Facing a tax bill you cannot pay in full can feel overwhelming, but the IRS offers multiple payment options designed to help taxpayers settle their obligations without financial catastrophe. Whether you owe a few thousand dollars or face significant tax debt, understanding how to irs set up payments properly can prevent aggressive collection actions, reduce penalties, and provide breathing room to regain financial stability. The process has become increasingly accessible through digital tools, though navigating the requirements and selecting the right payment structure requires careful consideration of your financial situation and long-term goals.

Understanding IRS Payment Plan Options

The IRS provides several structured payment arrangements, each designed for different financial circumstances and debt levels. Knowing which option aligns with your situation is the first step toward resolving tax debt effectively.

Short-Term Payment Plans

For taxpayers who can pay their full balance within 180 days, short-term payment plans offer the simplest solution. These arrangements carry no setup fee and allow you to make multiple payments over a period not exceeding six months. The IRS continues to assess penalties and interest during this time, but the rates remain lower than those associated with collection enforcement actions.

Eligibility requirements include:

- Total combined tax, penalties, and interest less than $100,000

- Current on all tax return filings

- No other active payment plans with the IRS

This option works well for taxpayers experiencing temporary cash flow issues rather than chronic financial hardship. Many individuals use short-term plans when waiting for asset liquidation, business receivables, or other expected income.

