Filing your taxes late or failing to pay what you owe can lead to significant financial consequences. A penalty tax return refers to a tax return that triggers penalties from the IRS or state tax authorities due to late filing, late payment, underpayment, or accuracy issues. These penalties can accumulate rapidly, turning a manageable tax bill into a substantial debt. Understanding how these penalties work, when they apply, and what steps you can take to minimize or eliminate them is essential for protecting your financial health and avoiding long-term complications with tax authorities.

Understanding Penalty Tax Return Situations

A penalty tax return occurs when specific violations of tax law result in additional charges beyond your base tax liability. These penalties serve as enforcement mechanisms designed to encourage timely and accurate tax compliance. The IRS imposes various penalty types, each with distinct triggers and calculation methods.

Common Types of Tax Penalties

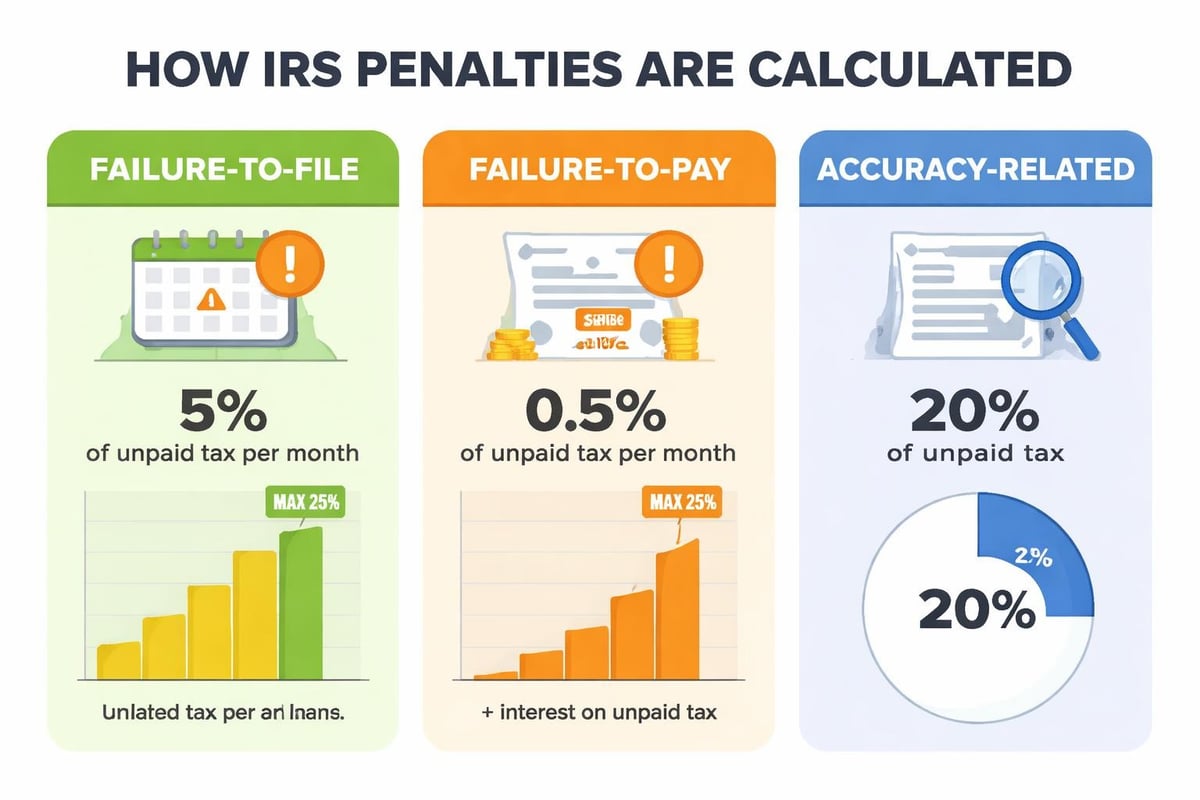

The most frequently encountered penalties fall into several categories. Failure-to-file penalties apply when you miss the tax filing deadline without obtaining an extension. This penalty typically equals 5% of unpaid taxes for each month or part of a month that your return is late, up to a maximum of 25%. The failure to pay penalty accrues at 0.5% per month on unpaid tax balances, also capping at 25%.

