tax obligations create similar burdens requiring resolution. State tax agencies offer programs analogous to federal options, including payment plans, offer in compromise programs, and penalty abatement.

Each state operates differently, with varying qualification criteria, application processes, and negotiation flexibility. Some states prove more willing to negotiate than others, while certain jurisdictions pursue aggressive collection actions similar to or exceeding IRS efforts.

Professional representation becomes particularly valuable when dealing with multiple tax jurisdictions. Coordinating resolution strategies for both federal and state debts requires careful planning to avoid conflicting agreements or unmanageable payment obligations.

Preventing Future Tax Debt

While addressing current tax debt is critical, preventing future accumulation is equally important. Many taxpayers resolve one tax debt only to face new obligations because they have not corrected the underlying problems causing tax shortfalls.

Prevention strategies include:

- Adjusting withholding to cover full tax liability

- Making quarterly estimated tax payments for self-employment income

- Setting aside tax reserves for business income

- Maintaining accurate records and timely filing

- Consulting tax professionals before major financial decisions

- Addressing unfiled returns immediately

Proactive tax planning costs far less than resolving tax debt after it accumulates. Working with tax professionals on an ongoing basis helps identify potential issues before they become serious problems requiring extensive resolution efforts.

The consequences of unresolved tax debt extend beyond financial penalties. Tax liens damage your credit, making it difficult to obtain financing, rent housing, or secure certain professional licenses. Levies can result in lost wages, seized bank accounts, and even property forfeiture.

Moving Forward with Tax Debt Resolution

Taking action represents the most important step when facing tax debt. The longer you wait, the more your debt grows and the fewer options remain available. The IRS collection statute of limitations runs for 10 years, but during that period, they possess extraordinary collection powers exceeding those of private creditors.

Help paying tax obligations exists through multiple programs and strategies, each designed for different financial circumstances. Determining the right approach requires honest assessment of your financial situation, understanding of available options, and often professional guidance to navigate complex procedures.

Whether you pursue an installment agreement, offer in compromise, currently not collectible status, penalty abatement, or another resolution strategy, the key is addressing your tax debt rather than avoiding it. The IRS proves far more willing to work with taxpayers who proactively seek solutions than those who ignore notices and collection attempts.

For additional information about navigating tax resolution, visit the CLAW Tax Group blog for resources and guidance on managing tax obligations effectively.

Resolving tax debt requires understanding your options and taking decisive action before collection activities escalate. Whether you need help paying tax obligations through installment agreements, offers in compromise, or other relief programs, professional guidance ensures you choose the most effective strategy for your situation. CLAW Tax Group specializes in tax resolution and legal representation, offering personalized solutions including payment plans, settlement negotiations, and defense against IRS enforcement actions. Contact our experienced team today to explore how we can help reduce your tax burden and protect your financial future.