Long-Term Installment Agreements

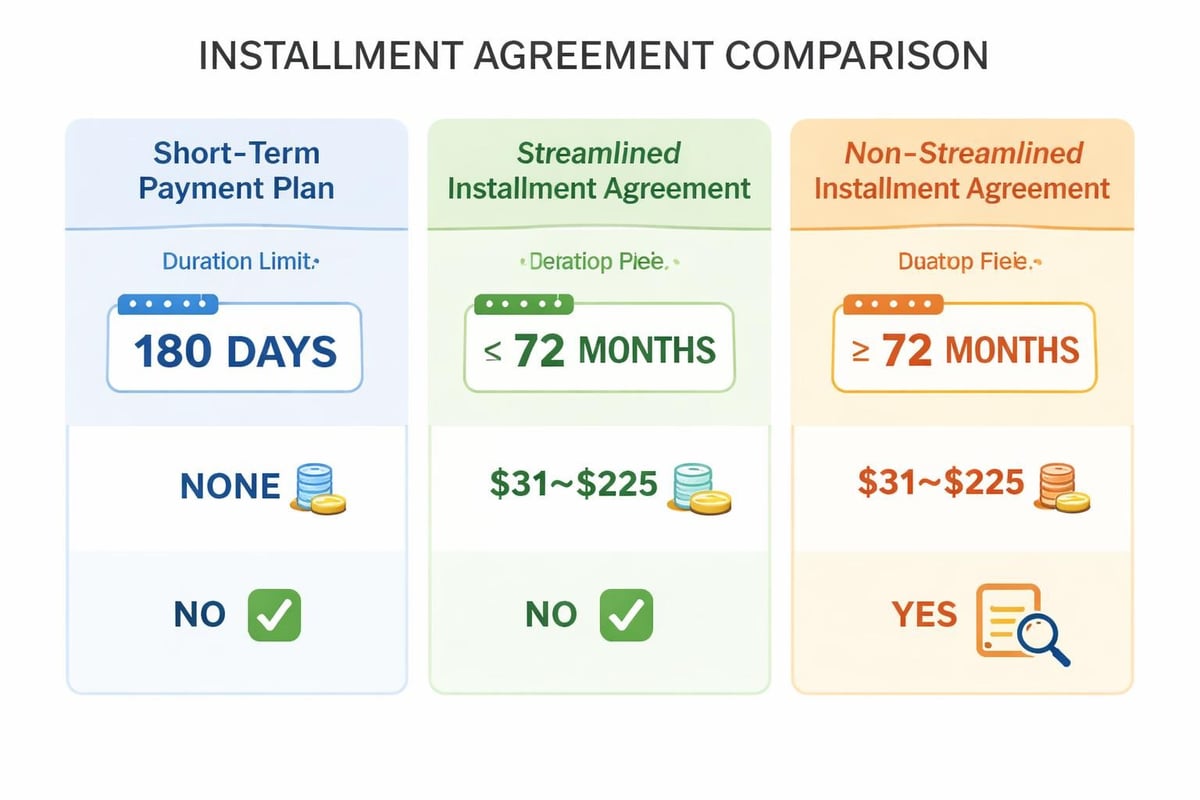

When you need more than 180 days to pay your tax debt, long-term installment agreements provide structured monthly payments extending up to 72 months in some cases. These agreements come with setup fees ranging from $31 to $225, depending on your payment method and application channel.

The IRS offers streamlined approval for qualified taxpayers through online payment agreement applications, making the process faster than traditional mail submissions. Processing times for online applications typically take just minutes, compared to weeks for paper submissions.

| Agreement Type | Maximum Debt | Duration | Setup Fee | Financial Statement Required |

|---|---|---|---|---|

| Short-Term | $100,000 | 180 days | $0 | No |

| Streamlined | $50,000 | 72 months | $31-$225 | No |

| Non-Streamlined | Over $50,000 | Varies | $225 | Yes |

| Partial Payment | Any amount | Until collection statute expires | $225 | Yes |

Guaranteed Installment Agreements

Taxpayers owing $10,000 or less qualify for guaranteed installment agreements if they meet specific criteria. The IRS must approve these applications as long as you have filed all required returns, demonstrate ability to pay the balance within three years, and have not entered into an installment agreement in the past five years.

This guarantee removes much of the uncertainty from the application process, though you still must propose reasonable monthly payments that satisfy the debt within the 36-month window.

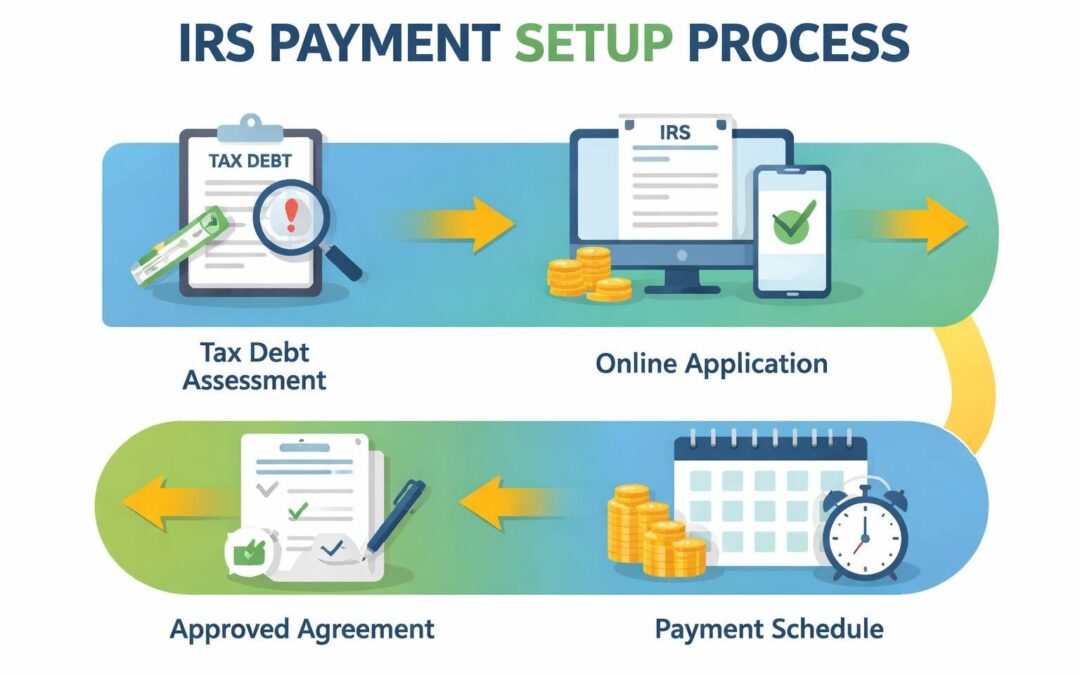

How to IRS Set Up Payments Online

The fastest and most efficient method to irs set up payments involves using the IRS online payment application portal. This digital approach offers immediate determination for many taxpayers and eliminates processing delays associated with mail correspondence.