When both penalties apply simultaneously, the failure-to-file penalty reduces to 4.5% per month, while the failure-to-pay penalty remains at 0.5%. This combined rate of 5% per month can quickly inflate your tax debt.

Accuracy-related penalties address issues with the information reported on your return. These include:

- Negligence or disregard of rules and regulations

- Substantial understatement of income tax

- Substantial valuation misstatements

- Substantial overstatement of pension liabilities

- Substantial estate or gift tax valuation understatements

These penalties generally equal 20% of the underpayment portion attributable to the error.

Estimated Tax Penalties

Business owners, self-employed individuals, and investors often face underpayment of estimated tax penalties. When you don't pay enough tax through withholding or quarterly estimated payments, the IRS calculates this penalty based on the underpayment amount and the time period it remained unpaid.

The penalty uses a variable interest rate that adjusts quarterly. You can generally avoid this penalty by paying at least 90% of your current year's tax liability or 100% of the previous year's tax liability (110% if your adjusted gross income exceeds $150,000).

| Penalty Type | Rate/Calculation | Maximum | Key Trigger |

|---|---|---|---|

| Failure to File | 5% per month | 25% | Missing deadline |

| Failure to Pay | 0.5% per month | 25% | Unpaid balance |

| Accuracy-Related | 20% of underpayment | No cap | Reporting errors |

| Estimated Tax | Variable interest rate | No cap | Insufficient quarterly payments |

How Penalty Tax Returns Impact Your Financial Situation

The financial consequences of a penalty tax return extend beyond immediate monetary costs. Interest continues accruing on both unpaid taxes and penalties, creating a compounding effect that accelerates debt growth. The IRS compounds interest daily, meaning every day of delay increases your total obligation.

Calculation Example

Consider a scenario where you owe $10,000 in taxes and file your return six months late without paying. Your failure-to-file penalty reaches $2,500 (5% × $10,000 × 5 months = $2,500). Your failure-to-pay penalty adds $300 ($10,000 × 0.5% × 6 months). Combined with interest charges, your original $10,000 debt could exceed $13,000 within half a year.

State tax authorities impose their own penalty structures. New York State interest and penalties differ from federal rates, while California Franchise Tax Board penalties follow separate guidelines. Taxpayers subject to multiple jurisdictions face layered penalty assessments that multiply their financial exposure.

Long-Term Consequences

Beyond immediate financial impact, penalty tax returns can trigger:

- Tax liens that attach to your property and appear on credit reports

- Levies allowing the IRS to seize bank accounts, wages, or other assets

- Collection actions including garnishments and property seizures

- Professional licensing issues for those in regulated industries

- Passport restrictions for seriously delinquent tax debts exceeding $62,000

Strategies to Minimize or Eliminate Penalties

Multiple avenues exist for reducing or removing penalties from a penalty tax return. Success depends on your specific circumstances, compliance history, and ability to demonstrate reasonable cause.

