Facing tax debt can be one of the most stressful financial situations for individuals and businesses. When you discover you have IRS owed taxes, the immediate reaction often involves anxiety about penalties, interest accumulation, and potential enforcement actions. However, understanding your options and taking proactive steps can transform this challenging situation into a manageable financial obligation. The IRS provides several resolution pathways, and professional tax resolution services can help you navigate these options to find the most favorable outcome for your specific circumstances.

Understanding Your IRS Tax Debt Situation

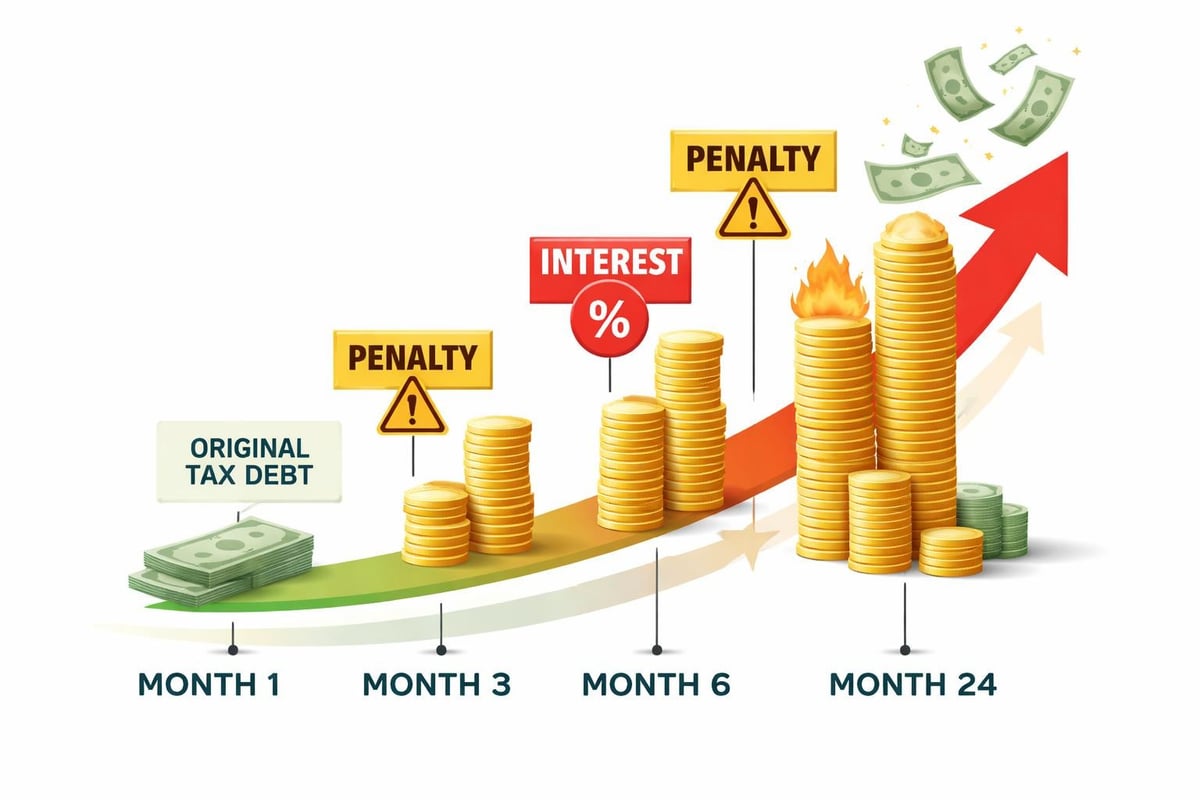

When the IRS determines you have unpaid tax liabilities, several factors come into play that affect both the amount you owe and the urgency of resolution. The IRS adds penalties and interest to your original tax debt, which compounds over time and significantly increases the total amount of irs owed taxes.

How IRS Tax Debt Accumulates

The calculation of tax debt goes beyond the original amount shown on your return. The IRS applies a failure-to-pay penalty of 0.5% per month on unpaid balances, up to a maximum of 25% of the original tax due. Additionally, interest compounds daily on both the unpaid tax and penalties, creating a snowball effect that makes early intervention critical.