Step-by-Step Online Application Process

Begin by gathering essential information before starting your application. You will need your Social Security number or employer identification number, filing status from your most recent tax return, and the specific tax year and form number for the balance you owe.

Required information includes:

- Personal identification details

- Bank account and routing numbers (for direct debit arrangements)

- Proposed monthly payment amount

- Preferred payment date each month

Navigate to the IRS payment plan application page and select the appropriate taxpayer type. Individual taxpayers and business owners follow slightly different paths, though the core information requirements remain similar. The system will verify your account status and confirm eligibility for streamlined processing before allowing you to continue.

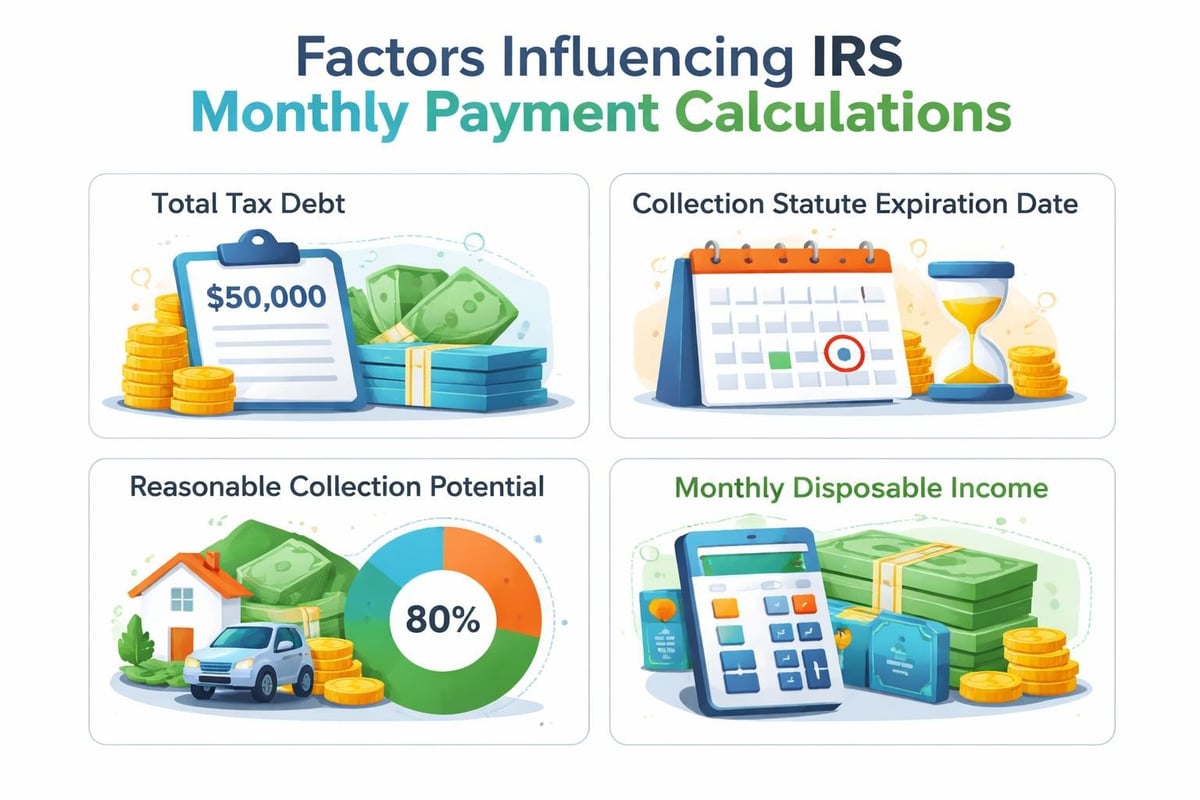

Calculate your minimum monthly payment by dividing your total balance by the maximum number of months allowed for your situation. The IRS typically requires payment sufficient to satisfy the debt before the collection statute expiration date, which falls ten years after assessment in most cases.