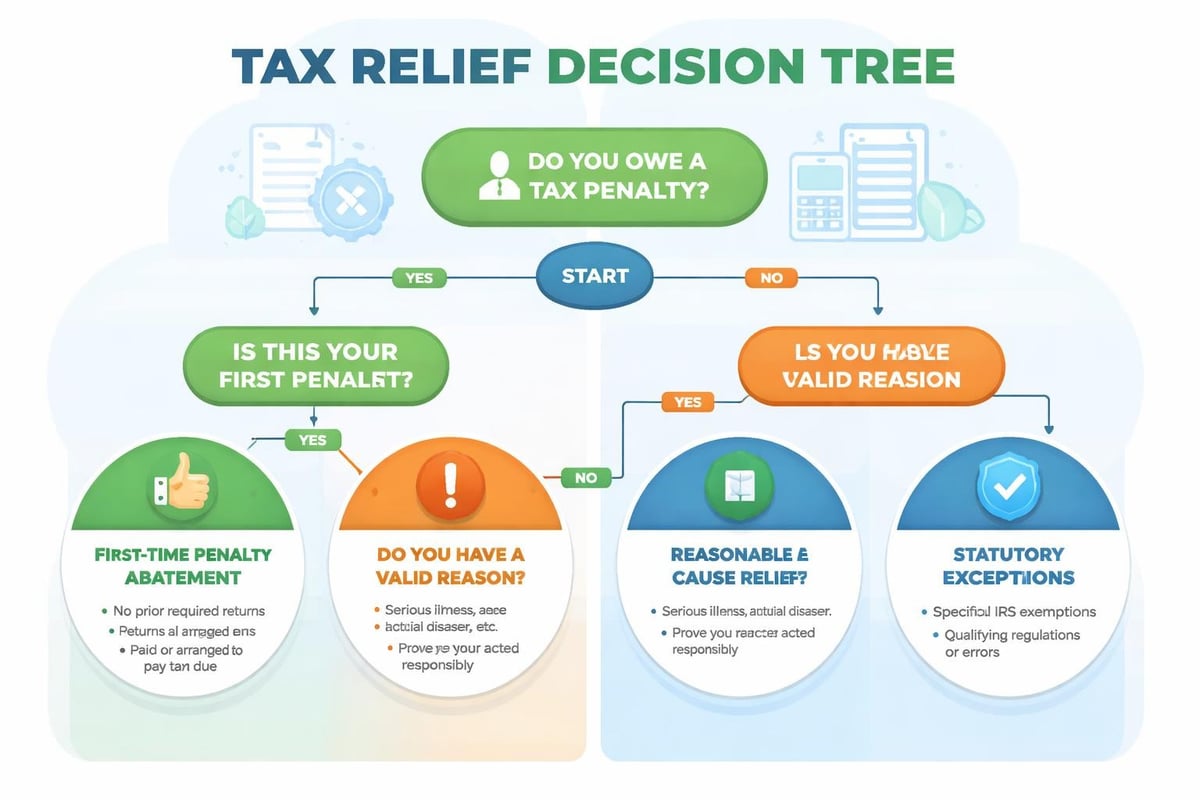

First-Time Penalty Abatement

The IRS offers administrative relief for taxpayers with clean compliance histories. First-time penalty abatement (FTA) removes failure-to-file, failure-to-pay, and failure-to-deposit penalties if you meet specific criteria:

- No penalties for the three preceding tax years

- All required returns filed or extensions obtained

- Payment arrangements established for current obligations

FTA doesn't require proving reasonable cause, making it the most accessible penalty relief option for eligible taxpayers. You request FTA by calling the IRS or including a written request with correspondence.

Reasonable Cause Relief

When FTA doesn't apply, reasonable cause provides an alternative path. You must demonstrate that despite ordinary business care and prudence, circumstances beyond your control prevented timely filing or payment. Acceptable reasons include:

- Serious illness or death in your immediate family

- Natural disasters that destroyed records or prevented filing

- Unavoidable absence such as required travel

- Fire, casualty, or theft affecting your ability to comply

- Official error or delay by the IRS or postal service

Documentation strengthens reasonable cause claims. Medical records, death certificates, insurance reports, and contemporaneous correspondence establish credibility.

Statutory Exceptions

Specific situations qualify for automatic penalty relief. Combat zone service members receive extensions and penalty waivers. Federally declared disaster areas trigger automatic deadline extensions. IRS penalties guidance outlines these special circumstances and required procedures.

Correcting a Penalty Tax Return

When you've already filed a return that triggered penalties, several correction methods can reduce your liability and demonstrate good-faith compliance.

Filing Amended Returns

An amended return using Form 1040-X corrects errors on original filings. While amending doesn't automatically remove penalties, it shows effort to comply correctly. If the amendment reduces your tax liability, associated penalties decrease proportionally.

You have three years from the original filing date or two years from when you paid the tax (whichever is later) to file most amended returns. Some situations allow longer timeframes.

