Facing a tax bill you cannot pay in full can feel overwhelming, but understanding how to make an IRS payment plan provides a practical path forward. The IRS offers several installment agreement options designed to help taxpayers manage their obligations without devastating their finances. Whether you owe $5,000 or $50,000, knowing the requirements, application process, and strategic considerations can make the difference between financial recovery and escalating penalties.

Understanding IRS Payment Plan Options

The IRS provides multiple payment plan structures tailored to different debt amounts and taxpayer situations. Selecting the right option depends on how much you owe, your ability to pay, and how quickly you can satisfy the debt.

Short-Term Payment Plans

Short-term payment plans allow taxpayers to pay their full balance within 180 days or less. This option suits those who need a brief extension but can manage the full payment relatively quickly.

Key features include:

- Available for balances under $100,000 (combined tax, penalties, and interest)

- No setup fee required

- Must satisfy the debt within 180 days

- Interest and penalties continue to accrue until paid in full

The IRS offers multiple tax payment options that accommodate different financial situations, with short-term plans being the most straightforward for those with temporary cash flow issues.

Long-Term Payment Plans (Installment Agreements)

Long-term installment agreements extend beyond 180 days and accommodate taxpayers who need years to resolve their tax debt. These plans require monthly payments and come with setup fees, but they provide breathing room for those facing significant liabilities.

| Plan Type | Debt Limit | Setup Fee (Online) | Setup Fee (Other Methods) | Payment Period |

|---|---|---|---|---|

| Short-Term | $100,000 | $0 | $0 | Up to 180 days |

| Long-Term (Direct Debit) | $50,000 | $31 | $107 | Beyond 180 days |

| Long-Term (Standard) | $50,000 | $130 | $225 | Beyond 180 days |

Low-income taxpayers may qualify for fee reductions or waivers, making these agreements more accessible across income levels.

Eligibility Requirements to Make IRS Payment Plan

Before you attempt to make an IRS payment plan, understanding eligibility criteria prevents application delays and rejections. The IRS evaluates several factors when reviewing installment agreement requests.

Basic Qualification Standards

To qualify for any payment plan, you must meet these fundamental requirements:

- File all required tax returns. The IRS will not approve payment plans for taxpayers with unfiled returns.

- Owe $50,000 or less for streamlined long-term agreements (combined tax, penalties, and interest).

- Demonstrate inability to pay the full amount immediately without causing financial hardship.

- Agree to remain compliant with all filing and payment requirements during the agreement period.

- Not currently be in bankruptcy proceedings.

The online payment agreement application streamlines the approval process for qualifying taxpayers, often providing instant confirmation.

Financial Disclosure Requirements

For debts exceeding $50,000, the IRS requires detailed financial disclosure through Form 433-F (Collection Information Statement). This document reveals your income, expenses, assets, and liabilities, allowing the IRS to determine appropriate monthly payment amounts.

Information you'll need to provide:

- Monthly household income from all sources

- Necessary living expenses (housing, utilities, food, transportation)

- Asset values (real estate, vehicles, investments)

- Other financial obligations (credit cards, loans, mortgages)

Professional guidance from tax resolution services can prove invaluable when navigating complex financial disclosures and negotiating favorable payment terms.

Step-by-Step Process to Make IRS Payment Plan

Successfully establishing a payment plan requires following specific procedures and gathering necessary documentation beforehand. Preparation significantly increases approval likelihood and expedites processing.

Gather Required Documentation

Before beginning your application, compile these essential documents:

- Copies of unfiled tax returns (if applicable)

- Most recent tax bill or notice from the IRS

- Financial statements showing income and expenses

- Bank account information for direct debit setup

- Details of assets and monthly obligations

Having this information readily available prevents application delays and ensures accuracy throughout the process.

Choose Your Application Method

The IRS accepts payment plan applications through three primary channels, each with different processing times and fees.

Online Application (Fastest)

The IRS online payment agreement system offers the quickest approval and lowest fees. Individual taxpayers can apply through the Online Payment Agreement tool, while businesses use the Business Online Payment Agreement system.

Benefits of online application:

- Immediate determination for qualifying taxpayers

- Lowest setup fees ($31 for direct debit, $130 for standard)

- 24/7 availability

- Secure electronic submission

Phone Application

Calling the IRS at 1-800-829-1040 (individuals) or 1-800-829-4933 (businesses) allows you to speak with a representative who can guide you through the process. However, phone applications take longer and carry higher fees.