Choosing Your Payment Method

Direct debit from your checking account offers the lowest setup fee at $31 for online applications, compared to $130 for non-direct-debit payment methods. Beyond cost savings, automatic withdrawals reduce the risk of missed payments that could trigger default status and resume collection activities.

Alternative payment methods include payroll deductions, check payments, money orders, and same-day wire transfers. Each carries different processing timelines and fee structures. The IRS payment plan options provide comprehensive details about each method's specific requirements.

Calculating Affordable Monthly Payments

Determining the right monthly payment amount requires balancing IRS requirements with your genuine financial capacity. Setting payments too high creates default risk, while unnecessarily low payments extend your debt burden and increase total interest costs.

Financial Assessment Considerations

For streamlined installment agreements under $50,000, the IRS does not require detailed financial statements. You can propose payments that satisfy the balance within 72 months without submitting Collection Information Statements. This simplified approach works well for taxpayers with straightforward financial situations.

When requesting non-streamlined agreements or partial payment arrangements, you must complete Form 433-F (Collection Information Statement) for individuals or Form 433-B for businesses. These comprehensive financial disclosures examine income, expenses, assets, and liabilities to determine your reasonable collection potential.

The IRS uses national and local standard expense allowances when evaluating financial statements. These standardized amounts apply to categories like housing, transportation, food, and healthcare. Actual expenses exceeding standards require documentation and justification.

Key financial factors reviewed:

- Monthly gross income from all sources

- Necessary living expenses (housing, utilities, food, transportation)

- Other debt obligations

- Asset equity available for liquidation

- Future income potential

Strategic Payment Planning

Consider the trade-offs between higher monthly payments that resolve debt quickly versus lower payments that preserve cash flow for business operations or emergency reserves. Many taxpayers benefit from professional guidance when structuring payment plans, particularly when dealing with complex audit situations or multiple tax years.

Setting payment dates early in the month, shortly after receiving regular income, reduces the temptation to spend funds earmarked for tax obligations. This timing also aligns with most individuals' paycheck schedules, making budgeting more predictable.

Managing Your Payment Agreement

Once approved, maintaining your installment agreement in good standing requires consistent compliance with both payment obligations and ongoing tax responsibilities. Failure to meet these requirements can result in default status and resumption of IRS collection activities.

Compliance Requirements

All payment agreements carry the condition that you must file all required tax returns on time and pay any newly accruing tax liabilities in full by their due dates. This means maintaining current compliance even while paying down past-due balances.

For business owners, this dual obligation can strain cash flow, requiring careful budgeting to satisfy both current tax deposits and installment payments. Quarterly estimated tax payments for self-employed individuals deserve particular attention, as underpayment can create new balances that jeopardize existing agreements.

The IRS continues assessing penalties and interest throughout your payment plan period. The failure-to-pay penalty typically runs at 0.25% per month (reduced from 0.5% while an installment agreement remains active), while interest compounds daily at the federal short-term rate plus three percentage points.

Modifying or Reinstating Agreements

Life circumstances change, and the IRS recognizes that payment amounts initially affordable may become burdensome due to job loss, medical emergencies, or business downturns. You can request payment plan modifications through the same online portal used for initial applications.

Reinstatement options exist for taxpayers who default on payment agreements due to temporary financial setbacks. The IRS may approve reinstatement if you can demonstrate that default resulted from circumstances beyond your control and that you can now maintain consistent payments.