Payment Plans and Offers in Compromise

Establishing payment arrangements demonstrates commitment to resolving tax debts. The IRS offers several options:

- Short-term payment plans (120 days or less) with no setup fees

- Long-term installment agreements spreading payments over multiple years

- Partial payment installment agreements when you cannot pay the full amount

- Offers in Compromise settling tax debts for less than the full balance

Working with CLAW Tax Group helps you navigate these options and negotiate favorable terms. Professional representation ensures you present the strongest case for penalty reduction and debt resolution.

| Resolution Option | Timeline | Best For | Impact on Penalties |

|---|---|---|---|

| First-Time Abatement | Immediate | Clean compliance history | Complete removal |

| Reasonable Cause | 30-90 days | Documented hardship | Complete removal |

| Payment Plan | Ongoing | Cannot pay immediately | Reduces accrual rate |

| Offer in Compromise | 6-24 months | Financial hardship | Settles penalties with tax debt |

Preventing Future Penalty Tax Returns

Proactive tax planning prevents penalty assessments and maintains positive standing with tax authorities. Implementing systematic approaches to compliance reduces risk and stress.

Establishing Filing Systems

Organize tax documents throughout the year rather than scrambling at deadline time. Create digital and physical filing systems that categorize:

- Income statements (W-2s, 1099s, K-1s)

- Deduction receipts organized by category

- Estimated tax payment confirmations

- Prior year returns and supporting documentation

- Correspondence from tax authorities

Set calendar reminders for quarterly estimated tax deadlines (April 15, June 15, September 15, and January 15). Missing even one payment can trigger penalties on a penalty tax return.

Working with Tax Professionals

Tax professionals provide expertise that minimizes errors and ensures compliance. They stay current on tax law changes, identify deductions you might miss, and represent you if issues arise. Tax preparer penalties incentivize professionals to maintain accuracy and due diligence.

When selecting a tax professional, verify their credentials. Enrolled agents, CPAs, and tax attorneys possess different specializations. Tax resolution specialists focus specifically on resolving issues with existing tax debts and penalty tax returns.

Maintaining Adequate Withholding

Employees should review W-4 forms annually and after major life changes. Adjust withholding when you:

- Get married or divorced

- Have children or dependents

- Start a side business

- Receive investment income

- Change jobs or income levels

Self-employed individuals should calculate quarterly estimated taxes based on projected annual income. Conservative estimates prevent underpayment penalties while avoiding excessive overpayment that ties up working capital.

Special Considerations for Business Owners

Businesses face additional penalty tax return risks beyond individual taxpayer concerns. Payroll tax penalties, information return penalties, and corporate filing requirements create multiple compliance obligations.

Payroll Tax Compliance

Employers must deposit payroll taxes according to specific schedules determined by total tax liability. Missing deposit deadlines triggers penalties ranging from 2% to 15% of the unpaid amount, depending on how late the payment arrives. The information return penalties structure applies to Forms W-2, 1099, and other information reporting documents.

Trust fund recovery penalties personally assess responsible parties for unpaid payroll taxes. This penalty equals 100% of the unpaid trust fund taxes (employee withholding portions) and applies when someone willfully fails to collect, account for, or pay over these taxes.

Business Entity Specific Penalties

Different business structures face unique penalty exposures:

- S corporations pay late filing penalties of $210 per shareholder per month (up to 12 months) for failing to file Form 1120-S timely

- Partnerships incur similar penalties for late Form 1065 filings

- C corporations face penalties for estimated tax underpayments and late filing

- LLCs encounter state-specific penalties varying by jurisdiction

Multi-state businesses must track varying state penalty structures and filing deadlines. A compliant federal return doesn't guarantee state compliance.

Responding to IRS Penalty Notices

Receiving an IRS notice regarding penalties on a penalty tax return requires prompt, informed action. Different notice types demand specific responses within defined timeframes.

Understanding Notice Types

The IRS issues notices through mail, never by phone or email initially. Common penalty-related notices include:

- CP14 – Balance due with failure-to-pay penalty

- CP161 – Balance due after second notice

- CP503 – Reminder of balance due

- CP504 – Intent to levy notice

- CP2000 – Proposed changes based on information returns

Each notice includes a response deadline and specific instructions. Missing these deadlines limits your options for resolution.