Mail or In-Person Application

Form 9465 (Installment Agreement Request) can be mailed to the IRS address on your tax bill or submitted in person at a Taxpayer Assistance Center. This method involves the longest processing times and highest fees ($225 for standard agreements).

Complete the Application Accurately

When completing your payment plan request, precision matters. Errors or omissions trigger delays or rejections.

- Calculate your proposed monthly payment. Divide your total debt by the number of months you need (up to 72 months for streamlined agreements).

- Select your payment day. Choose a date between the 1st and 28th of each month that aligns with your income cycle.

- Provide accurate financial information. Underreporting income or expenses can result in agreement termination.

- Choose direct debit if possible. Automatic withdrawals ensure timely payments and qualify for reduced fees.

The IRS emphasizes convenience and security in its self-service payment plan options, making online submission the preferred method for most taxpayers.

Strategic Considerations When You Make IRS Payment Plan

Beyond simply establishing a payment plan, strategic thinking optimizes your financial position and minimizes long-term costs. Understanding the implications of different choices helps you make informed decisions.

Minimize Interest and Penalties

Even with an approved payment plan, interest and late payment penalties continue accumulating on unpaid balances. The combined rate currently hovers around 8% annually, though it fluctuates quarterly based on federal rates.

Strategies to reduce total costs:

- Pay more than the minimum monthly amount whenever possible

- Make lump-sum payments when receiving windfalls (tax refunds, bonuses)

- Consider the plan duration carefully-shorter agreements mean less total interest

- Explore whether an Offer in Compromise might reduce your overall debt

The financial impact of extended payment plans can be substantial. A $30,000 debt paid over six years at 8% annual interest adds approximately $8,000 to your total obligation.

Maintain Compliance During Your Agreement

Payment plan agreements contain strict compliance requirements. Violating these terms results in immediate default and aggressive collection actions.

Critical compliance requirements:

- File all future tax returns on time

- Pay all future tax liabilities in full by their due dates

- Make all scheduled installment payments by their due dates

- Respond promptly to IRS correspondence

- Update the IRS if your financial situation changes significantly

A single missed payment or unfiled return can terminate your agreement, reinstating the full balance and subjecting you to liens, levies, and wage garnishments.

Consider Professional Representation

Complex tax situations often benefit from professional guidance. Tax resolution specialists understand IRS procedures, negotiation strategies, and alternative solutions that might better serve your situation.

When to seek professional help:

- Your tax debt exceeds $50,000

- You've received IRS notices of levy or lien

- You're considering alternatives like Offers in Compromise

- Previous payment plan applications were denied

- You're facing potential criminal tax charges

- Your financial situation is complex (multiple income sources, self-employment, business ownership)

Professional representation often pays for itself through better negotiation outcomes and avoidance of costly mistakes during the application process.

Common Mistakes That Jeopardize Payment Plans

Understanding what derails payment plans helps you avoid preventable setbacks. Many taxpayers inadvertently sabotage their agreements through common errors.

Proposing Unrealistic Payment Amounts

Optimism about future income can lead to proposing monthly payments you cannot sustain. When you default on those payments, the IRS terminates your agreement and may be less willing to negotiate future arrangements.

Best practices for setting payment amounts:

- Base calculations on current, verified income-not projected raises

- Account for seasonal income fluctuations

- Build in a small buffer for unexpected expenses

- Review your actual monthly spending before committing

The IRS provides various options to help taxpayers manage their obligations, but those options only work when payment amounts align with real financial capacity.

Ignoring Future Tax Obligations

Many taxpayers focus exclusively on past debt while neglecting current year obligations. This creates a cycle where you're constantly behind, accumulating new debt while paying old.

If you're self-employed or have income not subject to withholding, make quarterly estimated tax payments to avoid compounding your debt. Adjust W-4 withholding if you're an employee receiving a paycheck.

Failing to Communicate Financial Changes

Job loss, medical emergencies, or other financial hardships can make previously manageable payments impossible. Ignoring this reality and simply stopping payments guarantees default.

Instead, contact the IRS immediately when circumstances change:

- Request a payment plan modification

- Provide documentation of changed circumstances

- Propose adjusted payment amounts based on new financial reality

- Consider temporary suspension if you're experiencing extreme hardship

Proactive communication demonstrates good faith and often results in modified terms rather than default and collection action.