Key components of tax debt include:

- Original tax liability from your return

- Failure-to-pay penalties (0.5% monthly)

- Failure-to-file penalties (5% monthly, if applicable)

- Daily compounding interest based on federal short-term rates

- Additional penalties for specific violations

The time frame for IRS collection activities extends for ten years from the date of assessment, giving the agency substantial time to pursue outstanding balances. Understanding this timeline is crucial when evaluating your resolution options.

Payment Plans and Installment Agreements

For taxpayers who cannot pay their full tax debt immediately, Installment Agreements offer a structured path to resolution. These arrangements allow you to pay your irs owed taxes over time through monthly payments, preventing more aggressive collection actions.

Short-Term Payment Plans

If you can pay your full balance within 180 days, a short-term payment plan may be appropriate. This option requires no setup fee and provides breathing room to arrange funds without entering a long-term commitment. The IRS continues to add penalties and interest during this period, but you avoid the formal Installment Agreement process.

Long-Term Installment Agreements

For balances exceeding what you can pay within six months, long-term Installment Agreements extend payment periods up to 72 months or longer in certain cases. These agreements come in several varieties:

| Agreement Type | Maximum Debt | Setup Fee | Requirements |

|---|---|---|---|

| Streamlined | $50,000 or less | $31-$225 | Minimal financial disclosure |

| Partial Payment | Any amount | $225 | Extensive financial disclosure |

| Non-Streamlined | Over $50,000 | $225 | Complete financial analysis |

The monthly payment amount depends on your financial situation, outstanding balance, and the type of agreement. Streamlined agreements generally use a formula dividing your balance by 72 months, while partial payment arrangements consider your income, expenses, and asset equity to determine what you can reasonably afford.