Challenging Penalties

You have the right to challenge penalty assessments through several mechanisms:

- Written explanation responding to the notice within the stated deadline

- Form 843 (Claim for Refund) requesting penalty abatement after payment

- Appeals process if the IRS denies your initial request

- Tax Court petition if you receive a statutory notice of deficiency

Professional representation strengthens penalty challenges by ensuring proper procedure and persuasive presentation. Tax attorneys and enrolled agents understand IRS procedures and negotiation strategies that improve outcomes.

Documentation Requirements

Supporting your penalty tax return response requires comprehensive documentation. Gather:

- Copies of all tax returns for relevant years

- Payment records showing when amounts were paid

- Bank statements demonstrating financial constraints

- Medical records supporting illness claims

- Correspondence establishing timeline of events

- Professional assessments or reports relevant to your situation

Organize documents chronologically and create a clear narrative explaining your circumstances. Vague or incomplete responses typically result in denial.

The Role of Tax Resolution Services

Complex penalty tax return situations often exceed the typical taxpayer's expertise. Tax resolution specialists focus exclusively on resolving IRS and state tax problems, bringing specialized knowledge to challenging situations.

When to Seek Professional Help

Consider professional assistance when you face:

- Multiple years of unfiled returns

- Substantial penalties exceeding several thousand dollars

- Collection actions such as liens, levies, or garnishments

- Criminal investigation concerns

- Complex business tax issues

- Disagreement with IRS assessments

- Financial hardship preventing payment

Early intervention prevents problems from escalating. Once the IRS initiates collection enforcement, resolution becomes more difficult and expensive.

Services Tax Resolution Firms Provide

Comprehensive tax resolution encompasses multiple services tailored to penalty tax return challenges:

- Analyzing your complete tax situation and identifying all compliance issues

- Preparing unfiled returns to bring you into compliance

- Negotiating penalty abatement based on reasonable cause or FTA

- Establishing payment plans that fit your financial capacity

- Submitting Offers in Compromise to settle debts for less than full payment

- Representing you in audits, appeals, and collection proceedings

- Protecting assets from IRS collection actions

- Removing tax liens and releasing levies

The investment in professional services often saves substantially more than the cost through penalty reduction, improved settlement terms, and faster resolution. When considering options, requesting a consultation with CLAW Tax Group provides clarity on your specific situation and available solutions.

State Tax Penalties and Interactions

Federal penalties represent only part of the penalty tax return picture. State tax authorities impose their own penalties that operate independently from IRS assessments.

State-Specific Penalty Structures

Each state establishes unique penalty rates and rules. California's Franchise Tax Board assesses penalties for late filing, late payment, and frivolous returns. New York State imposes interest and penalties on late payments and underpayment of estimated tax. States without income taxes still impose penalties for business taxes, sales taxes, and employer withholding obligations.

Researching your state's specific requirements prevents unexpected penalty assessments. State tax agencies generally offer less flexibility than the IRS regarding penalty abatement, making prevention especially important.

Coordinating Federal and State Resolution

Resolving federal tax issues doesn't automatically resolve state problems. You must address each jurisdiction separately. However, federal tax returns often serve as the basis for state returns, meaning errors corrected federally should also be corrected on state returns.

Some resolution strategies work at both levels. Offers in Compromise exist in many states, though qualification criteria and acceptance rates vary. Installment agreements are widely available. Penalty abatement procedures differ significantly, with some states offering little flexibility compared to federal FTA and reasonable cause options.

Understanding penalty tax return implications and resolution strategies protects you from escalating tax debts and collection actions. Whether facing failure-to-file penalties, accuracy-related assessments, or estimated tax underpayments, taking prompt action minimizes financial damage and preserves your options. CLAW Tax Group specializes in resolving complex tax situations, negotiating penalty reductions, and establishing manageable payment solutions that protect your assets while achieving compliance with tax authorities.