Missing a single payment does not automatically trigger default. The IRS typically sends default notices providing 30 days to cure the missed payment before terminating the agreement. Responding quickly to these notices often prevents escalation to enforced collection.

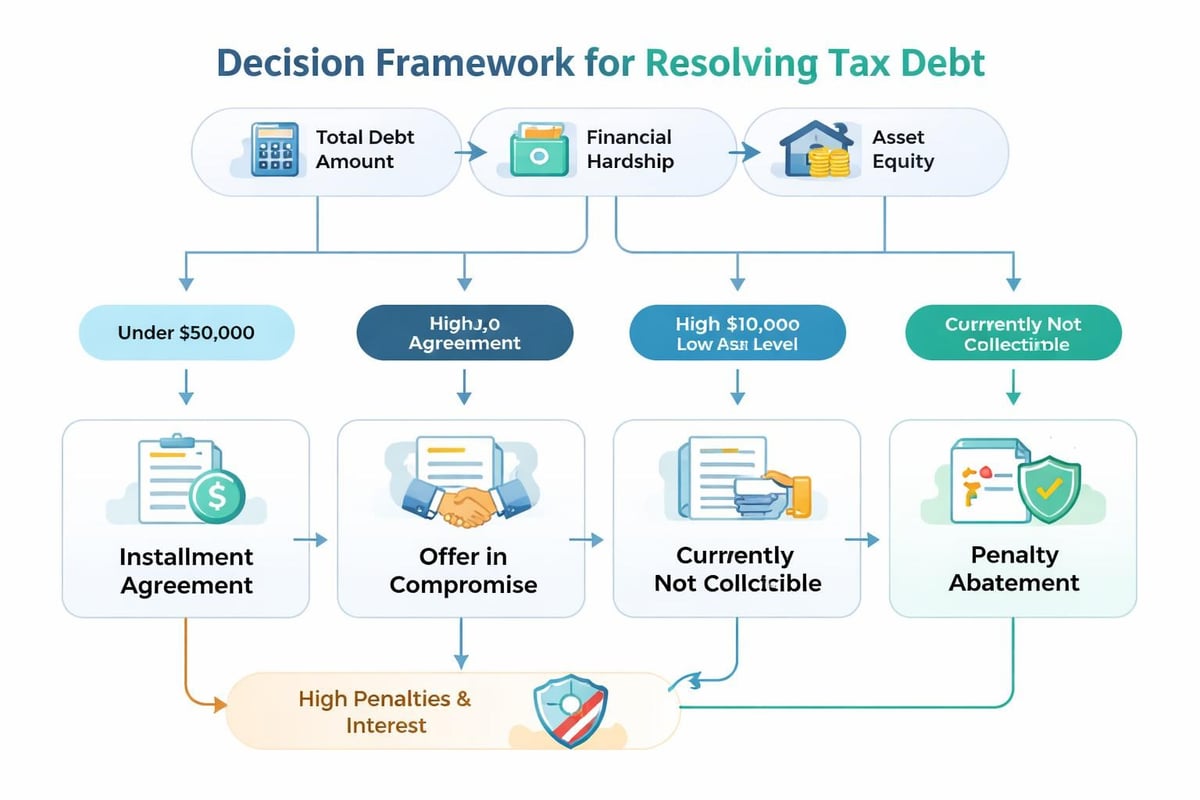

Alternative Resolution Options Beyond Standard Payment Plans

While installment agreements work for many taxpayers, they represent just one tool in the broader tax resolution landscape. Certain situations call for different approaches that may reduce total debt or provide more favorable terms.

Offers in Compromise

When full payment creates genuine economic hardship, Offers in Compromise allow qualified taxpayers to settle tax debts for less than the full amount owed. The IRS accepts these offers when the amount proposed represents the maximum they could reasonably collect before the collection statute expires.

The application process requires extensive financial disclosure, application fees, and initial payments. Approval rates remain relatively low, with the IRS rejecting offers that fail to meet minimum reasonable collection potential thresholds. Professional representation significantly improves approval odds by ensuring proper documentation and strategic positioning.