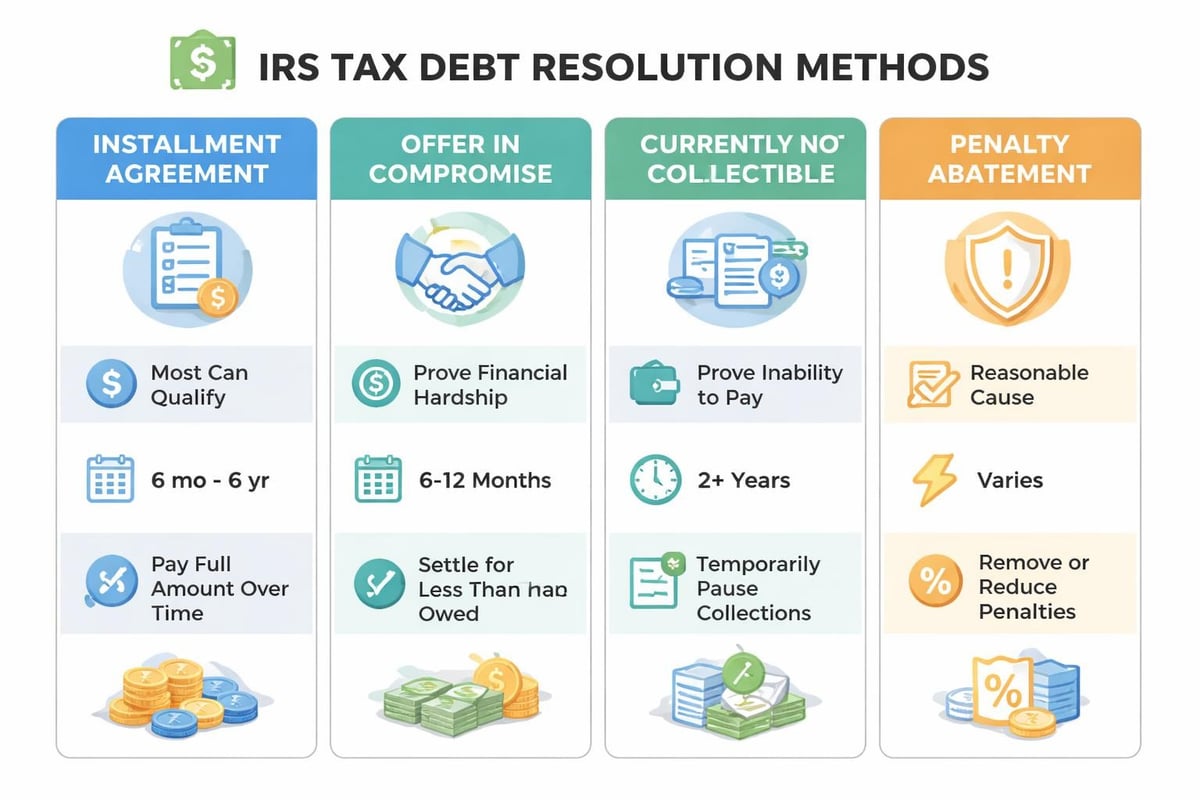

Alternative Solutions to Traditional Payment Plans

While installment agreements solve many tax debt situations, they're not always the optimal solution. Understanding alternatives helps you choose the most beneficial approach.

Offer in Compromise

An Offer in Compromise allows qualifying taxpayers to settle their tax debt for less than the full amount owed. This option suits those experiencing genuine financial hardship with limited assets and income.

| Criteria | Installment Agreement | Offer in Compromise |

|---|---|---|

| Debt Reduction | None (full balance plus interest) | Potential significant reduction |

| Qualification | Most taxpayers qualify | Strict eligibility requirements |

| Processing Time | Days to weeks | 6-12 months or longer |

| Success Rate | High (most are approved) | Low (historically 30-40%) |

| Long-Term Impact | Debt satisfied over time | Immediate resolution if accepted |

The application process is complex and benefits significantly from professional assistance. The CLAW Tax Group blog provides detailed information on various tax resolution strategies, including Offers in Compromise.

Currently Not Collectible Status

If you literally cannot afford any payment toward your tax debt without creating financial hardship, Currently Not Collectible (CNC) status temporarily suspends collection activities. The IRS places your account in this status after verifying that collecting would prevent you from meeting basic living expenses.

Important considerations:

- Interest and penalties continue accumulating

- The IRS reviews your financial situation periodically

- Tax refunds may be applied to your debt

- The IRS can reverse CNC status if your situation improves

- The collection statute of limitations continues running

CNC status provides breathing room during genuine financial crises but should be viewed as temporary relief, not a permanent solution.