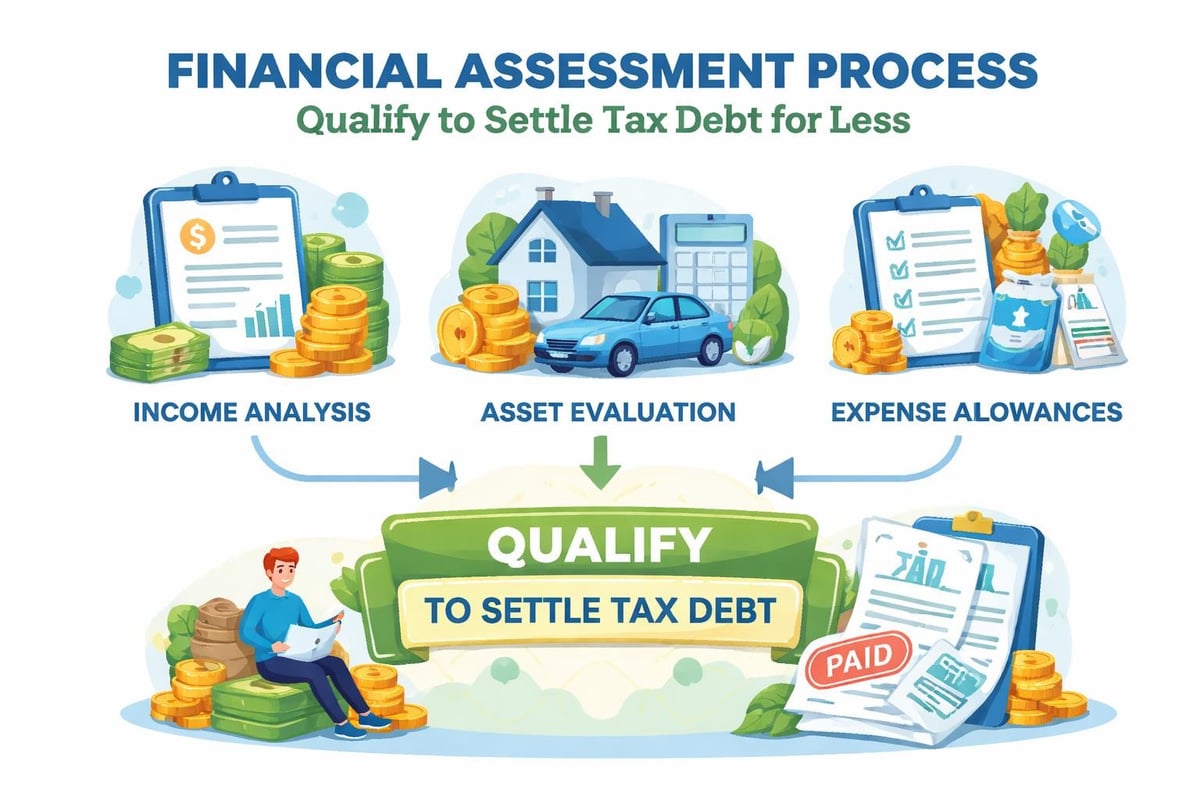

Offers in Compromise: Settling for Less

An Offer in Compromise (OIC) represents one of the most powerful tools for resolving substantial irs owed taxes when full payment creates financial hardship. This program allows qualifying taxpayers to settle their debt for less than the full amount owed.

Eligibility Requirements

The IRS evaluates OIC applications based on doubt as to collectibility, meaning they determine whether collecting the full amount would create economic hardship. Your reasonable collection potential (RCP) becomes the central calculation, factoring in your equity in assets, future income potential, and basic living expenses.

Critical eligibility factors include:

- Current compliance with all filing requirements

- No open bankruptcy proceedings

- All required estimated tax payments made for current year

- Valid extension filed if submitting during filing season

The acceptance rate for Offers in Compromise hovers around 33%, making professional representation valuable for maximizing approval chances. Tax resolution experts understand how to present your financial situation most favorably and navigate the complex calculation methods the IRS employs.

The OIC Application Process

Submitting an Offer in Compromise requires meticulous documentation and strategic presentation. The application package includes detailed financial statements, proof of income and expenses, asset valuations, and a calculated offer amount based on your RCP.

The IRS typically takes six to twelve months to evaluate applications, during which collection activities generally pause. If accepted, you must comply with all tax obligations for the next five years, or the offer may be revoked and your original debt reinstated.

Currently Not Collectible Status

When financial hardship makes any payment toward your irs owed taxes impossible, Currently Not Collectible (CNC) status provides temporary relief from IRS collection activities. This designation acknowledges that collecting from you would create undue economic hardship.

Qualifying for CNC Status

The IRS evaluates your income against allowable living expenses to determine if collection should be temporarily suspended. If your monthly income barely covers or falls short of necessary expenses for housing, food, transportation, and healthcare, you may qualify for this status.

While in CNC status, the IRS halts levies, wage garnishments, and other enforcement actions. However, penalties and interest continue accruing, and the IRS may file a federal tax lien to secure their interest in your assets. The agency also periodically reviews your financial situation, typically every two years, to determine if your circumstances have improved.

Penalty Abatement Strategies

Reducing or eliminating penalties can significantly decrease your total irs owed taxes. The IRS offers several penalty relief programs, with first-time penalty abatement being the most accessible for taxpayers with clean compliance histories.

First-Time Penalty Abatement

Taxpayers who have filed and paid on time for the previous three years and have no current penalties may qualify for administrative penalty relief. This provision can remove failure-to-file and failure-to-pay penalties for a single tax year, potentially saving thousands of dollars.

Requirements for first-time abatement:

- Clean compliance history for past three years

- Current with all filing requirements

- Current with payment obligations or under an approved payment plan

- No previous penalty abatement in recent years

Reasonable Cause Penalty Relief

Beyond first-time abatement, the IRS may remove penalties if you can demonstrate reasonable cause for late payment or filing. Acceptable reasons include serious illness, death in the family, natural disasters, or reliance on incorrect advice from tax professionals.

Documentation supporting your reasonable cause claim strengthens your case significantly. Medical records, death certificates, disaster declarations, or correspondence with tax advisors can substantiate your request.