Currently Not Collectible Status

Taxpayers experiencing severe financial hardship with no ability to make payments may qualify for Currently Not Collectible (CNC) status. This designation temporarily suspends IRS collection activities, though the debt remains valid and continues accruing interest.

The IRS periodically reviews CNC accounts to determine whether financial circumstances have improved sufficiently to resume collection. This status works best as a temporary measure while addressing underlying financial issues, not as a permanent solution.

Penalty Abatement Strategies

First-time penalty abatement provides relief for taxpayers with clean compliance history who face penalties for a single tax year. Successfully removing failure-to-file and failure-to-pay penalties can reduce total debt substantially, making standard payment plans more manageable.

Reasonable cause penalty abatement addresses penalties resulting from circumstances beyond taxpayer control, such as serious illness, natural disasters, or reliance on incorrect professional advice. The options for taxpayers needing payment assistance include exploring penalty relief alongside payment arrangements.

Common Mistakes When Setting Up IRS Payments

Even with straightforward online tools, taxpayers frequently make errors that complicate payment arrangements or lead to defaults. Awareness of these pitfalls helps you avoid unnecessary complications.

Underestimating Total Costs

Many taxpayers focus solely on the principal tax amount while overlooking accumulated penalties and interest. Before you irs set up payments, request a complete account transcript showing all assessments, payments, and accruals. This comprehensive view prevents surprise balance increases that render your payment calculation insufficient.

Interest continues accruing throughout the payment period, meaning your final payment amount will exceed the balance shown when you establish the agreement. Building a small cushion into your calculations accounts for this ongoing accumulation.

Ignoring State Tax Obligations

Federal installment agreements address only IRS debt. State tax agencies maintain separate collection processes and payment plan options. Taxpayers with both federal and state liabilities must coordinate dual payment arrangements, ensuring sufficient cash flow for both obligations.

Some states offer similar simplified payment plan options, while others require more extensive financial disclosure regardless of debt amount. Failing to address state obligations while focusing on federal debt simply shifts the problem rather than solving it.

Setting Unrealistic Payment Amounts

Proposing monthly payments you cannot consistently afford sets you up for default. The IRS prefers conservative payment amounts you can maintain reliably over optimistic proposals that fail within months.

Before finalizing any payment amount, track your actual spending for at least two months to identify your genuine disposable income. This realistic assessment prevents the common mistake of basing calculations on ideal budgets that do not reflect actual spending patterns.

Missing Application Deadlines

The IRS provides specific timeframes for responding to collection notices and submitting payment plan applications. Missing these deadlines can result in lost opportunities for favorable terms or progression to enforced collection actions like levies and liens.

Collection Due Process hearings offer taxpayers facing liens or levies the opportunity to propose payment arrangements before enforcement proceeds. These hearings come with strict 30-day response deadlines from notice issuance. Missing this window forfeits valuable appeal rights.

Strategic Considerations for Business Owners

Business tax debt presents unique challenges distinct from individual obligations. Employment tax liabilities carry more aggressive collection timelines and personal liability considerations that affect payment strategy.

Trust Fund Recovery Penalty Implications

Business owners responsible for collecting and remitting payroll taxes face potential Trust Fund Recovery Penalty assessments when these obligations go unpaid. This penalty makes business owners personally liable for the trust fund portion of employment taxes, bypassing corporate liability protection.

When business tax debt includes employment taxes, payment allocation becomes strategically important. The IRS applies payments first to trust fund taxes, then to non-trust-fund portions. Understanding this sequencing helps business owners protect themselves from expanded personal liability.

Balancing Current Operations and Past Debt

Maintaining a business payment plan requires generating sufficient revenue to cover both current tax deposits and installment payments on past debt. This dual obligation often necessitates improved cash flow management, expense reduction, or revenue enhancement strategies.