Penalty Abatement

The IRS may remove or reduce penalties if you have reasonable cause for late payment or filing. First-time penalty abatement is particularly accessible for taxpayers with clean compliance history.

Successful penalty abatement can reduce your total debt by 25% or more, making it worthwhile to explore even if you still need a payment plan for the remaining balance. This strategy works best when combined with a comprehensive tax resolution approach.

Managing Your Payment Plan Long-Term

Successfully establishing a payment plan represents just the beginning. Maintaining the agreement requires ongoing attention and financial discipline.

Set Up Automatic Payments

Direct debit arrangements eliminate the risk of missed payments due to oversight. Beyond convenience, automatic withdrawals qualify for reduced setup fees ($31 versus $130 for online applications).

Steps to establish direct debit:

- Provide bank routing and account numbers during application

- Verify the withdrawal date aligns with your income schedule

- Ensure sufficient funds are available on the withdrawal date

- Monitor your account to confirm successful withdrawals

- Maintain adequate balance to avoid overdraft fees

Most payment plan defaults result from simple forgetfulness rather than inability to pay. Automation removes this risk entirely.

Track Your Progress

Understanding your remaining balance and projected payoff date helps maintain motivation and allows for strategic additional payments.

Key metrics to monitor:

- Remaining principal balance

- Accrued interest since agreement establishment

- Total payments made to date

- Projected payoff date at current payment rate

- Potential savings from increased payments

The IRS provides balance information through its online account system, allowing you to track progress and verify accurate payment application.

Prepare for Agreement Completion

As your payment plan nears completion, take steps to ensure successful closure and prevent future tax debt:

- Verify final payoff amount with the IRS several months before scheduled completion

- Request lien releases if a tax lien was filed during your debt period

- Review your compliance history to ensure all returns were filed and payments made

- Adjust withholding or estimated payments to prevent future debt accumulation

- Maintain emergency savings to cover unexpected tax liabilities

Successfully completing a payment plan improves your standing with the IRS and makes future negotiations easier if tax issues arise again.

Impact of Payment Plans on Your Financial Health

Understanding how payment plans affect your broader financial situation helps you make informed decisions and plan accordingly.

Credit Implications

The IRS doesn't directly report payment plans to credit bureaus. However, tax liens (which may be filed for larger debts) do appear on credit reports and significantly impact credit scores.

- Payment plans themselves: No credit impact

- Tax liens filed before payment plan: Negative credit impact

- Successfully completing plan: No credit improvement (but prevents further damage)

- Defaulting on plan: May lead to liens, which damage credit

Recent IRS policy changes have increased the threshold for automatic lien filing, but debts exceeding $25,000 still carry this risk. Negotiating lien withdrawal or subordination as part of your payment plan can mitigate credit damage.

Refund Offset Expectations

While making payments under an installment agreement, the IRS automatically applies any tax refunds to your outstanding balance. This reduces your debt faster but eliminates refunds you might have counted on for other expenses.

Planning considerations:

- Adjust withholding to break even rather than receiving large refunds

- Don't plan major expenses around expected refund amounts

- Consider refund offsets as "forced" extra payments that accelerate debt resolution

- Request refund release only in extreme hardship situations

Strategic withholding adjustment prevents the disappointment of lost refunds while giving you control over cash flow throughout the year.

Future Borrowing Considerations

Some lenders check for tax liens during mortgage or business loan applications. An active payment plan might raise questions during underwriting, though it demonstrates responsibility compared to unpaid, unresolved tax debt.

Be prepared to explain:

- The reason for the original tax debt

- Your current payment plan terms and compliance history

- Steps taken to prevent future tax issues

- Remaining balance and projected payoff date

Transparency and demonstrated responsibility often satisfy lender concerns, particularly when the payment plan is well-established with a strong compliance record.

Successfully navigating the process to make an IRS payment plan requires understanding your options, meeting eligibility requirements, and maintaining compliance throughout the agreement period. While the IRS offers accessible self-service options, complex situations often benefit from professional guidance to ensure you choose the most advantageous resolution strategy. CLAW Tax Group specializes in helping taxpayers establish favorable payment arrangements, negotiate alternative solutions like Offers in Compromise, and protect assets from aggressive collection actions-providing the expertise and representation needed to resolve tax debt while minimizing financial impact.