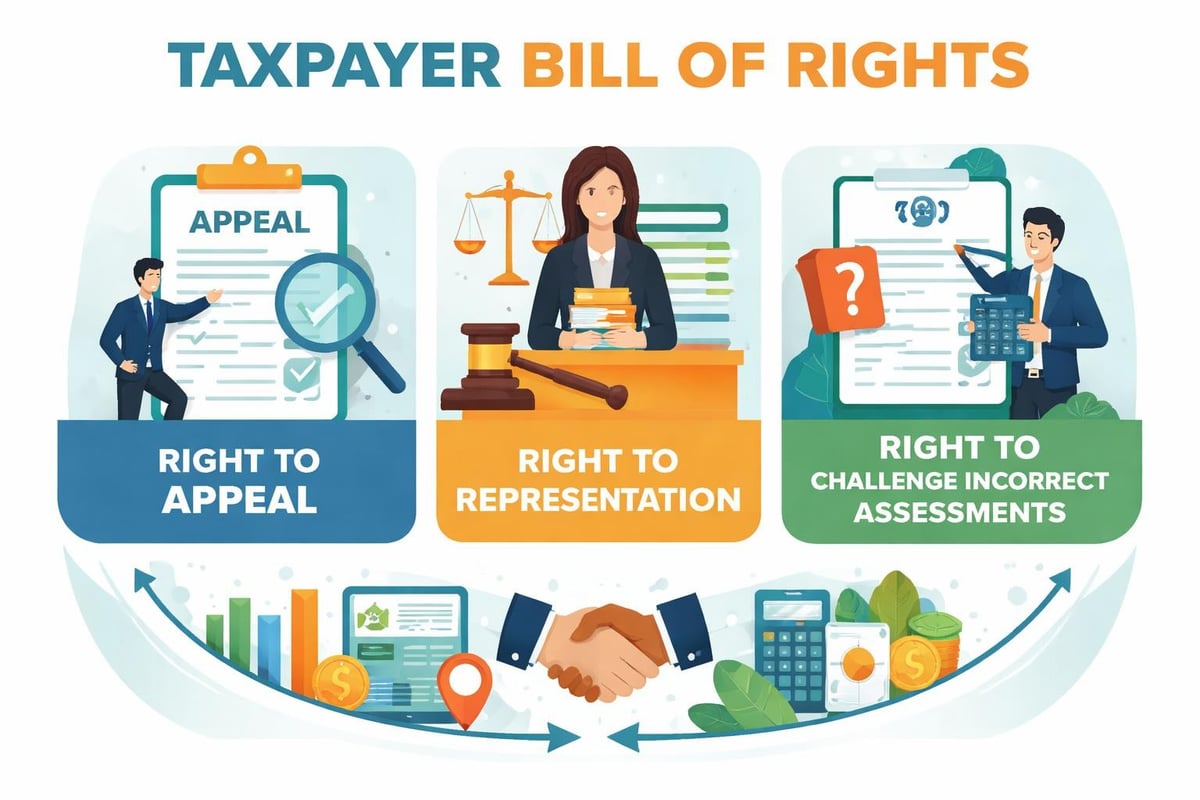

Protecting Your Rights During Tax Debt Resolution

Taxpayers dealing with irs owed taxes maintain specific rights throughout the collection process. The Taxpayer Bill of Rights guarantees fair treatment, including the right to pay no more than the correct amount of taxes owed.

Collection Due Process Rights

Before the IRS can levy your assets or wages, they must provide notice and opportunity for a Collection Due Process (CDP) hearing. This hearing allows you to challenge the collection action, propose alternative payment arrangements, or dispute the underlying tax liability.

Requesting a CDP hearing within 30 days of receiving a final notice of intent to levy automatically stays enforcement action while your case is reviewed. Independent appeals officers evaluate your financial situation and the appropriateness of proposed collection alternatives.

Audit Reconsideration and Amended Returns

If you believe your tax assessment is incorrect, you can challenge the amount through audit reconsideration or filing an amended return. Audit reconsideration applies when you have new information that wasn't considered during the original examination or when you failed to respond to the initial audit notice.

Filing an amended return using Form 1040-X allows you to correct errors, claim overlooked deductions or credits, and potentially reduce your liability. The IRS has three years from the original filing deadline to process refund claims, making timely action essential.

Avoiding Tax Scams While Resolving Debt

Taxpayers struggling with tax debt become prime targets for scams. Understanding how to recognize and avoid tax scams protects you from compounding your financial difficulties.

Common Tax Relief Scams

Fraudulent tax resolution companies make unrealistic promises, such as guaranteeing Offer in Compromise acceptance or claiming they can eliminate your debt for pennies on the dollar without reviewing your financial situation. These operations often charge substantial upfront fees before providing little or no actual service.