Some business owners find that professional tax resolution services provide valuable support in negotiating sustainable payment terms while implementing systems to prevent future tax debt accumulation. The CLAW Tax Group blog offers resources addressing common business tax challenges and resolution strategies.

Corporate Structure Considerations

The legal structure of your business affects available payment options and liability exposure. Sole proprietors and partners face direct personal liability for business taxes, while corporate structures may provide some separation between business and personal obligations.

This distinction influences whether to pursue business or individual payment arrangements, particularly when dealing with mixed debt types across multiple entities or tax identification numbers.

Recent Changes to IRS Payment Programs

The IRS regularly updates payment plan policies, fees, and eligibility thresholds. Staying informed about these changes ensures you access the most favorable terms available for your situation.

Expanded Online Access

Recent years have seen significant expansion of self-service options through the IRS website. The Online Payment Agreement application now handles more complex scenarios previously requiring phone or mail submissions, including business payment plans and situations involving multiple tax years.

These digital tools provide immediate determination for qualified taxpayers, eliminating the weeks-long wait associated with traditional processing methods. The IRS self-service payment plan options emphasize convenience and security improvements.

Fee Structure Updates

Setup fees change periodically, with the IRS typically announcing adjustments through official notices. Currently, low-income taxpayers may qualify for fee waivers or reductions when demonstrating financial hardship. The reimbursement option allows eligible taxpayers to reclaim setup fees after completing their payment agreements.

Direct debit arrangements consistently carry the lowest fees, incentivizing automatic payment methods that reduce administrative burden for both taxpayers and the IRS.

Threshold Adjustments

The IRS periodically increases debt thresholds for streamlined processing, expanding the number of taxpayers who can access simplified approval without extensive financial documentation. Recent threshold increases for streamlined installment agreements from $50,000 to current levels reflect this taxpayer-friendly trend.

Monitoring these threshold changes helps taxpayers time their applications strategically, particularly when balances hover near eligibility boundaries. Sometimes waiting for a threshold increase provides access to simplified processing previously unavailable.

When Professional Representation Makes Sense

While many taxpayers successfully navigate payment plan applications independently, certain situations benefit substantially from professional tax resolution assistance. Recognizing when to seek help can save money and improve outcomes.

Complex Financial Situations

Taxpayers with multiple income sources, significant assets, ongoing business operations, or previous IRS negotiations often benefit from professional guidance. Tax resolution specialists understand IRS financial analysis methods and can position your information for optimal results.

Professional representation proves particularly valuable when pursuing Offers in Compromise, appealing collection actions, or negotiating partial payment arrangements. These advanced resolution options carry higher stakes and more complex requirements than standard installment agreements.

Serious Collection Threats

Facing immediate levy threats, wage garnishments, or federal tax liens requires swift, strategic action. Professionals familiar with Collection Due Process procedures can quickly implement protective measures while negotiating sustainable long-term solutions.

The consequences of missteps in high-stakes situations justify professional fees through improved outcomes and protected assets. Tax attorneys and enrolled agents possess specialized knowledge of collection procedures and taxpayer rights that most individuals lack.

Business Tax Debt

Business owners dealing with payroll tax debt, multiple entity structures, or ongoing compliance challenges typically achieve better outcomes with professional assistance. The complexity of business tax resolution, combined with personal liability risks, makes expert guidance a sound investment.

Representatives can coordinate multi-year payment plans, negotiate concurrent individual and business agreements, and implement systems preventing future tax debt accumulation while resolving past obligations.

Successfully navigating IRS payment options requires understanding available programs, calculating sustainable payment amounts, and maintaining consistent compliance with both agreement terms and ongoing tax obligations. The process has become increasingly accessible through online tools, though individual circumstances often benefit from strategic planning beyond basic installment arrangements. If you are facing tax debt that feels unmanageable or need expert guidance on structuring the most advantageous payment solution, CLAW Tax Group provides comprehensive tax resolution services including installment agreement negotiations, Offers in Compromise, and legal representation to protect your financial interests while resolving your tax obligations.