Red flags indicating potential scams:

- Guarantees of specific outcomes before reviewing your case

- Requests for large upfront payments before work begins

- Claims they have "special relationships" with IRS employees

- Pressure to hire immediately without time for research

- Unwillingness to provide credentials or references

Legitimate tax professionals conduct thorough financial analyses before recommending strategies and clearly explain the requirements, costs, and realistic outcomes for each option. They also maintain proper credentials, such as Enrolled Agent status, CPA licenses, or tax attorney bar admissions.

Liens, Levies, and Asset Protection

When irs owed taxes remain unresolved, the IRS escalates collection efforts through liens and levies. Understanding these enforcement tools helps you respond appropriately and protect your assets.

Federal Tax Liens

A federal tax lien represents the government's legal claim against your property when you neglect or refuse to pay tax debt. The IRS files a Notice of Federal Tax Lien with local authorities, creating a public record that affects your credit and ability to sell or refinance property.

Tax liens attach to all current and future assets, including real estate, vehicles, securities, and business property. While liens don't immediately seize assets, they take priority over most other creditors and complicate financial transactions.

You can request lien withdrawal after satisfying certain conditions, such as entering a Direct Debit Installment Agreement or demonstrating that withdrawal facilitates tax collection. Subordination and discharge options also exist for specific situations involving property sales or refinancing.

IRS Levies and Wage Garnishment

Levies represent actual seizure of property to satisfy tax debt. The IRS can levy bank accounts, wages, retirement accounts, and physical property. Getting help with tax debt before levies occur prevents the financial disruption they cause.

Wage garnishments leave you with only a small portion of your paycheck based on filing status and dependents, creating immediate financial crisis for most taxpayers. Bank levies freeze accounts and allow the IRS to seize the full balance after a 21-day waiting period.

Importance of Professional Representation

Navigating tax debt resolution requires understanding complex IRS procedures, negotiation strategies, and legal protections. Professional representation from tax attorneys, enrolled agents, or CPAs specializing in tax resolution significantly improves outcomes.

Benefits of Expert Tax Resolution Services

Tax professionals bring several advantages to your case. They communicate directly with the IRS on your behalf, relieving you of stressful interactions with collection agents. Their experience with IRS systems and personnel helps expedite resolutions and avoid common pitfalls that delay cases or result in rejections.

| Service Type | Best For | Key Advantages |

|---|---|---|

| Tax Attorney | Complex cases, legal issues | Attorney-client privilege, litigation |

| Enrolled Agent | Most resolution needs | IRS representation rights, affordability |

| CPA | Financial analysis, business taxes | Accounting expertise, business focus |

Professionals also provide strategic advice on timing, payment structuring, and which resolution option best fits your long-term financial goals. They identify opportunities for penalty abatement, statute of limitations considerations, and potential defenses against collection that taxpayers typically overlook.

Business Tax Debt Considerations

Businesses facing irs owed taxes encounter additional complications beyond individual taxpayers. Payroll tax debt carries severe consequences, including personal liability for business owners and Trust Fund Recovery Penalty assessments.

Payroll Tax Obligations

Employment taxes withheld from employee paychecks are held in trust for the government. Failure to remit these taxes on time results in Trust Fund Recovery Penalty assessments against responsible parties, making business owners, officers, and sometimes employees personally liable for the debt.

The IRS pursues payroll tax debt aggressively, often moving to enforcement actions more quickly than with income tax debt. Maintaining current payroll tax compliance is essential, as the IRS typically won't negotiate resolution for back taxes while you're accumulating new debt.

Business Resolution Options

Businesses can access the same resolution tools as individuals, including Installment Agreements and Offers in Compromise. However, business OICs face more scrutiny, particularly regarding asset valuations and going concern value for operating entities.

For struggling businesses, strategic decisions about entity dissolution, bankruptcy, or restructuring interact with tax debt resolution planning. Professional guidance helps you understand how business decisions affect both business and personal tax liabilities, especially for pass-through entities where business income flows to personal returns.

Preventing Future Tax Debt

After resolving current irs owed taxes, implementing systems to prevent recurrence protects your financial stability. The strategies that prevent new tax debt are often simpler than the resolution process you've just completed.

Estimated Tax Payments

Self-employed individuals and those with substantial non-wage income must make quarterly estimated tax payments. Underpayment creates tax bills at filing time, potentially restarting the debt cycle. The IRS expects payments by April 15, June 15, September 15, and January 15, covering income not subject to withholding.

Calculating estimated payments requires projecting annual income and deductions, which challenges taxpayers with variable income. Using safe harbor provisions based on prior year tax provides certainty, even if you overpay slightly.

Withholding Adjustments

Employees can prevent year-end tax surprises by reviewing and adjusting W-4 withholding elections. Life changes like marriage, divorce, additional income sources, or major deductions warrant withholding reviews to ensure adequate tax coverage throughout the year.

The IRS provides a withholding estimator tool that helps you calculate appropriate withholding based on your specific situation. Reviewing withholding mid-year allows time to correct any shortfalls before year-end.

Tax planning best practices:

- Review tax situation quarterly, not just at year-end

- Set aside tax reserves for self-employment and investment income

- Maintain organized records throughout the year

- Consult tax professionals for major financial changes

- File and pay on time, even if you can't pay the full amount

Understanding that paying taxes on time prevents penalties and interest accumulation reinforces the importance of timely compliance.

Bankruptcy and Tax Debt

Bankruptcy offers limited relief for tax debt, with strict requirements determining which taxes can be discharged. Understanding how bankruptcy intersects with tax resolution helps you evaluate whether this option serves your overall financial recovery.

Dischargeable Tax Debt Requirements

For income tax debt to be discharged in bankruptcy, it must meet all of the following conditions: the tax year is at least three years before filing bankruptcy, you filed the return at least two years before bankruptcy, the IRS assessed the tax at least 240 days before bankruptcy, and the return wasn't fraudulent.

Even meeting these criteria, tax liens survive bankruptcy. While the personal obligation to pay may be discharged, liens remain attached to property owned when bankruptcy was filed, requiring satisfaction before you can sell or refinance.

Bankruptcy vs. Tax Resolution

For most taxpayers, traditional tax resolution provides better outcomes than bankruptcy. Offers in Compromise can eliminate tax debt without the broad financial consequences of bankruptcy, and Installment Agreements preserve your credit and financial flexibility while resolving debt over time.

However, when tax debt combines with substantial other debts and you meet the discharge criteria, bankruptcy might be appropriate. Professional analysis comparing tax resolution options against bankruptcy helps you make informed decisions aligned with your complete financial picture.

Working with CLAW Tax Group for Resolution

Professional tax resolution services provide invaluable support when dealing with irs owed taxes. Experienced representatives understand IRS procedures, negotiation tactics, and legal protections that maximize favorable outcomes while minimizing stress and time investment.

Comprehensive Case Evaluation

Effective resolution begins with thorough analysis of your tax situation, financial position, and resolution options. Professional representatives review your tax history, collection notices, income and assets, and personal circumstances to identify the most advantageous strategy.

This evaluation considers both immediate relief and long-term financial impact. The goal extends beyond merely resolving current debt to establishing sustainable compliance and preventing future tax problems.

Negotiation and Implementation

Once a strategy is identified, professionals handle all IRS communications, prepare required documentation, and negotiate on your behalf. Their experience navigating IRS systems and understanding what appeals to collection personnel improves acceptance rates and speeds resolution.

Throughout the process, you receive updates on case progress and guidance on maintaining compliance with agreement terms. This support continues until full resolution, ensuring you successfully exit the tax debt situation.

Resolving IRS tax matters requires expertise, persistence, and strategic planning. Professional representation transforms an overwhelming situation into a manageable process with a clear path to financial recovery.

Addressing irs owed taxes requires understanding your options, acting promptly, and seeking professional guidance when needed. Whether through payment plans, Offers in Compromise, or other resolution strategies, pathways exist to resolve even substantial tax debt while protecting your financial future. CLAW Tax Group specializes in helping individuals and businesses navigate complex tax debt situations with proven strategies including Offers in Compromise, Installment Agreements, and comprehensive legal representation. If you're facing tax debt challenges, contact our experienced team today to explore your resolution options and take the first step toward financial peace of mind.